By Joe Pinsker and Veronica Dagher

Aug. 14, 2024

Millennials are now wealthier than previous generations were at their age. They can’t believe it either.

Fifteen years ago, Andy Holmes was a college graduate living with his parents, mowing lawns and digging ditches for extra income. He and his college pals who could only get low-paid jobs wondered if they would have a shot at the success their parents had.

Today, Holmes is a chief financial officer in Kansas City, Mo., on track to retire at 52.

“I’m in a place financially that I couldn’t have imagined coming out of college,” he said. “At age 37, my net worth is closer to what I thought it’d be at 47.”

Older millennials like Christian Hutchinson and Becky Wang have come into their own in recent years. PHOTO: Sylvia Jarrus for WSJ

The change in fortune for Holmes’s generation, now between 27 and 44 years old, was recent and swift.

The median household net worth of older millennials, born in the 1980s, rose to $130,000 in 2022 from $60,000 in 2019, according to inflation-adjusted data from the Federal Reserve Bank of St. Louis. Median wealth more than quadrupled to $41,000 for Americans born in the 1990s, which includes the generation’s youngest members, born in 1996.

The turnaround has been so dramatic that millennials—mocked at times for being perpetually behind in building wealth, buying homes, getting married and having children—now find themselves ahead.

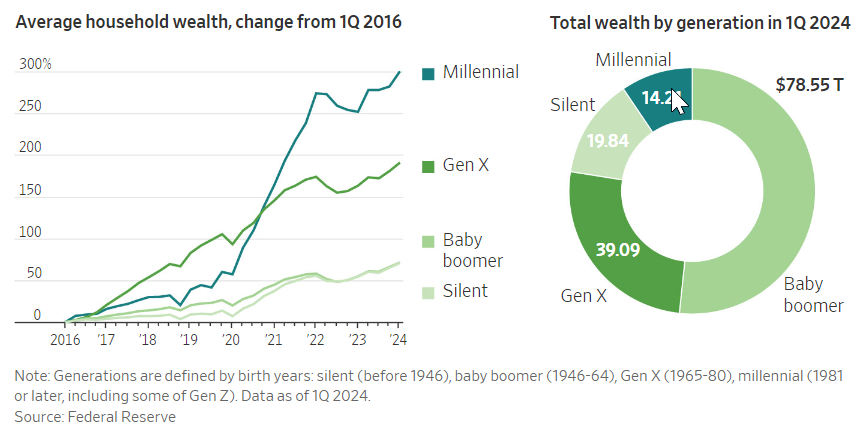

In early 2024, millennials and older members of Gen Z had, on average and adjusting for inflation, about 25% more wealth than Gen Xers and baby boomers did at a similar age, according to a St. Louis Fed analysis.

Ana Hernández Kent, a senior researcher at the St. Louis Fed and a millennial herself, spent years examining whether her cohort was a “lost generation.”

“They’re no longer lost,” she said. “They’re found.”

In the first quarter of 2024, the collective wealth of millennials and older Gen Z stood at $14.2 trillion, up from $4.5 trillion four years earlier, according to the Federal Reserve.

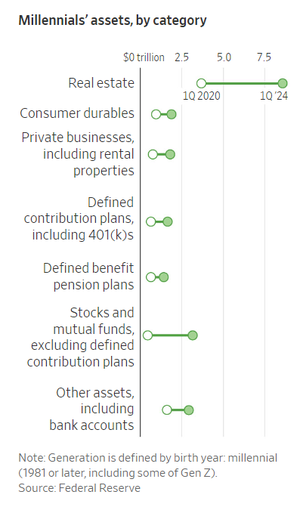

The biggest driver of that increase was real estate. Millennials’ housing wealth grew $2.5 trillion, after accounting for the additional mortgage debt they took on. A colossal jump in home prices benefited owners, whether they scraped together a down payment in the early 2010s or squeaked in just before the recent leap in prices and rates.

Stocks and mutual funds also played a key role, in part because many employees made larger contributions to retirement accounts earlier in their careers.

Inequalities remain, and in many instances have grown. In addition to disparities along racial and educational lines, millennials’ fates diverge based on whether they are burdened by student debt, can buy a home or live in an expensive area.

It’s unclear if millennials are better off overall, given the outsize increases in some of the most burdensome costs, such as child care, housing and healthcare. They’re also projected to live longer than Boomers, so they’ll need to make their money last.

As a group, though, they have traits that point to long-term prosperity, economists say. More have college degrees, which boost income. And they are having fewer children, which, whatever the effects on the country, is a boon to budgets.

Two early decisions helped set Holmes up for a better financial future. Moving back home after college allowed him to save for a down payment. He ended up purchasing a three-bedroom for $90,000 in 2010. That home is now worth about $300,000.

“I have to pat Andy from 2010 on the back,” he said.

In 2017, Holmes put a chunk of money into the stock market, which later yielded a gain in the high five-figures. The windfall, combined with a lucrative job switch, made it easier for his wife, Megan Holmes, to quit her job. She now looks after their two young children full-time.

How they’re spending

Brent Royer got a 40% raise when he switched jobs in 2021, giving him the funds to invest more in his passion, skydiving.

The 36-year-old accountant makes weekly trips to a wind tunnel near his home in San Diego and last year took part in a record-setting jump where 108 participants assumed three different formations midair.

Royer estimates he spent about $40,000 on skydiving in 2023, including parachutes, custom-made jumpsuits and “lift tickets” on planes.

He saves diligently, but doesn’t want to miss out by socking away any more than he needs to.

“We don’t know how long we will have in this life, so I want to ensure that I’m enjoying it now,” he said.

Some 62% of millennials say vacations are a high priority in their household, compared with 54% of adults overall, according to Mintel, a market-research firm. They are also more likely to have paid for a luxury travel experience.

The generation’s approach to leisure is informed by witnessing the 2007-09 recession in their formative years, said Mike Gallinari, a senior analyst at Mintel.

“They realized they can lose their stuff to forces outside their control,” he said. “But nobody can take their memories from them.”

Phantom wealth

Overall, millennials hold about 9% of U.S. households’ wealth. That might seem small, but net worths tend to swell with age, meaning that increases work out to bigger percentage gains for younger generations that have yet to build up significant wealth.

Roughly 66% of Americans aged 30 to 44 said in 2023 they were doing at least OK financially, up from 55% a decade earlier, according to a Fed survey.

For many, success feels fragile.

On paper, Becky Wang and Christian Hutchinson of Grosse Pointe Shores, Mich., are thriving. The married couple, both 40, have stable jobs, a sub-4% mortgage and nine rental properties.

“My wife and I are much more scared of failure in 2024 than 2014,” Hutchinson said. “Once you have something to lose, you get soft oftentimes.”

Hutchinson, a business analyst, was born in Detroit and watched the area shed jobs as he grew up. Wang moved there in adulthood after emigrating from China at 14, and her awareness of how quickly luck can turn comes from treating cancer patients as a nurse.

The couple started scooping up rental properties in 2013, when prices were low around the time the city of Detroit filed for bankruptcy. To diversify, they are contemplating buying a laundromat or an online retail business. Both also want to have side gigs.

“Deep down, we kind of fear that one day things can fall apart,” Wang said.

That feeling isn’t uncommon in their generation, according to Taylor Leary, a financial planner in Greenwood Village, Colo., whose practice focuses on millennials.

Gains in the value of a home or 401(k) can feel like phantom wealth because they are illiquid and have no bearing on day-to-day cash flow. Meanwhile, millennials are experiencing the weight of big-ticket items such as daycare.

They may also have memories of a parent losing a job during the 2007-09 recession, graduating college in a tough job market or, more recently, fumbling through the uncertainty of the Covid-19 pandemic.

“It’s almost like many millennials are looking over their shoulder waiting for something to happen,” said Leary.

Growing gaps

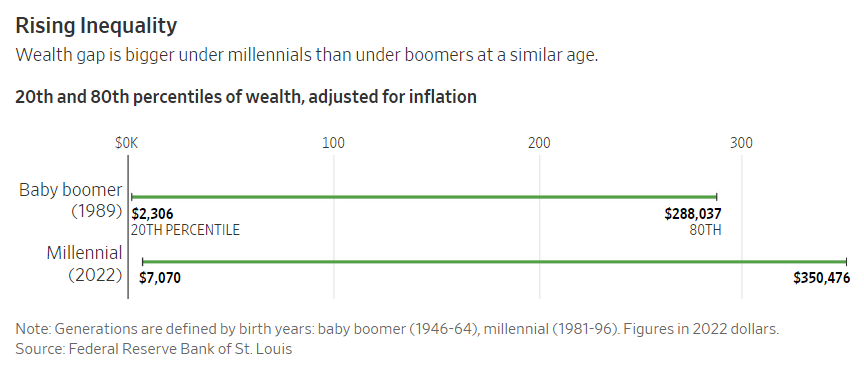

As successful as this generation has been overall, wealth inequality has widened among millennials compared with their predecessors.

The gap between the 80th percentile of wealth and the 20th percentile of wealth for millennials was about $343,000 in 2022, according to the St. Louis Fed. Adjusting for inflation, that gap was about $286,000 for Boomers when they were a similar age in 1989.

One explanation is that the payoffs for white-collar work grew during that period, while those for working-class jobs stagnated, according to a 2023 study in the American Journal of Sociology. Another crucial divide: homeownership.

Older millennials’ homeownership rate recently caught up with that of previous generations, rising to around 60% between 2019 and 2022, according to the St. Louis Fed. Meanwhile, only about 39% of Americans born in the 1990s owned a home in 2022.

Black millennials are half as likely to own a home as white millennials, the largest gap of any generation, according to Redfin. Low-income Americans are also losing out. About 8% of new mortgages went to low-income buyers ages 25 to 34 in 2023, down from 9% in 2020, Redfin found.

Saving for a home and retirement feels like a far-off goal for many, especially millennials who aren’t high earners. It takes an annual household income of at least $100,000 to afford the median-priced home in nearly half of all metro areas, according to Harvard University’s Joint Center for Housing Studies. A job loss or medical bills can postpone the ability to save and buy a home even longer.

Deanna Fuller, 40, and her husband Marc Fuller, 42, both make more money than they did before the pandemic, but their budget remains tight thanks to inflation.

The Salt Lake City, Utah, couple earns about $89,000 a year from her work in the back office of a financial-services firm and his job in a warehouse distribution center. After $1,300 in rent for their 800-square-foot apartment and other expenses such as food and transportation, they’re able to save about $200 a month.

Medical bills wiped out most of their savings, she said, and they haven’t been able to stock much away in retirement accounts.

After recent pay raises, the Fullers’ first priority is to build on the roughly $3,000 they have saved for emergencies and then save for a down payment.

“Maybe we’ll be able to buy a house when we’re 50,” Deanna Fuller said.

Strong foundation

Many who bought homes before the pandemic are sitting pretty, even with rising insurance premiums and property taxes in some parts of the U.S.

“One of the biggest wealth divides, especially for millennials, is did you buy a house in 2020 or before, or after? Or not at all?” said Jean Twenge, a psychology professor at San Diego State University who has been studying generational differences for decades and wrote several books on the subject.

Existing home prices are up 19% adjusted for inflation nationwide since June 2020, according to the National Association of Realtors. The average home equity among owners with mortgages increased $122,900 over the past four years, according to CoreLogic.

Some millennials attribute their good housing fortune to careful financial planning. Others chalk it up to luck.

Justin Moorhead, 37, and his wife, Natalie Sheppard, 38, bought their 1,500-square-foot A-frame Nashville home for around $215,000 in 2016.

They had been renting a two-bedroom, 900-square-foot apartment when their rescue dog Scarlett started loudly barking anytime she saw other dogs in the complex’s hallways. They wanted to give the 45-pound collie-mix more room to play and calculated their monthly mortgage payment would be less than their rent.

Their house is worth about $500,000 today, and they owe around $165,000 on their roughly 4% mortgage.

“It’s not lost on us that we made the best financial decision of our lives so far just because we wanted a lawn for our dog,” said Moorhead.

Good timing

While soaring home prices play a large role in prosperous millennials’ finances, there are other factors working in their favor—high among them the rising value of retirement funds.

Millennials had an average 401(k) account balance of $59,800 in the first quarter of 2024 compared with $27,600 in 2019, according to Fidelity.

Good timing helped here, too.

Millennials were the first generation to have access to automatic enrollment in workplace plans during their early working years, said Matt Brancato, chief client officer in Vanguard Institutional Investor Group.

In 2006, 57% of employees aged 25 to 40 were enrolled in workplace retirement plans in which Vanguard was the record-keeper. In 2022, 83% were enrolled.

Vanguard estimates older millennials with median incomes will be able to replace almost 60% of their preretirement income with Social Security and savings from 401(k)s, individual retirement accounts and other sources. The youngest Boomers with median earnings are, by contrast, likely to replace about half of their paychecks in retirement.

Adam Chen and Margeaux Anderson started contributing to 401(k) plans in their early 20s. The Denver couple has switched jobs several times in the technology field and now have about $800,000 invested, mostly in their 401(k)s.

Chen, 40, and Anderson, 34, like to live below their means. They grow their own lettuce, cook at home frequently and prefer free activities such as hiking.

“We don’t want to have to work forever,” Chen said.

Write to Joe Pinsker at joe.pinsker@wsj.com and Veronica Dagher at Veronica.Dagher@wsj.com

Dow Jones & Company, Inc.