Troy Segal

July 9, 2024

What Is a Roth IRA?

A Roth IRA is a type of tax-advantaged individual retirement account to which you can contribute after-tax dollars toward your retirement. The primary benefit of a Roth IRA is that your contributions and the earnings on those contributions can grow tax-free and be withdrawn tax-free after age 59½, assuming the account has been open for at least five years. In other words, you pay taxes on money going into your Roth IRA, and then all future withdrawals are tax-free.

Roth IRAs are similar to traditional IRAs, with the biggest distinction being how the two are taxed. Roth IRAs are funded with after-tax dollars. Unlike a traditional IRA, the contributions are not tax-deductible, but once you start withdrawing funds, the money you take out is tax-free.

KEY TAKEAWAYS

- A Roth IRA is a special individual retirement account (IRA) where you pay taxes on money going into your account, and then all future withdrawals are tax free.

- Roth IRAs are best when you think your marginal taxes will be higher in retirement than they are right now.

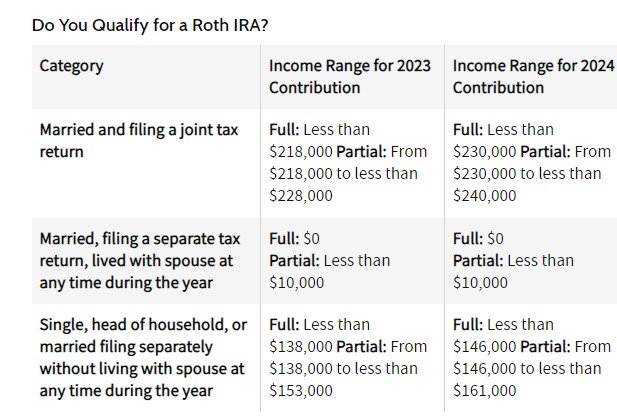

- Single filers can’t contribute to a Roth IRA if they earned more than $153,000 in 2023. For married couples filing jointly, the limit is $228,000 for 2023. In 2024, the contribution limits increase to $161,000 and $240,000, respectively.

- The amount that you can contribute changes periodically. In 2023, the limit increased to $6,500 (plus the additional $1,000 for those 50 and older). In 2024, the limit increases again to $7,000 with the catch-up contribution remaining at $1,000.

- Almost all brokerage firms, both brick-and-mortar and online, offer a Roth IRA. So do most banks and investment companies.

Tara Anand / Investopedia

How Does a Roth IRA Work?

You can put money you've already paid taxes on into a Roth IRA. It will then grow, and when you come to withdraw once you retire, you won't have to pay any further taxes.

A Roth IRA can be funded from a number of sources:

- Regular contributions

- Spousal IRA contributions

- Transfers

- Rollover contributions

- Conversions

All regular Roth IRA contributions must be made in cash (which includes checks and money orders)—they can’t be in the form of securities or property. The Internal Revenue Service (IRS) limits how much can be deposited annually in any type of IRA, adjusting the amounts periodically. The contribution limits are the same for traditional and Roth IRAs. These limits apply across all your IRAs, so even if you have multiple accounts you can't contribute more than the maximum.

Similar to other qualified retirement plan accounts, the money invested within the Roth IRA grows tax-free. However, a Roth IRA is less restrictive than other accounts. The account holder can maintain the Roth IRA indefinitely. There are no required minimum distributions (RMDs) during their lifetime, as there are with 401(k)s and traditional IRAs.

Conversely, traditional IRA deposits are generally made with pretax dollars. You usually get a tax deduction on your contribution and pay income tax when you withdraw the money from the account during retirement.

Allowable Investments in a Roth IRA

Once the funds are contributed, a variety of investment options exist within a Roth IRA, including mutual funds, stocks, bonds, exchange-traded funds (ETFs), certificates of deposit (CDs), and money market funds.

Note that IRS rules don't allow the contribution of cryptocurrency directly to your Roth IRA. However, the recent emergence of “Bitcoin IRAs” has created retirement accounts designed to let you invest in cryptocurrencies indirectly. The IRS also lists other assets that are not permitted within an IRA, such as life insurance contracts and derivative trades.

If you want the broadest range of investment options, you need to open a Roth self-directed IRA (SDIRA), a special category of Roth IRA in which the investor, not the financial institution, manages their investments. These unlock a universe of possible investments, including directly investing in digital assets.

In addition to the standard investments (stocks, bonds, cash, money market funds, and mutual funds), you can hold assets that aren’t typically part of a retirement portfolio. Some of these include gold, investment real estate, partnerships, and tax liens—even a franchise business.

$7,000

The maximum annual contribution that an individual can make to a Roth IRA in 2024. People ages 50 and older can contribute up to $8,000. The maximum is up from $6,500 in 2023 (those 50 and older can contribute up to $7,500).

Opening a Roth IRA

A Roth IRA must be established with an institution that has received IRS approval to offer IRAs. These include banks, brokerage companies, federally insured credit unions, and savings and loan associations. Generally, individuals open IRAs with brokers.

A Roth IRA can be established anytime. However, contributions for a tax year must be made by the IRA owner’s tax-filing deadline, which is normally April 15 of the following year.

Two basic documents must be provided to the IRA owner when an IRA is established:

- The IRA disclosure statement

- The IRA adoption agreement and plan document

These provide an explanation of the rules and regulations under which the Roth IRA must operate, and they establish an agreement between the IRA owner and the IRA custodian/trustee.

Not all financial institutions are created equal. Some IRA providers have an expansive list of investment options, while others are more restrictive. Almost every institution has a different fee structure for your Roth IRA, which can have a significant impact on your investment returns.

Your risk tolerance and investment preferences will play a role in choosing a Roth IRA provider. If you plan on being an active investor and making lots of trades, you want to find a provider that has lower trading costs. Certain providers even charge you an account inactivity fee if you leave your investments alone for too long. Some providers have more diverse stock or ETF offerings than others; it all depends on what type of investments you want in your account.

Pay attention to the specific account requirements as well. Some providers have higher minimum account balances than others. If you plan on banking with the same institution, see if your Roth IRA account comes with additional banking products. If you’re looking at opening a Roth IRA at a bank or brokerage where you already have an account, see whether existing customers receive any IRA fee discounts.

Most IRA providers offer only regular IRA (traditional or Roth) accounts. For a self-directed IRA, you’ll need a qualified IRA custodian that specializes in that type of account, which allows assets beyond the typical stocks, bonds, ETFs, and mutual funds.

Are Roth IRAs Insured?

If your account is located at a bank, be aware that IRAs fall under a different insurance category from conventional deposit accounts. Therefore, coverage for IRA accounts is not as robust. The Federal Deposit Insurance Corp. (FDIC) still offers insurance protection up to $250,000 for traditional or Roth IRA accounts, but account balances are combined rather than viewed individually.

For example, if the same banking customer has a CD held within a traditional IRA with a value of $200,000 and a Roth IRA held in a savings account with a value of $100,000 at the same institution, then the account holder has $50,000 of vulnerable assets without FDIC coverage.

What Can You Contribute to a Roth IRA?

The IRS dictates not only how much money you can deposit in a Roth IRA, but also the type of money that you can deposit. Basically, you can only contribute earned income to a Roth IRA.

For individuals working for an employer, compensation that is eligible to fund a Roth IRA includes wages, salaries, commissions, bonuses, and other amounts paid to the individual for the services that they perform. It’s generally any amount shown in Box 1 of the individual’s Form W-2. For a self-employed individual or a partner or member of a pass-through business, compensation is the individual’s net earnings from their business, less any deduction allowed for contributions made to retirement plans on the individual’s behalf and further reduced by 50% of the individual’s self-employment taxes.

Money related to divorce—alimony, child support, or in a settlement—can also be contributed if it is related to taxable alimony received from a divorce settlement executed prior to Dec. 31, 2018.

So, what sort of funds aren’t eligible? The list includes:

- Rental income or other profits from property maintenance

- Interest income

- Pension or annuity income

- Stock dividends and capital gains

- Passive income earned from a partnership in which you do not provide substantial services

You can never contribute more to your IRA than your earned income in that tax year. And as previously mentioned, you receive no tax deduction for the contribution—although you may be able to take a Saver's Tax Credit of 10%, 20%, or 50% of the deposit, depending on your income and life situation.

Who’s Eligible for a Roth IRA?

Anyone who has earned income can contribute to a Roth IRA—as long as they meet certain requirements concerning filing status and modified adjusted gross income (MAGI). Those whose annual income is above a certain amount, which the IRS adjusts periodically, become ineligible to contribute. The chart below shows the figures for 2023 and 2024.

Internal Revenue Service. "401(k) Limit Increases to $23,000 for 2024, IRA Limit Rises to $7,000."

Here’s how the system works: An individual who earns less than the ranges shown for their appropriate category can contribute up to 100% of their compensation or the contribution limit, whichever is less.

Individuals within the phaseout range must subtract their income from the maximum level and then divide that by the phaseout range to determine the percentage that they are allowed to contribute.

The Spousal Roth IRA

One way that a couple can boost their contributions is the spousal Roth IRA. An individual may fund a Roth IRA on behalf of their married partner who earns little or no income. Spousal Roth IRA contributions are subject to the same rules and limits as regular Roth IRA contributions. The spousal Roth IRA is held separately from the Roth IRA of the individual making the contribution, as Roth IRAs cannot be joint accounts.

For an individual to be eligible to make a spousal Roth IRA contribution, the following requirements must be met:

- The couple must be married and file a joint tax return.

- The individual making the spousal Roth IRA contribution must have eligible compensation.

- The total contribution for both spouses must not exceed the taxable compensation reported on their joint tax return.

- Contributions to one Roth IRA cannot exceed the contribution limits for one IRA (however, the two accounts allow the family to double their annual savings).

Withdrawals: Qualified Distributions

At any time during the tax year, you may withdraw contributions from your Roth IRA, both tax- and penalty-free. If you take out only an amount equal to the sum that you’ve put in, then the distribution is not considered taxable income and is not subject to penalty, regardless of your age or how long it has been in the account.

However, there’s a catch when it comes to withdrawing account earnings—any returns that the account has generated. For distribution of account earnings to be considered a qualified distribution, it must occur at least five years after the Roth IRA owner established and funded their first Roth IRA, and the distribution must occur under at least one of the following conditions:

- The Roth IRA holder is at least age 59½ when the distribution occurs.

- The distributed assets are used toward purchasing—or building or rebuilding—a first home for the Roth IRA holder or a qualified family member (the IRA owner’s spouse, a child of the IRA owner or of the IRA owner’s spouse, a grandchild of the IRA owner and/or of their spouse, or a parent or other ancestor of the IRA owner or of their spouse). This is limited to $10,000 per lifetime.

- The distribution occurs after the Roth IRA holder becomes disabled.

- The assets are distributed to the beneficiary of the Roth IRA holder after the Roth IRA holder’s death.

The Five-Year Rule

Withdrawal of earnings may be subject to taxes and/or a 10% penalty, depending on your age and whether you’ve met the five-year rule. Here’s a quick rundown.

If you meet the five-year rule:

- Under age 59½: Earnings are subject to taxes and penalties. You may be able to avoid taxes and penalties if you use the money for a first-time home purchase (a $10,000 lifetime limit applies) or if you have a permanent disability. If you pass away and your beneficiary takes the distribution, taxes and penalties may also be avoided.

- Ages 59½ and older: There are no taxes or penalties.

If you don’t meet the five-year rule:

- Under age 59½: Earnings are subject to taxes and penalties. You may be able to avoid the penalty (but not the taxes) if you use the money for a first-time home purchase (a $10,000 lifetime limit applies), qualified education expenses, unreimbursed medical expenses, if you have a permanent disability, or if you pass away and your beneficiary takes the distribution.

- Ages 59½ and older: Earnings are subject to taxes but not penalties.

Important: Roth IRA withdrawals are made on a first in, first out (FIFO) basis—so any withdrawals made come from contributions first. Therefore, no earnings are considered touched until all contributions have been taken out.

Withdrawals: Non-Qualified Distributions

A withdrawal of earnings that do not meet the above requirements is considered a non-qualified distribution and may be subject to income tax or a 10% early distribution penalty. There may be exceptions, however, if the funds are used:

- For unreimbursed medical expenses: If the distribution is used to pay unreimbursed medical expenses for amounts that exceed 7.5% of the individual’s adjusted gross income (AGI).

- To pay medical insurance: If the individual has lost their job.

- For qualified higher education expenses: If the distribution goes toward qualified higher education expenses of the Roth IRA owner and/or their dependents. These qualified expenses are tuition, fees, books, supplies, and equipment required for the enrollment or attendance of a student at an eligible educational institution and must be used in the year of the withdrawal.

- For childbirth or adoption expenses: If they're made within one year of the event and don't exceed $5,000.

Note that if you withdraw only the amount of your contributions made within the current tax year—including any earnings on those contributions—then the contribution is reversed. For example, if you contribute $5,000 in the current year and those funds generate $500 in earnings, you can withdraw the $5,000 principal tax- and penalty-free and the $500 gain will be treated as taxable income.

Coronavirus-Related Distributions

A special provision in the Coronavirus Aid, Relief, and Economic Security (CARES) Act allowed taxpayers to take a coronavirus-related distribution from Jan. 1, 2020, to Dec. 31, 2020, up to an aggregate $100,000 from all qualified plans and IRAs. The coronavirus-related distribution could be taken by a qualified individual, defined by the IRS as someone who was negatively affected by coronavirus—either financially or through a family diagnosis. Retirement plan owners who qualified for coronavirus-related distributions included those:

- Diagnosed with SARS-CoV-2

- Whose spouse or dependent was diagnosed with SARS-CoV-2

- Who were financially impacted due to furlough, quarantine, layoff, or reduced work hours during the pandemic

- Who were unable to work due to lack of childcare during the pandemic

- Who were financially impacted due to the reduction of business hours or closure of their own business during the pandemic

The special provision allowed the retirement account holder to take the distribution as a standard withdrawal with no repayment or as a loan with a repayment option. The distribution was exempt from the 10% early distribution penalty but was taxed as ordinary income. The CARES Act allowed the withdrawal to be taxed as ordinary income in full in 2020 or over a three-year period in 2020, 2021, and 2022. Those who took advantage of this provision had until the end of the third year to pay back the funds.

For example, let’s assume that you withdrew $15,000 in 2020. You would need to claim $5,000 on your tax returns in 2020 and 2021. If you repaid the funds in full in 2022, then you would not have needed to pay taxes on the final $5,000. Additionally, you will need to file an amended return for 2020 and 2021 to recoup your taxes previously paid on the first two-thirds.

Roth IRA vs. Traditional IRA

Whether a Roth IRA is more beneficial than a traditional IRA depends on the tax bracket of the filer, the expected tax rate at retirement, and personal preference.

Individuals who expect to be in a higher tax bracket once they retire may find the Roth IRA more advantageous since the total tax avoided in retirement will be greater than the income tax paid in the present. Therefore, younger and lower-income workers may benefit the most from a Roth IRA.

Indeed, by beginning to save with an IRA early in life, investors make the most of the snowballing effect of compound interest: Your investment and its earnings are reinvested and generate more earnings, which are reinvested, and so on.

Of course, even if you expect to have a lower tax rate in retirement, you’ll still enjoy a tax-free income stream from your Roth IRA. That’s not the worst idea in the world.

Those who don’t need their Roth IRA assets in retirement can leave the money to accrue indefinitely and pass the assets to heirs tax-free upon death. Even better, while the beneficiary must take distributions from an inherited IRA, they can stretch out tax deferral by taking distributions for a decade—and, in some specialized cases, for their lifetimes.

Traditional IRA beneficiaries, on the other hand, do pay taxes on the distributions. Also, a spouse can roll over an inherited IRA into a new account and not have to begin taking distributions until age 73.

Some open or convert to Roth IRAs because they fear an increase in taxes in the future, and this account allows them to lock in the current tax rates on the balance of their conversions. Executives and other highly compensated employees who are able to contribute to a Roth retirement plan through their employers—for example, via a Roth 401(k)—can also roll these plans into Roth IRAs with no tax consequence and then escape having to take mandatory minimum distributions when they turn 73.

What is a Roth IRA?

Is It Better to Invest in a Roth IRA or a 401(k)?

There are many variables to consider when choosing a Roth IRA or a 401(k) retirement account. Each type of account provides an opportunity for savings to grow tax-free. Roth IRAs do not provide tax advantages when you make a deposit, but you can withdraw tax-free during retirement. The reverse is true for 401(k)s. These types of accounts involve contributing a portion of your paycheck to a 401(k) prior to income tax deductions. In terms of contribution limits, Roth IRAs are typically lower than 401(k)s.

Additionally, 401(k)s allow employers to make matching contributions. On the flip side, 401k(s) often have higher fees, minimum distributions, and fewer investment options.

How Much Can I Put in My Roth IRA Monthly?

In 2023, the maximum annual contribution amount for a Roth IRA is $6,500, or $541.67 monthly for those under age 50. This amount increases to $7,500 annually, or roughly $625 monthly, for individuals age 50 or older. Note there is no monthly limit, only the annual limit.

The limits increase for 2024 to $7,000 annually or $583.33 monthly. For those 50 and older, the limit is $8,000 annually or $666.67 monthly.

What Are the Advantages of a Roth IRA?

While Roth IRAs do not include an employer match, they do allow for a greater diversity of investment options.6 For individuals who anticipate that they will be in a higher tax bracket when they’re older, Roth IRAs also can be a beneficial option. And you can withdraw your contributions (but not earnings) at any time, tax- and penalty-free. Ultimately, you can manage how you want to invest your Roth IRA by setting up an account with a brokerage, bank, or qualified financial institution.

What Are the Disadvantages of a Roth IRA?

Among the disadvantages of Roth IRAs is the fact that, unlike 401(k)s, they do not include an up-front tax break. Secondly, annual contribution limits are about a third of 401(k)s. And for some high-income individuals, contributions are either reduced or not allowed.

The Bottom Line

A Roth IRA is an individual retirement account (IRA) that allows you to withdraw money (without paying a penalty) on a tax-free basis after age 59½, and after you have owned the account for its five-year holding period. If you buy a home, pay for college, or need your Roth funds for the birth or adoption of a child, you can also withdraw without paying a penalty.

Roth accounts are funded with after-tax money, so while you don't get the up-front tax break of a traditional IRA, you can withdraw your contributions without paying federal or state income tax on the amount after meeting the criteria for withdrawals.

For individuals who anticipate that they will be in a higher tax bracket when they are older or have retired, Roth IRAs can provide a beneficial option, as the money is not taxable, unlike a 401(k) or traditional IRA withdrawals.