March 7, 2025

Editor’s note (March 6th): Since this article was published, Donald Trump announced that tariffs on Mexican and Canadian goods covered by the North American trade agreement (roughly half their total exports to America, according to the White House) would be paused until April 2nd.

Keeping abreast of Donald Trump’s utterances on tariffs, from actual announcements to vague threats, is a dizzying task. One day he is set on wrecking the integrated North American economy; the next he wants to appease carmakers that depend on it. When it comes to China, he veers between slapping ever-larger levies on its goods and hinting at a desire for a giant trade deal. As for other countries, he speaks ominously of big but so far unspecified tariffs that will soon kick in.

It would be comical were the consequences not so grave, both for America and the rest of the world. In the run-up to last year’s presidential election, as businesses grappled with the uncertainties of Mr Trump’s trade agenda, analysts examined different scenarios. The most bearish focused on his suggestion that he might impose universal tariffs on all goods entering America. Moody’s Analytics, a data outfit, reckoned such levies could by 2026 reduce America’s GDP by nearly 3% relative to its projected path—a decline that would almost certainly mean a recession. The blows to large exporting countries, notably China and Mexico, would be even bigger, the firm’s economists calculated.

iStock-1893923678

Most observers dismissed such outcomes as far-fetched. Surely Mr Trump was just sabre-rattling and would come to his senses when the stockmarket registered its displeasure? Six weeks into his presidency, the worst-case scenarios are looking all too plausible. The idea of a single universal tariff, fixed at 10% or 20%, would be appealing in its simplicity if nothing else. Instead, Mr Trump has started to add tariff to tariff in a hotch-potch of protectionism.

He is going after specific products, vowing levies of 25% on aluminium, copper, lumber and steel. He has targeted America’s biggest trading partners, imposing tariffs of 25% on Canada and Mexico plus 20% on China (on top of the average tariff of over 10% that already applied to most Chinese goods). And he has pledged much more will come on April 2nd, when America will create a wall of tariffs, taxes and non-monetary barriers to match whatever countries levy on American goods. In an address to both houses of Congress on March 4th, Mr Trump laid out his philosophy: “We’ve been ripped off for decades by nearly every country on earth, and we will not let that happen any longer.”

Much of the media discussion about Mr Trump’s tariffs has focused on their inflationary impact. It is true that, as a first-order consequence, they will push up some prices for consumers. Brian Cornell, boss of Target, a retailer, has warned that the prices of fruit and vegetables could rise in the next few days because of America’s reliance on produce from Mexico. If supply chains that criss-cross Canada and Mexico are caught in tariffs, the price of SUVs assembled in North America could rise by $9,000, according to one estimate.

Nevertheless, for inflation to truly be a problem, it would require not just a one-off rise in prices but sustained increases. And for that to happen, consumer demand would have to remain buoyant. Meanwhile, the way markets have reacted to Mr Trump’s tariffs indicates concerns about economic growth are swamping fears of inflation. The S&P 500 index of large American firms has fallen back to where it was before Mr Trump’s election victory in November, wiping out more than $3trn in gains (see chart 1). Yields on Treasury bonds have sagged as investors price in more interest-rate cuts by the Federal Reserve this year—something that central bankers would do only if they were more troubled by damage to the job market than by the risk of resurgent inflation.

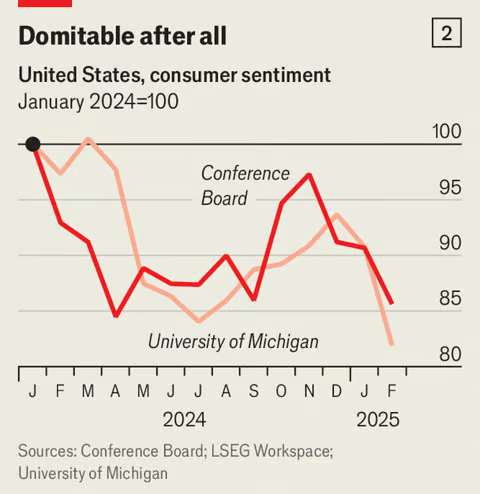

Tariffs weigh on growth in a variety of ways. Higher import prices raise production costs for domestic firms, offsetting the increased output of those that benefit from protection. Higher costs for shoppers lower their real incomes and hence their spending power. This effect already seems visible in a plunge in consumer sentiment (see chart 2). When countries retaliate—an inevitability—exports suffer: those to Mexico and Canada could drop by as much as 60%, according to Oxford Economics, a research firm. Stockmarket falls also represent a tightening of financial conditions, which begets funding challenges for businesses. Last, confusion about tariff implementation is itself an impediment to investment. A gauge of global trade-policy uncertainty created by Fed economists is now at its highest in more than six decades, well above a previous peak in 2018, when Mr Trump mainly targeted China.

Such uncertainty reflects the fact that Mr Trump is moving quickly and aggressively. His first term featured narrower tariffs on steel and aluminium, plus a more protracted dispute with China. Ultimately, Mr Trump’s tariffs covered nearly $400bn-worth of American imports. Not even two months into Mr Trump’s new term, his tariffs reach $1.4trn of imports—a figure that could soon start rising fast.

Given the pain, many still think Mr Trump will back down from his most extreme measures. On March 5th he granted those automakers complying with a North American trade deal struck in 2020 a month’s delay to his latest tariffs. The exemption covers at most 14% of Canadian and 26% of Mexican exports. It is much narrower than the one offered in February, when he delayed tariffs for a month on all North American trade. Moreover, zigzagging on such an important policy hardly makes for a stable business environment. A recent survey of American manufacturers found that their orders contracted in February. Many respondents bemoaned the president’s rush towards tariffs.

Perhaps the biggest surprise of Mr Trump’s presidency so far is his apparent indifference to the downsides of his actions. Investors had thought that he viewed the stockmarket as a scorecard on his presidency. His concern with it has been replaced by a belief that tariffs are obviously good for the economy, since they will revitalise industry and create new government revenues. “There will be a little disturbance, but we are OK with that. It won’t be much,” he said on March 4th.

Growing pains

The president has also glibly dismissed the concerns of American farmers, who sell about a fifth of their total output abroad. They should “get ready to start making a lot of agricultural product to be sold INSIDE of the United States”, he posted on Truth Social, his social-media platform, on March 3rd. In reality, none will pivot from growing soyabeans for export to planting avocado trees for domestic consumption.

For the foreign countries in Mr Trump’s crosshairs, there is deep confusion about what exactly he wants. Claudia Sheinbaum, Mexico’s president, had won plaudits for the cool-headed way she won a late reprieve ahead of Mr Trump’s first deadline in February. The president gushed that she was a “marvellous woman” whom he likes “very much”. Mexican officials had expected, at most, targeted tariffs at a lower rate.

Assuming Mr Trump truly is worried, as he claims, about migrants and fentanyl crossing the border, Ms Sheinbaum has shown herself willing to address his concerns. On February 27th her government took the unprecedented step of extraditing 29 alleged gang members to America. Mexico has also offered to impose extra tariffs on Chinese imports. Discussions between the two countries on these issues have gone well. “But we are talking to irrelevant actors,” says someone on the Mexican side. “This is a personalist regime.”

The relationship between America and Canada is usually characterised by high tedium rather than high tension. Now the ties between Mr Trump and Justin Trudeau has curdled to the point where the Canadian prime minister’s requests for a telephone call in the 24 hours before the tariffs went into effect were ignored. Whereas Ms Sheinbaum has said Mexico will wait until March 9th to announce retaliatory measures—leaving time for quiet discussions—Canada has already put in place tariffs on American goods such as bourbon, citrus fruit and motorcycles. Doug Ford, premier of Ontario, a province at the heart of Canada’s car industry, has threatened to halt the flow of hydro-electric power to several northern American states. “If they want to try to annihilate Ontario, I will do anything, including cutting off their energy, with a smile on my face,” he said.

China has been more restrained, for now. It has introduced tariffs on a small number of American products, including chicken and maize, and added a dozen American firms—none big names—to its unreliable-entity list, which prevents Chinese companies from doing business with them. But it has also rebuffed Mr Trump’s attempts to start talks with Xi Jinping, the country’s leader. Mr Xi is, in effect, giving Mr Trump the silent treatment until he starts to behave and keeping China’s options open for more potent retaliation if he persists in raising tariffs.

In the meantime, American firms are trying to adjust to an economic terrain that is rapidly shifting. Lexi Swift of World Class Shipping, a logistics firm, says that brokering cross-border transactions has become much more complicated. She now has to factor in multiple tranches of tariffs on some products, set up payments for them and advise clients—the importers of record—about the extra money they owe the government. “I’ve seen as much as a 5,000% increase in duties and taxes owed for customers that brought in the same commodities for years,” she says. Normally that is not the sort of growth a business-friendly leader wants. But Mr Trump is convinced that it will be good for America, heedless of all evidence to the contrary. ■