Suzanne Woolley

March 4, 2024

The return of FOMO is fueling concern that the market may take a tumble.

Strong earnings and an overall downward trend in inflation have helped fuel a surge in the S&P 500 that few would want to miss. But with much of the index’s 30% rise over the past 52 weeks stemming from just a handful of stocks like artificial-intelligence play Nvidia Corp., some market watchers fear there may be a melt-up unfolding.

Below, market veterans and financial advisers offer tips on how to navigate choppy markets and create a portfolio you can stick with. Declines, inevitably, happen. But thinking through the potential impact of a drop can help guard against making any rash moves. So here’s what to keep in mind.

Pedestrians in front of the New York Stock Exchange in New York.Photographer: Michael Nagle/Bloomberg

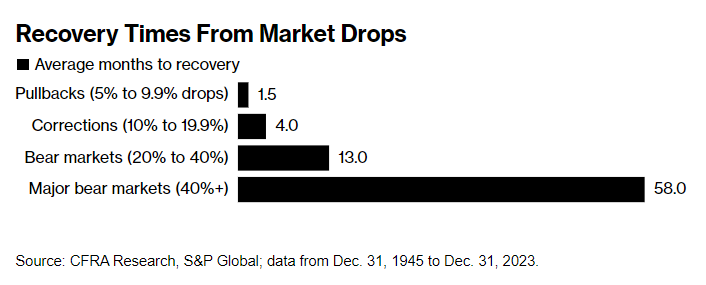

Markets Tend to Recover Quickly

To keep market drops in perspective, Sam Stovall, chief investment strategist of CFRA Research, suggests using stock market history as “virtual Valium.”

“What amazes me is how long people think it takes to get back to breakeven from a correction, or from a decline of from 10% to 20%,” Stovall said. “Most people would say years, but on average it takes about four months.”

The speed of market bounce-backs argues against trying to time the market. Also, with market-timing you have to be right both on when to get out, and when to get back in. Often people talk themselves out of getting back in, fearing that a bullish move could just be prelude to another drop, said Stovall. Missing a handful of top-performing days can have a big impact on long-term returns.

Downturns Are Normal

Just as hitting new highs is normal for a well-functioning stock market, so are downturns.

“To be a disciplined investor, you have to accept ahead of time that even in good markets, it will not continue indefinitely — markets do drop,” said Rob Williams, managing director of financial planning at Charles Schwab. “The good news is that they generally recover, and the general direction of the markets continues to be up.”

A Schwab analysis looked at intra-year stock market declines over the 20 years from 2002 to 2021. There was a drop of 10% in 10 out of the 20 years, so half of the time, and the average size of the pullback was 15%. In two additional years, the decline was nearly 10%.

It sounds stressful, but the good news is that in most of those years, stocks were up, and the average gain was approximately 7%, according to Schwab.

Diversification Can Help Protect

The S&P 500 looms large, but most people don’t have all their money in the index or the mega-cap tech stocks driving its performance.

Whether you use a financial adviser or have exposure to the stock market through a target-date fund (TDF) in a workplace 401(k) retirement plan, your stock holdings are likely more diversified than you may think.

“We continue to educate and remind clients that they are not simply invested in the S&P 500 [and mega-cap tech], where there is significant volatility, emotional trading and inherent risk, as evidenced by declines in those stocks in 2022,” said Laura Mattia, founder of Atlas Fiduciary Financial. “While large-cap US stocks may comprise a portion of our clients’ investments, their overall portfolio is well-balanced across various asset classes which are not overinflated.”

Finding out how your TDF is invested can be reassuring to know if the market drops, and is easy to find out by simply googling a fund, looking on your 401(k) plan’s website, or searching for a fund on Morningstar.com. Theoretically at least, younger investors should welcome downdrafts as times to buy more stock at lower prices. (If you’re in a 401(k) and stay fully invested, your regular contributions will do just that.)

Rebalancing Reduces Risk

If you or a financial adviser have set an asset allocation for your portfolio, like the classic 60/40 split between stocks and bonds, your portfolio may be out of whack given the market’s rise. Your portfolio was designed to reflect your goals and the time horizons attached to those goals, so bringing percentages back in line keeps you on track.

Selling appreciated stock in a taxable account does mean paying capital gains taxes in the following year, but it locks in gains and lowers risk in a portfolio. You may be able to offset those gains by doing some tax-loss harvesting to realize losses.

Schwab’s Williams suggests rebalancing once a year. “If you rebalance more frequently you may be overreacting to market moves,” he said.

You Can Build a Buffer

Many financial planners manage client money in different “ buckets” earmarked for different goals and time horizons.

A bucket for shorter-term needs will be invested conservatively. For someone nearing retirement who will need to tap savings for expenses, that bucket would be one to three years’ worth of low volatility bonds such as Treasuries or high-quality bonds with short durations, said George Gagliardi of Coromandel Wealth Management.

There will be a medium-term bucket, perhaps to fund a child’s college, and a longer-term bucket for retirement money. If you have decades to retirement, that bucket will be heavily in stocks so you get their higher long-term growth and beat inflation. Since you have the short-term bucket to tap for immediate needs, you shouldn’t need to touch that long-term money and can avoid selling stock into a downturn.

© 2024 Bloomberg L.P.