By Reshma Kapadia

Feb. 20, 2024

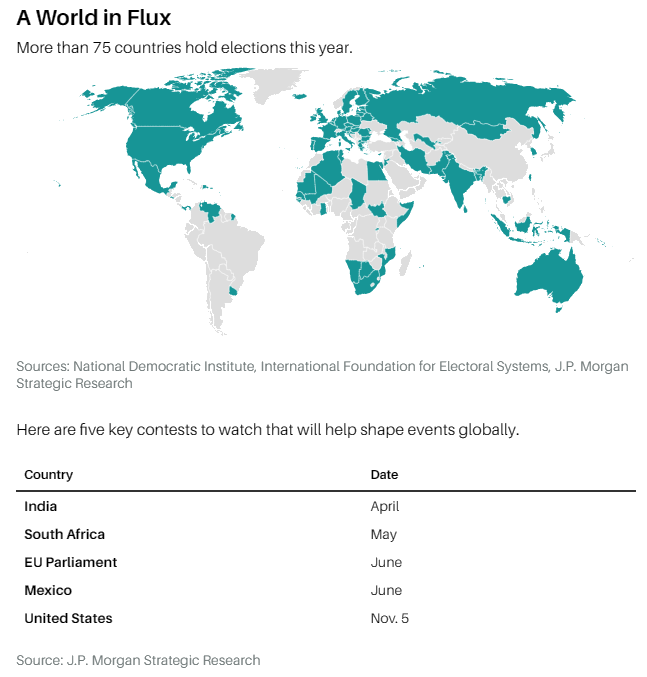

Investors typically ignore elections, but this isn’t a normal year. Nearly 60% of the world’s population heads to the polls as two wars rage, populist candidates are on the march, and higher interest rates make running hefty budget deficits more problematic for countries near and far.

The electoral outcomes this year will shape the global economy in ways that matter to markets, particularly if protectionism stifles global trade and countries have to pick sides as the U.S.-China rivalry intensifies.

Nearly 60% of the world’s population heads to the polls this year. ILLUSTRATION BY NICHOLAS KONRAD

More than 75 countries will hold elections. The year is bookended by two key ones. Taiwan kicked off 2024 by delivering an unprecedented third term for the incumbent party and electing Lai Ching-te, who has vowed to safeguard the country’s independence from China, as president. And the U.S. general election in November probably will be the most consequential anywhere, given sharp policy differences between the probable candidates, current President Joe Biden and his predecessor, Donald Trump.

India heads to the polls in late spring, South Africa in May, and Mexico on June 2. European parliamentary elections will be in June, and a United Kingdom election is likely to be called by year end.

The outcomes will signal to investors whether polarization, populism, democratic deterioration, and geoeconomic fragmentation continue. J.P. Morgan’s head of global research, Joyce Chang, describes these as the “four horsemen” that threaten long-term growth prospects, make economies less efficient, feed market volatility, and dent market multiples.

Investors often dismiss elections because any one administration’s impact tends to play out over decades, not quarters. Neil Shearing, chief economist at Capital Economics, says this year could prove to be an exception, with the possibility of radical shifts in policy, notably in the U.S.

“There are enormous geopolitical implications. That’s the fault line around which election this year matters,” Shearing says.

The populist wave of election outcomes in 2016 sent ripples throughout the global economy, especially with the trade war started under newly elected President Trump. But this year is more consequential, not just in the number of elections but also against a backdrop of higher rates, steeper deficits, and more fragmentation and geopolitical flux.

If Biden is re-elected, he is expected to continue a tough stance on China that limits its access to critical technology, while pushing manufacturers to bring production back to the U.S. or closer to home.

Tariffs are likely to stay in place under Biden, but trade restrictions are expected to be far more prominent in a second Trump administration. Trump recently said that he would consider a 60% tariff on all Chinese imports and a 10% tariff on other imports.

“A Trump Round Two would add to a sense around the world that the policies of his first term weren’t a blip and there’s a bigger political shift in the U.S. that will force other countries abroad to rethink their own policies,” says Owen Tedford, analyst at Beacon Policy Advisors. “That could mean more retaliatory tariffs and trade wars that become faster and more the norm.”

It could also mean more spats between traditional allies. Trump’s recent comments continue to raise questions about his commitment to participation in the North Atlantic Treaty Organization, or NATO. At a recent South Carolina rally, Trump built upon his comments that Europe isn’t paying its share for military protection, adding that he would encourage Russia, for example, to invade U.S. allies that don’t pay enough for military defense. The remarks drew swift backlash from European allies. Trump’s campaign site lists “reject globalism and embrace patriotism” as one of his key issues.

India’s Prime Minister Narendra Modi greeting crowds of supporters. RITESH SHUKLA/GETTY IMAGES

A potential souring in U.S.-Europe relations and a more isolationist policy under Trump could impinge on global growth and add to inflationary pressures. The International Monetary Fund has estimated that international trade restrictions could shave as much as $7 trillion off global economic output over the long term.

“The biggest question is which countries are going to align more with the China-Russia axis versus the U.S. and the West. Some, like India, are playing both sides. It’s one of the reasons these elections matter more,” says Sarah Ketterer, a value investor and head of Causeway Capital Management.

While the U.S. elections may produce the biggest ripples, there are a handful of other big elections that investors are keeping tabs on. That includes three countries that are getting a lot of attention as beneficiaries of the move to reduce reliance on China—Mexico, India, and Indonesia.

India and Mexico have improved their fiscal health over the past five to 10 years, but challenges persist. In Mexico, for example, left-leaning President Andrés Manuel López Obrador surprised investors by being more fiscally conservative than anticipated, managing to keep a balanced budget as the world was reeling from Covid in 2020. He can’t run for re-election under Mexican law, but he’s breaking from tradition by campaigning against the leading opposition candidate in the race to succeed him.

“He gave markets and Mexican society each what they wanted. Markets needed austerity and a reduction of deficits, which he did. But now he is going out with the biggest expenditures and transfers of his term,” says Joan Domene, chief economist for Latin America for Oxford Economics. For example, López Obrador has increased spending on pensions for seniors and scholarship aid, and upgraded an intercity railway that goes across the Yucatán Peninsula “to support the people.”

Reining in some of this government largess will fall on either Claudia Sheinbaum, the front-runner and member of López Obrador’s Morena party, or opposition presidential candidate Xóchitl Gálvez. Such cuts could slow growth, but Mexico remains a favored market for money managers because it is well positioned as American companies look to bring production closer to home.

The bigger wild card for Mexican stocks may be the U.S. election—and whether the outcome creates friction between the neighboring countries. The biggest concern: additional trade restrictions. If Mexico is pulled into a trade war with the U.S., that would quickly spoil the positive economic outlook that has been lifting the country’s stock market and the Mexican peso.

India is another China alternative but it’s more insulated from the U.S. election. The world’s most populous country is home to some of the strongest economic growth anywhere, after a series of reforms from Prime Minister Narendra Modi drew foreign investment to the country.

Modi is widely expected to win a third term this spring. Part of that strong support from voters, as well as some investors, stems from his government’s strategy of combining Hindu nationalistic policies with sensible management of the economy. “As long as Modi continues to pursue gradual reforms with prudent macroeconomic management, investors will look at India favorably,” says TS Lombard chief India economist Shumita Deveshwar.

The one potential hiccup for markets would be if Modi’s Bharatiya Janata Party is unable to secure a majority in Parliament, Deveshwar says. While it’s unlikely to derail the strong growth outlook for India’s economy, Deveshwar says there is a risk that limited political or economic pressure slows the impetus for more reforms and constrains India’s prospects.

Longer term, some investors are concerned about the populist and Hindu nationalist undercurrents in the country, as well as Modi’s increased consolidation of power. “It’s an echo of what Xi has done in China,” says Ketterer. “The parliamentary system is set up to have power sharing. When it’s out of balance in an emerging market country, it can be destabilizing.”

When asked what steps Modi was willing to take to improve the rights of Muslims and other minorities during his U.S. visit last year, he suggested they didn’t need to be improved. In Parliament this week, Modi said the government’s policies were aimed at raising the standard of living for all by ensuring the basics—including access to cheaper medicine, connections to tap water, and building more toilets.

India is still a favored destination for investors, including Ketterer, who leans toward cheaper, smaller-cap companies.

In Indonesia this past week, Minister of Defense Prabowo Subianto had a decisive lead in unofficial tallies and appeared on track to be the next president. The victory for the former military general and son-in-law of former dictator Suharto will keep investors on watch for governance concerns and potential backsliding on business-friendly reforms implemented over the two terms of President Joko Widodo, popularly known as Jokowi. The current president came to power as a reform-oriented leader who wasn’t part of the country’s political and economic elite.

Instead of backing the candidate from his own party, Jokowi supported former political rival Subianto, who ran with Gibran Rakabuming Raka, Jokowi’s eldest son. Capital Economics analysts caution that Subianto could hurt future foreign investments by introducing populist or nationalist policies, derailing the country’s efforts to attract foreign investment into its metals industry. Subianto’s win poses a risk to what are “some of the best long-term growth prospects of any economy,” writes Gareth Leather, Capital Economics’ senior Asia economist, in a note to clients on Wednesday.

The messiest election among bigger emerging markets may be in South Africa. The ruling African National Congress, or ANC, party risks seeing support slip below the 50% mark for the first time in three decades, meaning that it may need to build a coalition with opposition parties. That could create more uncertainty for an already beleaguered economy.

In the developed world, Europe will hold parliamentary elections this summer. The debate will probably center around the Stability and Growth Pact, an agreement among European Union members to limit deficits and spending, Chang says.

Analysts at Eurasia Group don’t anticipate a populist sweep in EU elections but instead expect incumbent governments to emerge weaker, especially in Germany and France. These governments will probably have to focus on domestic issues, undermining their ability to deal with challenges like anemic economic growth and trade frictions.

One plus: In many countries heading to the polls, economies have stabilized. The Federal Reserve’s decision to pause its interest-rate hikes—and probably start cutting later in the year—offers both emerging and developed markets a supportive backdrop.

That could trump the impact on markets from domestic elections in the near term, though it might not trump the effect of Trump himself if he is elected and carries through with plans to impose steep trade barriers or alter the U.S.-Europe alliance.

Even under another Biden administration, efforts will continue to limit China’s access to markets, which could have the effect of increasing trade barriers around the world. “The free-trade movement is in full pause,” Tedford says. “When you put your China competition helmet on, there are a lot of measures that may not be supportive for the global economy.”

Write to Reshma Kapadia at reshma.kapadia@barrons.com

This Barron's article was legally licensed by AdvisorStream.

Dow Jones & Company, Inc.