By Sam Goldfarb

Jan. 2, 2024

U.S. stocks delivered outsize returns in 2023. This year, many investors are dreaming of something more normal.

Their wish list includes an economic backdrop of moderate inflation and middle-of-the road interest-rate policies—seemingly modest aspirations that would still mark a change from both the recent rate surge and the stimulus-fueled meme-stock craziness that preceded it.

iStock image

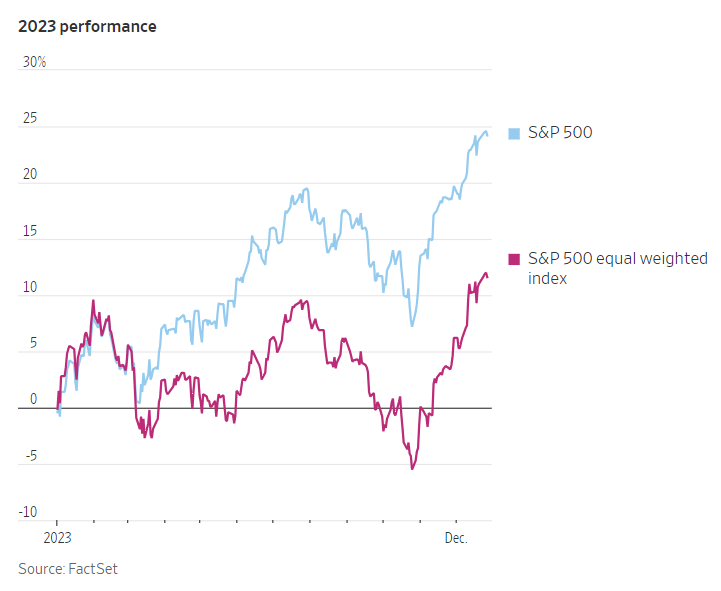

Few think the S&P 500 can match its 24% gain from 2023, which essentially erased its 2022 losses. Many, though, believe that a return to economic normalcy could translate into a reasonable and sustainable rise in stocks, powered by improving corporate earnings.

They also have high hopes for conventional portfolios made up of 60% stocks and 40% bonds, a time-honored Wall Street strategy for mitigating risk that has recently been battered by rising rates.

They could be disappointed. Twelve-month inflation remains above the Federal Reserve’s 2% target, and a round of data showing an unexpectedly large jump in prices could lead investors to question their assumptions about how quickly the Fed will cut interest rates. That would likely cause bonds and stocks to fall in tandem, as has happened often in the past two years.

Yet there are causes for optimism. The Fed’s preferred measure of inflation has cooled substantially and is already right around 2% on a three-month or six-month annualized basis. The Fed itself has signaled that it is likely to start trimming rates soon. At the same time, more than a year of rate increases has had the benefit of driving up U.S. Treasury yields, which are largely determined by expectations for future short-term rates.

That means bonds promise solid returns if interest-rate expectations don’t change. They also have more room to rally if economic conditions deteriorate and the Fed cuts rates more aggressively.

Rising rates have been painful recently. But the previous period of near-zero rates was also “not a stable equilibrium,” given how those rates punished certain savers and rewarded businesses that would have otherwise been uncompetitive, said Matt Toms, global chief investment officer at Voya Investment Management.

“We’ve returned to a point that looks a heck of a lot more stable,” he added.

Markets have taken a long road to get here.

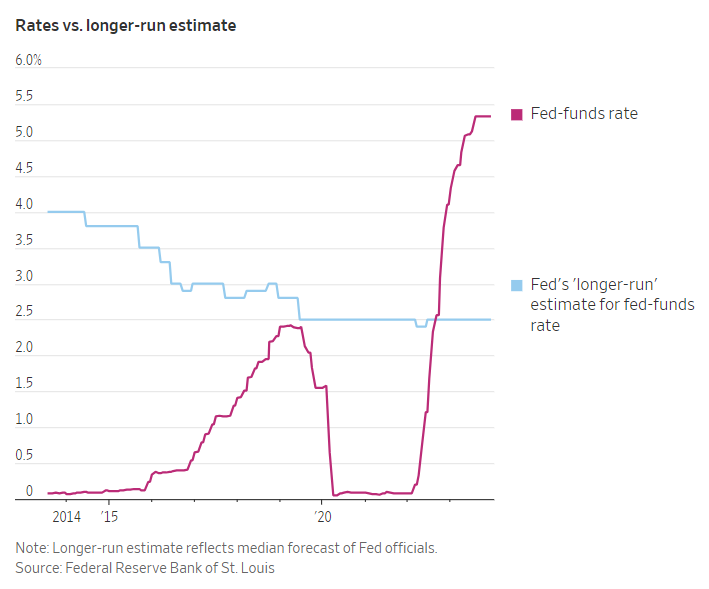

For years after the 2008-2009 financial crisis, the chief concern of Fed officials was that consumer prices were rising too slowly, creating the risk of deflation. As a result, they kept interest rates near zero and bought trillions of dollars in bonds, trying to stimulate the economy. Stocks and other risky assets thrived, but bonds offered paltry returns and there were nagging concerns that the Fed was creating a bubble.

Conditions became more extreme in the early stages of the Covid-19 pandemic, with even longer-term bond yields falling below 1% and investors piling into everything from cryptocurrencies to meme stocks such as GameStop.

Between the financial crisis and 2022, the highest the Fed raised its benchmark federal-funds rate was near 2.5% at the end of 2018. But, even then, it quickly pivoted to cutting rates by mid-2019.

Now, the Fed’s fight against inflation has brought the fed-funds rate to around 5.3%. The rate is widely expected to come down from here, but neither the Fed nor interest-rate markets are predicting that it will fall back below 2.5%.

Rising interest rates are a double-edged sword for bond investors. In the short-term, they drive down the price of existing bonds issued when rates were lower. That same process, however, pushes up yields, or the annualized expected return on bonds (assuming they get paid back in full at maturity).

Once rates stabilize, as they have recently, investors can start to appreciate those higher yields. Still, they could be frustrated if yields move sharply again in either direction.

Already, bets that rates will fall have dragged the yield on the 10-year Treasury note down to around 3.9% from roughly 5% in late October.

Some analysts warn that investors might have gotten ahead of themselves and that bond prices could fall if rate cuts take longer than expected. Bond prices could also drop if the growing supply of Treasurys needed to fund the federal budget deficit starts to overwhelm demand.

Conversely, bonds could provide a refuge in a recession, with their prices rising as rates fall. But that could also drag yields back to prepandemic levels, giving investors only a short-lived benefit.

“We’ve seen a massive move in fixed income already,” said Lori Heinel, global chief investment officer at State Street Global Advisors. With volatility still high, it is unlikely that the next move in yields will be a one-directional trade, she added.

Higher yields are also no guarantee that stocks will behave calmly.

Some worry that stock prices are already too high relative to the earnings that analysts expect over the next year, especially when compared with the yield investors can get from bonds. In 2023, just a handful of large technology companies were responsible for a bulk of the S&P 500’s gains, similar to when yields were lower.

Still, there was a shift toward the end of 2023, with investors favoring shares from a much wider range of companies after an encouraging inflation report in November. Many expect this trend to continue in 2024 as investors look for bargains outside of the tech sector.

Wylie Tollette, chief investment officer at Franklin Templeton Investment Solutions, said his team believes that “higher yields lift all boats,” providing investors with a safe way to earn returns while tempering excesses in stocks.

At the same time, he expressed optimism that stocks can weather the competition from bonds. He pointed to both their record and the potential for new artificial-intelligence technologies to boost corporate profits.

“Corporates have shown an amazing resiliency at generating continued earnings growth even in the face of a slowing economy,” he said.

Write to Sam Goldfarb at sam.goldfarb@wsj.com

Dow Jones & Company, Inc.