By Paul R. La Monica

Aug. 12, 2024

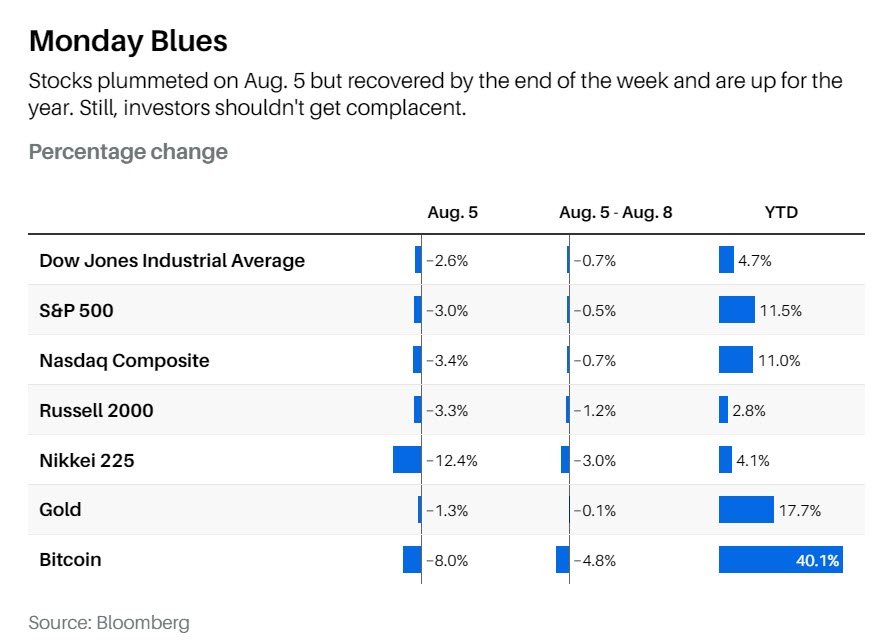

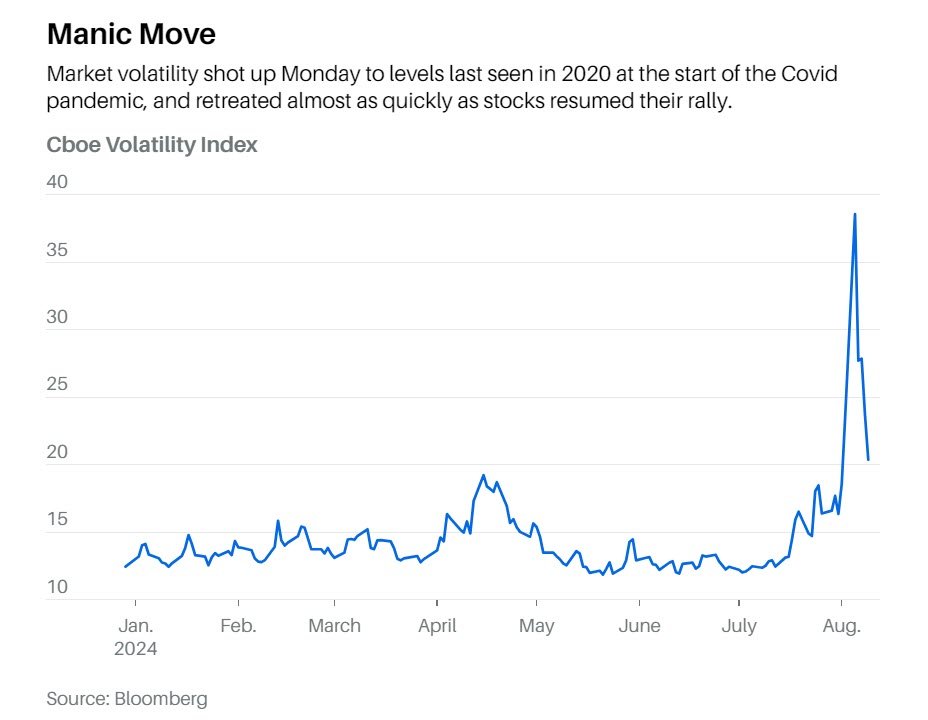

Wall Street had a wild and crazy week, marked by dramatic stock swings, currency convulsions, and a surge in stock market volatility not seen since 2020, at the beginning of the Covid pandemic. Although Monday’s trading, which cost U.S. stocks about 2.5% and Japan’s Nikkei 225 more than 12%, was a distant memory by Friday, it is hard to argue that nothing changed in the investment world.

Wall Street had a wild and crazy week, marked by dramatic stock swings, currency convulsions, and a surge in stock market volatility not seen since 2020, at the beginning of the Covid pandemic. Although Monday’s trading, which cost U.S. stocks about 2.5% and Japan’s Nikkei 225 more than 12%, was a distant memory by Friday, it is hard to argue that nothing changed in the investment world.

iStock-476307996

To the contrary, investors got a jarring wake-up call that shattered—or should have shattered—their complacency about the status quo. A weak July jobs report, released Aug. 2, suggested, along with other indicators, that the economy finally is softening after an unusually strong stretch. An uptick in Japan’s still-ultralow interest rates sparked the unwinding of a popular leveraged “carry trade” that had helped buoy numerous stocks, currencies, and other assets over the past few years.

Also, skeptics have begun to question whether artificial intelligence will deliver on the promise implied by the near-vertical rise of the market’s largest technology stocks this year. And a contentious U.S. election season and heightened global turmoil could pose more worries for the markets.

Although U.S. stocks regained nearly all the ground they lost Monday by the end of the week, it is hard to say the turmoil is over. Thus, it is a good time to get more defensive and diversify into less highly valued corners of the market than some of the so-called Magnificent Seven tech stocks and other richly priced shares.

Todd Walsh, CEO and chief technical analyst at Alpha Cubed Investments, called the past week’s developments “a perfect storm of normalization” that should remind investors that the economy inevitably will slow. Walsh argues against concentrating portfolios in just a small group of stocks, noting the market has been “myopically focused on tech and artificial intelligence.”

“Investors should step back and make sure they aren’t following the day-to-day whipsaw action of the market,” says Max Wasserman, co-founder and senior portfolio manager at Miramar Capital.

The question to ask: “Are you looking for trades, or are you investing?”

Those “looking for trades” have gotten ample opportunities so far this month. Aug. 1 brought news of a sharp contraction in U.S. manufacturing via the Institute for Supply Management, whose manufacturing index measured a disappointing 46.8 in July. The same day, a surprise jump in weekly jobless claims set off alarm bells about the economy. The Dow Jones Industrials tumbled nearly 500 points on the news, and bond yields fell sharply.

The picture darkened further the next day, when the U.S. government reported that only 114,000 new jobs were added to nonfarm payrolls in July, far below expectations. The Dow fell another 600 points as some economists and investors began to call for an emergency interest-rate cut by the Federal Reserve, which is widely expected to lower rates at its September meeting.

As Monday’s trading opened, investors were digesting the news that Warren Buffett’s Berkshire Hathaway had unloaded a big stake in Apple, the company’s top equity holding and one of the Mag Seven stocks. On the other side of the world, Japan’s benchmark stock index was in free fall after the aforementioned rate hike, even as investors who had borrowed cheaply in yen to buy U.S. tech stocks, other currencies, and perhaps Bitcoin and gold raced to undo those trades.

At Monday’s lows, the Dow had lost more than 2,300 points in just three days of trading. The S&P 500 had given up 6%, and the Nasdaq Composite had fallen firmly into correction territory with a pullback of more than 10% from its recent record high. Small-cap stocks, which had rallied in July as part of an investment rotation into companies likely to benefit from lower interest rates, also tanked.

The fear was palpable: The Cboe Volatility Index, or VIX, quickly shot up from the teens to a peak of more than 65. The 10-year Treasury yield tumbled from around 4.1% to 3.67% as investors saw safety in bonds (whose prices rise inversely to yields). Even gold, which typically thrives during times of financial uncertainty, fell about 1% on Aug. 5, while cryptocurrencies were crushed: Bitcoin lost 8%.

And then, sentiment turned on a dime. The stock market rallied Tuesday, experienced a bumpy Wednesday, and surged again on Thursday, after a decline in weekly filings for unemployment insurance suggested the job market and economy might not be losing much steam after all. By week’s end, bond yields were back to nearly 4%, and the VIX had retreated to considerably less alarming levels in the low-20s.

So, has anything changed for investors? No, and yes. Long-term investors shouldn’t be spooked by a one-day rout or the market’s churning. The S&P 500 and Nasdaq are still up more than 11% on the year, and recent news confirmed certain trends already in place, in particular a cooling labor market and a modest transition under way from the most expensive technology stocks to more cyclical sectors such as energy, financials, and industrials, and dividend-paying bond proxies such as utility stocks and consumer staples. That trend might accelerate, which would be something to welcome, not dread.

Yet, the violence of the moves in various asset prices speaks to broader changes that could lie ahead, and an underlying fragility in the markets that investors might have chosen to ignore while bidding up mostly AI-related stocks to levels that allow little margin for error.

“Be cognizant of history,” says Bill Sterling, global strategist at GW&K Investment Management. “Chasing winners isn’t a great strategy for longer-term portfolios. Don’t overlook other opportunities. If you want to diversify away from large-cap tech, look to energy, industrials, and financials.”

James Ragan, director of wealth management research at D.A. Davidson, thinks it also makes sense to take some profits in tech. “Rebalance, trim overweight positions, and add to underperformers,” he says.

Walsh, of Alpha Cubed, expects that value stocks, especially dividend payers in what he calls the Forgotten 493 of the S&P 500, will shine. And Brad Long, managing partner and chief investment officer with Fiducient Advisors, calls high-yielding utility stocks the “antithesis to the Magnificent Seven.”

Tech valuations might not be as bubblicious as in the late 1990s and early 2000s, or even earlier this year. But the indexes’ megacaps aren’t cheap. The Roundhill Magnificent Seven exchange-traded fund trades for about 32 times earnings estimates.

That type of premium might have made sense when companies outside of tech weren’t producing much in the way of growth. Yet earnings for the equal-weighted S&P 500 index are expected to rise more than 5% this year and 14% in 2025, following a tepid 1% increase in 2023. The equal-weighted index trades for 18 times 2024 earnings forecasts, compared with a P/E of 22 for the capitalization-weighted S&P.

“Earnings growth is going to broaden out to the rest of the market,” says Mike Rode, senior investment director with American Century Investments. “You will see dollars flow out of large-cap growth and redistribute to other areas that haven’t done as well.”

Valuations also look more compelling for smaller and midsize stocks. Both the S&P SmallCap 600 and S&P MidCap 400 indexes trade for just 16 times 2024 earnings estimates. These smaller stocks could thrive when the Federal Reserve cuts rates.

“Lower rates are justified by inflation pressures coming down,” says Ed Yardeni, president of Yardeni Research. “That will benefit small- and mid-caps more than large companies, since many have floating rate debt.”

The August jitters have also created better entry points in some of the Magnificent Seven stocks, such as Microsoft and Nvidia. There could be further buying opportunities ahead if the volatility persists, which seems likely. “August and September are seasonally weak months, and it could get worse,” says Phil Blancato, chief market strategist at Osaic. “But when you see a selloff in great companies, take advantage of [it].”

This month’s turmoil has already given way to more benign and less volatile trading. But don’t forget it. Stay alert to what stocks and bonds are saying about the potential macro and market changes ahead, and the dangers and opportunities that await.

This Barron's article was legally licensed by AdvisorStream.