By Anne Tergesen

March 11, 2024

The 401(k) is doing double duty as both a retirement account and a source of emergency funds for more Americans.

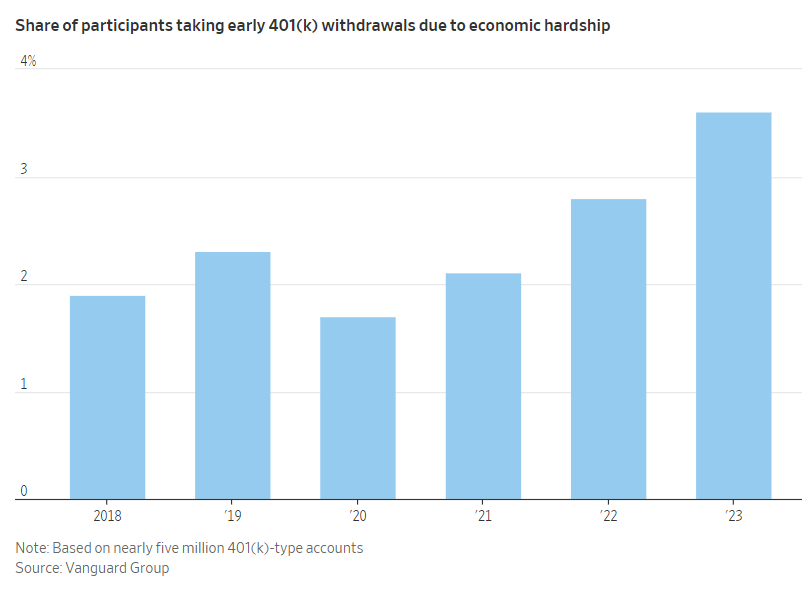

A record share of 401(k) account holders took early withdrawals from their accounts last year for financial emergencies, according to internal data from Vanguard Group. Overall, 3.6% of its plan participants did so last year, up from 2.8% in 2022 and a prepandemic average of about 2%.

iStock image

Retirement plans such as the 401(k) are designed to keep Americans’ nest eggs out of reach until later in life. And values in these accounts have risen substantially, in part because of a strong stock market and programs that automatically funnel money from people’s paychecks into their 401(k) accounts.

These surging balances, however, have helped make more people comfortable dipping into their accounts when needed.

Americans are dealing with conflicting financial forces. While hiring has been strong and workers’ earnings keep rising, the cost of groceries, child care and car insurance keeps climbing. More people are carrying heftier balances on their credit cards.

Pulling money out

Emergency distributions hit back-to-back record highs in 2022 and 2023, according to Vanguard, which administers 401(k)-type accounts for nearly five million people and published the data ahead of an annual report scheduled for June.

The Internal Revenue Service allows withdrawals for hardship-related reasons, including preventing evictions and paying medical and tuition bills. People who take them from traditional accounts must pay income tax, plus often a 10% penalty if they are younger than 59½ years old.

Nearly 40% of those who took a hardship distribution last year did so to avoid foreclosure, compared with 36% in 2022. In 2023, more than 75% of hardship distributions totaled $5,000 or less, according to Vanguard.

Recent changes in federal law have loosened the rules governing when people can tap their retirement accounts for hardship-related reasons. For example, under a 2018 law, Congress did away with a requirement to take a 401(k) loan before a hardship distribution.

About 13% of participants had a 401(k) loan outstanding at the end of 2023, up from 12% the year before. As interest rates have risen, more investors may be turning to 401(k) loans to avoid higher-cost debt, said Dave Stinnett, head of strategic retirement consulting at Vanguard.

The law allows participants to borrow generally up to half of their balance, or $50,000, whichever is less. Stinnett said many workers like the idea of borrowing from themselves, since that means they repay their own account over time, along with interest set by the retirement plan.

Those who default on loans from traditional pretax 401(k) accounts must pay income taxes and often a 10% penalty on the unpaid balance.

Putting money in

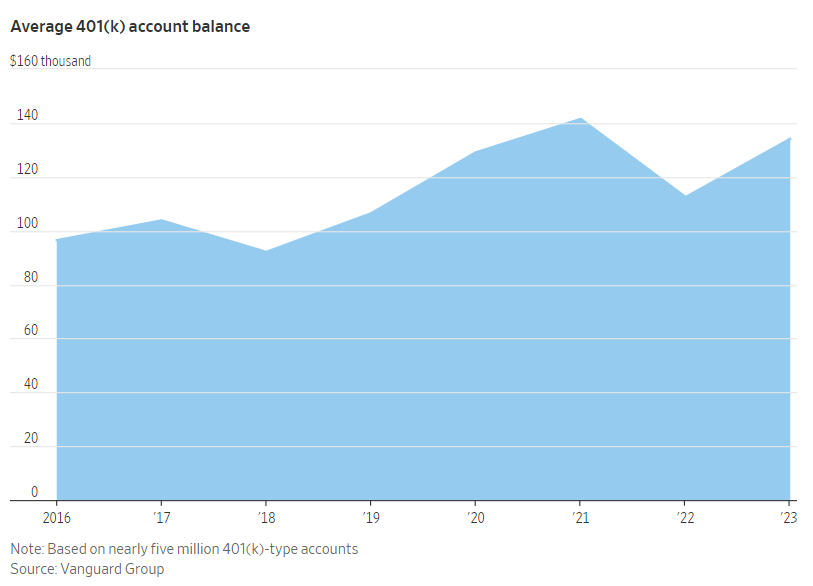

Average account balances rose 19% in 2023, according to Vanguard, a welcome change from 2022, when falling stock and bond markets wiped 20% from the average 401(k) balance.

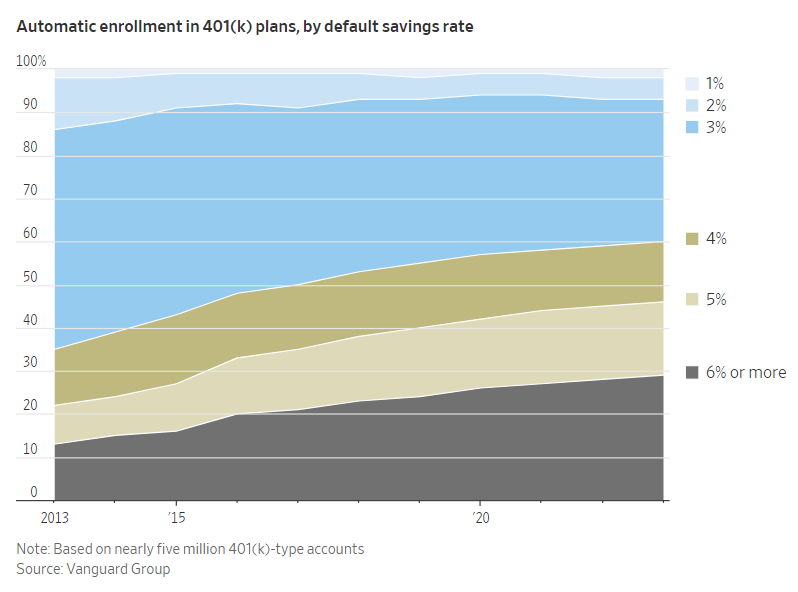

The growing popularity of automatic enrollment has moved more workers into 401(k) accounts. Among the more than 1,500 employer plans that use Vanguard’s 401(k) administration services, 59% automatically enrolled new hires in 2023, up from 34% in 2013.

Nearly three in 10 plans with automatic enrollment started workers out at a savings rate of 6% of pay or higher. In 2013, just 13% of plans with auto-enrollment used a starting savings rate of 6% or more.

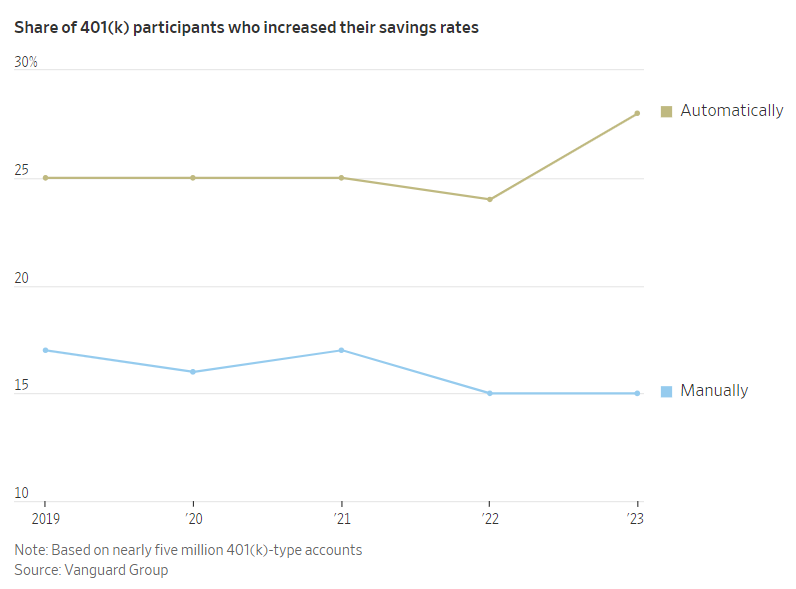

More people are increasing their 401(k) contribution rates annually, in part because of programs that put retirement savings on autopilot, said Stinnett.

A majority of plans that automatically enroll new hires also automatically increase employees’ savings rates, typically by 1 or 2 percentage points a year until reaching a cap that is often 10% or more of pay, according to Vanguard. Employees are free to opt out.

A record 43% of 401(k) participants saved more in 2023 than they did in 2022.

The spread of such auto-escalation programs has helped boost the money going into these accounts. Workers contributed an average of 11.3% of pay, including the employer match, in 2022, the latest year for which data are available from Vanguard. That is up from 10.4% in 2016, and close to the 12% to 15% annual savings rates that many advisers recommend.

Write to Anne Tergesen at anne.tergesen@wsj.com

Dow Jones & Company, Inc.