By Nick Timiraos

Aug. 22, 2024

There’s a saying that economic expansions don’t die of old age: They’re murdered by the Federal Reserve.

Fed Chair Jerome Powell has spent the past two years determined to beat inflation even if it resulted in recession. Now he’s on the brink of winning the battle without bringing down the economy, but the next few months will be crucial.

Jerome Powell spoke at a news conference in July. Andrew Harnik/Getty Images

If he succeeds and maneuvers the economy to a soft landing that brings inflation down without a big rise in unemployment, it’ll be a historic achievement worthy of the central banking Hall of Fame. If he fails, the economy will slide into recession anyway under the weight of higher interest rates—and he’ll have proved the old maxim about the Fed.

Powell and his colleagues have signaled in recent weeks that they’re ready to start cutting rates when they next meet in September, with price pressures now easing but the jobs market cooling. That’s put attention on how fast officials should bring down rates from a two-decade high.

For Powell, the last phase of the Fed’s inflation fight marks a make-or-break moment. How he plans his approach will loom over the central bank’s annual conference in Wyoming’s Grand Teton National Park this week, including during a widely anticipated speech on Friday.

When Powell spoke there two years ago amid doubts over the Fed’s conviction to bring down inflation, he delivered a somber promise. He signaled his readiness to accept a recession as the price of curing high inflation by invoking the example of former Fed Chair Paul Volcker. In the early 1980s, the Fed famously ratcheted rates to very high levels and put the economy through a wrenching downturn that ultimately tamed high prices.

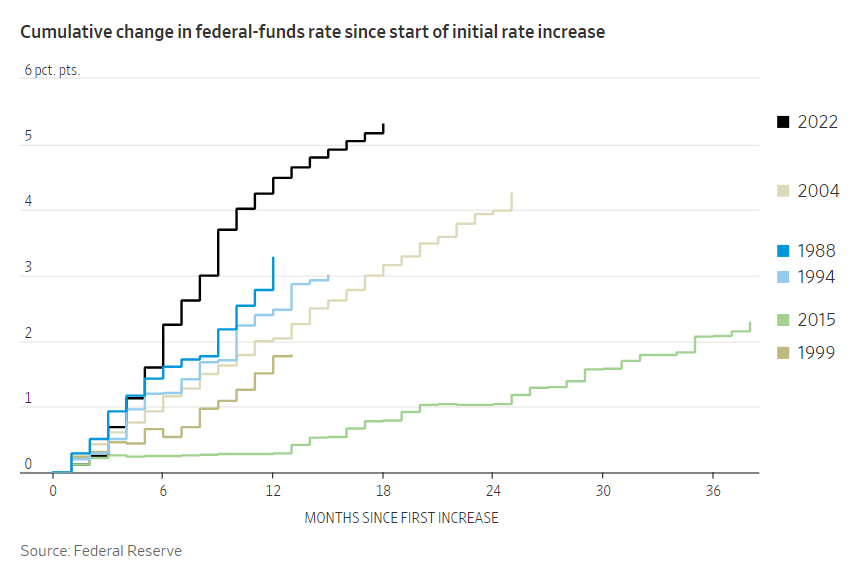

The Fed under Powell also raised rates rapidly, in 2022 and 2023. Still, Powell has held on to the possibility that the Fed might be able to avoid a recession this time around because the inflation of 2021-23 was different from the 1970s episode.

For Fed officials, sticking a soft landing would offer the ultimate redemption. Three years ago, they had incorrectly predicted inflation would be short lived. Success would illustrate that the costs of being slow to end aggressive stimulus policies in 2021 weren’t as disastrous as many critics warned.

“It would be the finest moment in their history,” said Dario Perkins, an economist at GlobalData TS Lombard. “They could say, ‘We not only prevented this 1970s runaway-inflation scenario, but we’ve managed to do it with no meaningful cost to the economy—this perfect soft landing.’”

In doing so, Powell has the chance to emulate two of his heroes. A successful outcome would marry the fortitude of Volcker with the deftness of Alan Greenspan, who as Fed chair in the late 1990s resisted calls to slow the economy amid a boom that yielded little inflation.

‘Bad karma’

Powell is navigating against the backdrop of a divisive election campaign, and the Fed’s decisions could shape the economy the next president inherits.

Democrats including Massachusetts Sen. Elizabeth Warren have criticized Powell for not having cut rates sooner. They make no secret they’ll blame any economic downturn on Powell.

Donald Trump, who appointed Powell as chair in 2018, says he wants a greater say in interest-rate policy if he recaptures the presidency this fall. A recession could embolden the GOP nominee in his quest to mold the institution to his liking.

Much could still go wrong, something Powell knows well. Slamming into or skidding off the runway is something the mild-mannered Fed chair has said keeps him up at night. Powell, 71, refrains from using the “soft landing” term, according to people who have worked or spoken with him, to avoid sounding like he has counted his chickens before they hatch. Instead, he’ll refer to it obliquely as “the good outcome” or “that thing we all want.”

He’s not alone. “I try not to use the phrase. It’s bad karma,” said Tom Barkin, president of the Richmond Fed, in an interview last week.

The Fed chief—who after college traveled through Europe with his guitar, serenading patrons at a Paris cafe with Hank Williams ballads including “I’m So Lonesome I Could Cry”—said recently he and his wife have stopped dining at restaurants. “People at the next table are always listening,” he told a lunchtime audience of a few hundred businesspeople in Washington last month.

The economic script has flipped

Worries about the labor market have raised questions about how quickly to cut rates.

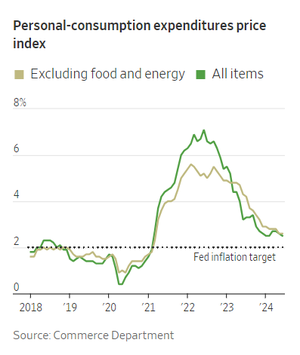

Inflation has fallen to around 2.5% from above 7% two years ago, not far from the Fed’s 2% target. But the unemployment rate climbed to 4.3% in July from 3.7% at the beginning of the year. While that’s a historically low level, it won’t necessarily stay there. Usually when the unemployment rate starts rising a little bit, it subsequently rises by a lot. That line of thinking argues for lowering rates with reasonable speed.

Yet some officials are nervous that rate cuts will stoke new price pressures that jeopardize their hard-won gains.

The U.S. economy has defied rolling predictions of imminent recession, powering through higher rates over the last two years. Now evidence is gathering that unique buffers that shielded the economy so far, including pandemic-era savings cushions and an immigration surge that boosted spending, could be fading along several fronts.

Low- and middle-income consumers’ budgets are showing strains. More companies say they’re focusing again on keeping costs down to attract deal-conscious shoppers.

The U.S. housing sector, which avoided a downturn that usually occurs when interest rates rise sharply, faces a bleak outlook. Today’s pool of would-be buyers have weaker income and wealth profiles than those who stepped up to buy homes when mortgage rates first soared above 6% two years ago.

Many homeowners have held their homes off the market, which initially limited competition for home builders. That’s ending now as inventories are rising. Meanwhile, an apartment building boom that kept construction workers on job sites is over. The number of housing units under construction has fallen nearly 10% over the past year, the largest such decline since 2011.

In the labor market, companies have slowed hiring. For now, layoffs are low. But what looks like a controlled demolition of labor demand risks moving past a tipping point. The Labor Department said Wednesday that payroll growth for the 12 months ending in March could be revised down to 2.1 million jobs from an initially reported figure of nearly three million jobs, meaning job gains for most of 2023 and the first three months of this year were milder.

“If job openings fall a lot more, people who lose their jobs are not going to be able to walk across the street and find work,” said Peter Berezin, chief global strategist at BCA Research.

Sticking the landing

Many downturns look like soft landings at first, but since World War II, the U.S. has convincingly achieved only one, in 1995. Back then, Greenspan attempted to pre-empt inflationary pressures by raising rates rapidly, from 3% to 6%. He then reversed course and over six months cut rates to 5.25%.

Whether Powell manages the feat depends not only on whether the economy is weakening under the surface faster but also whether lower rates can spur new borrowing and spending to counteract any softness.

Investors are optimistic because the Fed has plenty of room to cut. Still, some borrowers could face a squeeze from the lagged effects of the Fed’s past hikes even after the central bank reduces borrowing costs.

That’s because borrowers enjoyed more than a decade of historically very low borrowing costs before the Fed started raising rates, and many firms and households still have low fixed-rate debt. If that debt matures in the next year, they could face a sizable increase in borrowing costs even if the Fed cuts rates by a full percentage point.

A soft landing seems tantalizingly close because the economy so far has hewed closer to an optimistic scenario Fed officials outlined two years ago.

When officials began lifting rates from near zero in 2022, prominent economists said a period of higher unemployment was almost required to create enough slack—such as unemployed workers and idled factories—to lower prices. They argued inflation was being driven by overheated labor markets.

Fed leaders said another path was possible because inflation had been driven not by the labor market but by the collision between strong demand and discombobulated supply chains. They suggested the labor market was so out of whack after the pandemic, as reopening businesses scrambled to hire workers, that cooling demand might lead firms to simply scrap unfilled openings rather than fire workers.

Good luck has played a part in that outcome. Supply chains healed last year. The economy avoided new shocks, such as a sharp rise in oil prices or a financial-market blowup. And a surge in immigration boosted output while alleviating worker shortages. “We know more now about where this [inflation] came from because we can see what made it go away,” Powell told lawmakers last month.

Earlier this year, as economists puzzled over why interest rates hadn’t done more to slow the economy, Powell suggested that the immigration surge might have masked the effects of tight interest-rate policy. His underlying concern was that the effects of restrictive policy would reveal themselves gradually and then suddenly.

‘What’s the rush?’ vs. ‘Why are we waiting?’

Inside the Fed, the economic uncertainty threatens to end a period of unanimity that is remarkable even for a committee that prizes consensus. No Fed officials have dissented at a policy meeting since June 2022, matching a streak last seen between 2003 and 2005.

One camp that includes Fed governor Michelle Bowman and Kansas City Fed President Jeff Schmid worries cutting rates too soon will reignite inflation or allow it to settle out closer to 3%—well above their target. With the unemployment rate at a historically low level, this group has argued, “What’s the rush?”

This group has also reacted skeptically to pessimism about the labor market. They point to how the recent uptick in the unemployment rate has been driven by temporary and not permanent layoffs along with an increase in the number of people entering the job market. They think interest rates are only moderately restrictive, meaning the Fed may not need to cut rates very much.

Another camp is more anxious about growing too complacent about the slowdown in labor demand. Inflation-adjusted interest rates are at their highest level in decades, and these officials are asking, “Why are we waiting?”

“In regular business cycles, unemployment goes up like a rocket but comes down like a feather,” said Chicago Fed President Austan Goolsbee in an interview. While the current cycle might be unusual, “it’s at least a note of caution that the job market has been cooling. It needs to stop cooling.”

Many are ready to start cutting rates by a traditional quarter-percentage-point next month but aren’t sure how fast they should go thereafter. At issue is the question over how far rates currently sit above a “neutral” setting that neither spurs nor slows activity.

At the September meeting, Fed officials will have to fill out their projections for interest rates for the next three years. Minneapolis Fed President Neel Kashkari is dreading it because he’s so uncertain “about how tight policy is right now,” he said in an interview.

Barkin said he and his Richmond Fed staff canvass hundreds of businesses to see if demand is weakening and whether they are preparing to lay off workers as a result. He isn’t seeing it outside of a few narrow sectors. “You can make mistakes by moving too aggressively or not aggressively enough,” he said.

Broadly speaking, the Fed faces two paths for the coming months. Under one, officials could cut rates by a quarter-point at each of their next few meetings and then dial up or down the size and speed of reductions depending on how the economy fares early next year.

If the economy enters a sharper slowdown, they could cut rates in larger half-point increments to get interest rates closer to 3% by next spring. (The Fed’s benchmark rate is currently set between 5.25% and 5.5%.)

Powell is likely to keep his options open when he speaks this week. Labor market data for August, to be released early next month, could tip the scales in favor of a larger cut if it is as disappointing as July’s readings.

“The reason you move gradually as a central banker is it gives you optionality,” said Goolsbee. “The downside of gradualism is that when things move, you don’t have that luxury anymore.”

A handful of private-sector and former Fed economists, including at JPMorgan Chase and Wells Fargo, say evidence that the labor market might be weakening too much should lead officials to make larger rate cuts upfront, shedding their longstanding preference for gradualism.

“They’ve got a lot of wood to chop, and they need to get going. But it’s a very consensus-driven place, and they don’t have the consensus yet to do that,” said Jay Bryson, chief economist at Wells Fargo. That looks unlikely to happen on this committee without “a shock or a run of weak data that suddenly shifts the consensus to where they move faster.”

Write to Nick Timiraos at Nick.Timiraos@wsj.com

Dow Jones & Company, Inc.