Matt King

July 17, 2024

Swings in central bank reserves provide a powerful indicator of liquidity in markets.

iStock-1432418176

Markets this year have followed the same law that held during much of 2023: whatever the news, equities and credit always rally. But there are growing reasons to doubt whether the pattern will hold.

The problem is not with the economy. Recession fears are all but forgotten. Lower inflation means real wages are growing again. Corporate profits are strong, with little sign of pressure on record margins. Despite 20-year highs in interest rates, unemployment has ticked up only slightly from record lows. Credit concerns linger, but even the prospect of losses on some tranches of commercial property debt previously rated AAA shows little sign of proving systemic. Besides, were the outlook to deteriorate, central banks would simply move to additional rate easing.

Nor, for now, does it feel like political concerns have sufficient power to end the rally. Despite growing evidence of the electoral appeal of extremist parties and policies, markets struggle to price budgetary irresponsibility until confronted by its reality. A brief attempt to re-establish a political risk premium in France has fizzled out. And increasing expectations of Trump 2.0 for now seem more likely to be accompanied by rallying equities and bank outperformance on deregulation prospects than by bond yield tantrums.

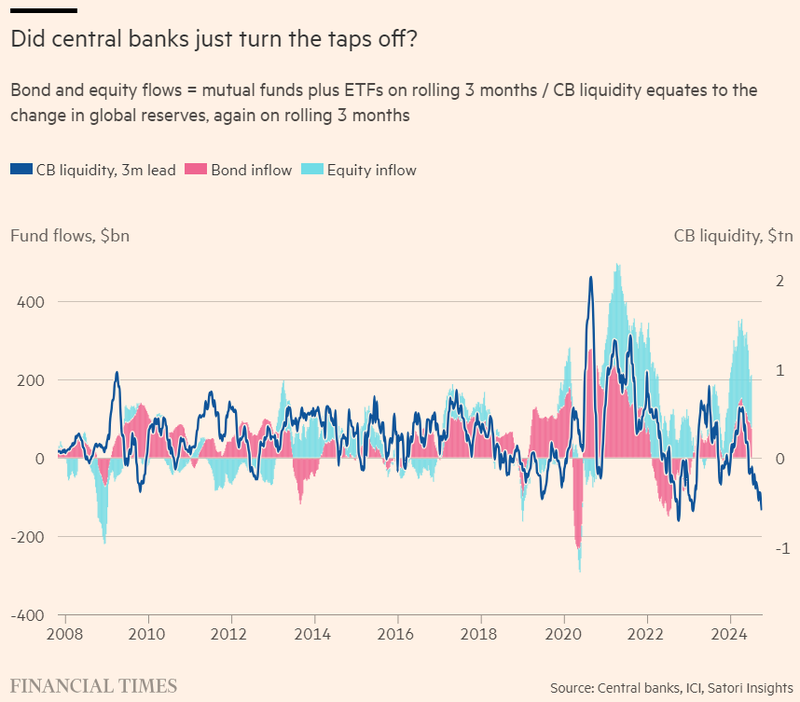

The reasons for doubt come instead from the flows that have fuelled the rally, and from the money creation dynamics which underlie them. At $600bn, year-to-date inflows to mutual funds and ETFs exceed those for any year bar 2021. As many a portfolio manager will acknowledge when not in marketing mode, it is ongoing inflows — not the cheapness of their asset classes — which keeps them buying.

Historically, the inflows look like an anomaly. Current levels of interest rates would normally have spurred a rotation away from riskier assets and into money markets and treasury bills. But no such rotation has occurred. This is partly because even as central banks have been tightening with one hand, they have been easing with the other.

Ongoing quantitative tightening — the reversal of massive central bank quantitative easing programmes to support economies since the financial crisis — ought normally to have reduced the level of reserves that commercial banks hold at central banks. But other factors also drive reserves.

When governments reduce their deposits at central banks and spend it in the real economy, it boosts the deposits and reserves of commercial banks. The same happens when money market funds move money out of the Fed’s Reverse Repo Programme — a facility to store cash at the central bank — and put it to work in markets, say by buying treasury bills. In all such cases, reserves are a convenient measure of the “portfolio balance” effect: how much money is in private hands relative to how many assets are available to absorb it.

In the six months following markets’ most recent trough last October, global reserves rose by $600bn, ongoing QT notwithstanding. As such, the risk rally was no coincidence: it was almost as though central banks had been doing QE.

More than enthusiasm about fundamentals or valuations or prospects for rate easing, this additional money was the ultimate source of the mutual fund inflows. As under QE itself, rising liquidity pushed investors into taking risk in search of returns, fuelling momentum and encouraging widespread disregard for expensive valuations.

Central banks’ devotion to theory and focus on the impact of reserve levels on rates has largely blinded them to the impact such liquidity swings have on markets. When reserves have been drained, first in 2022, then in April this year and again briefly in late June, both fund flows and markets have fallen. A narrowing group of US equities may have outperformed but that reflects a greater focus on a smaller number of stocks as liquidity dwindles. Performance and flows in credit, emerging markets and bitcoin also have all softened since April — in line with reserves.

Thinking in terms of these money flows — and not just rate changes — casts this year’s market performance in a very different light. Mutual fund flows in the past few weeks have remained quite strong notwithstanding the lack of support from reserves. That decoupling may have further to run. But with the liquidity torrent from central banks unlikely to be re-established in coming months, any further rally from here looks at risk of drying up. And rate easing, when it comes, is unlikely to be a substitute.

Copyright The Financial Times Limited 2024

© 2024 The Financial Times Ltd. All rights reserved. Please do not copy and paste FT articles and redistribute by email or post to the web.

This article was legally licensed by AdvisorStream