By Francesco Guerrera

July 17, 2024

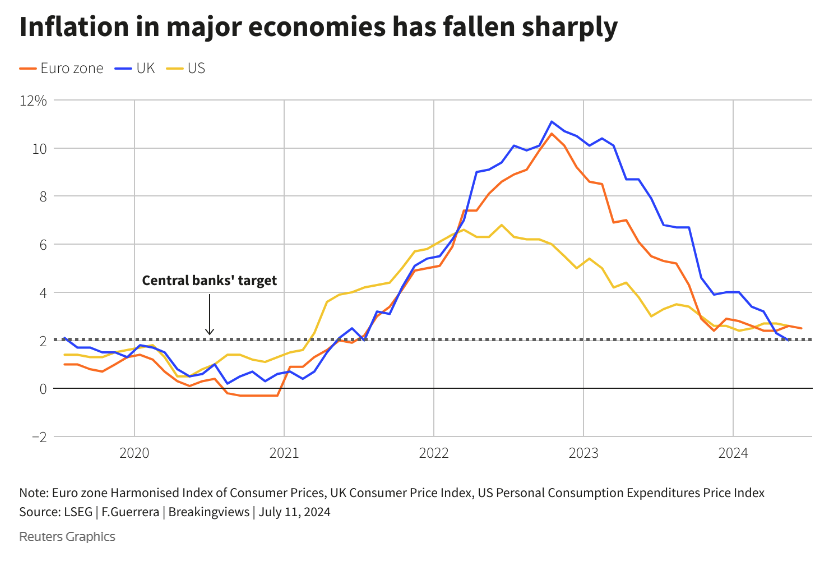

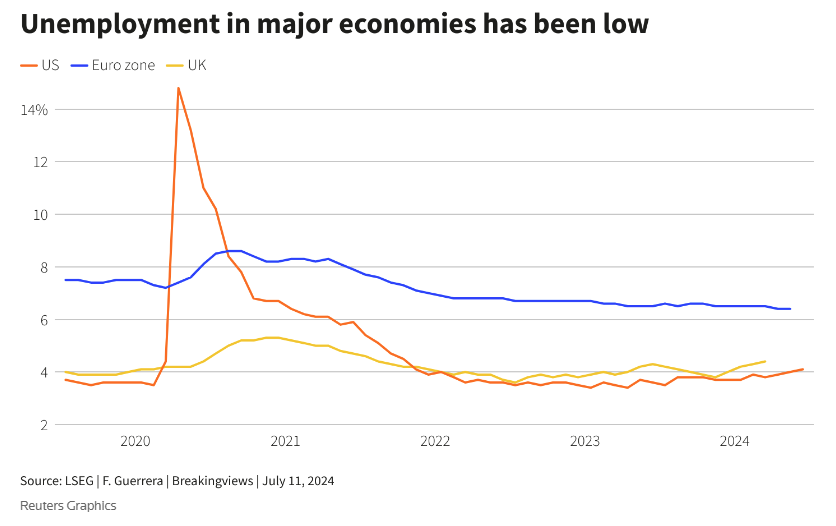

LONDON, (Reuters Breakingviews) - Central bankers are close to declaring mission accomplished. After inflation soared beyond 9% following the pandemic and Russia’s invasion of Ukraine, it’s tumbling back toward the 2% level targeted by the U.S. Federal Reserve and its peers in Britain and Europe. They were initially wrong-footed, but eventually responded with sharp and swift increases to benchmark interest rates. And contrary to most predictions by economists and market strategists, this aggressive policy did not trigger major recessions in the world’s largest economies.

iStock image

For monetary authorities, this is as good it gets. But before Fed Chair Jerome Powell, European Central Bank boss Christine Lagarde and Bank of England Governor Andrew Bailey close the book on this treacherous period, they would be well-served to acknowledge the amount of luck that was involved and learn what they could do better when the next crisis rolls around. As Alan Greenspan, one of Powell’s predecessors, once said, “Excessive optimism sows the seeds of its own reversal.”

In that spirit, here are five useful takeaways.

BE HUMBLE.

Modesty is a relative concept here. By the standards of corporate chieftains, central bankers are typically even-keeled, soft-spoken and deliberate. During this economic cycle, however, they often came off too confident in their convictions.

That’s particularly true for Powell and his penchant for describing inflation as “transitory.” He introduced the idea in March 2021, when yearly price growth was still below 2%, but then stuck with it for months and only “retired it” eight months later. By then, the Fed’s preferred measure of inflation was more than twice its target rate. A lingering anchoring effect probably played a part in the Fed’s decision to wait yet another four months before making it pricier to borrow.

A century ago, renowned economist John Maynard Keynes urged investors to change their minds when facts change. The tenet applies equally, if not more so, to interest-rate guardians.

TALK LESS.

In 1987, Greenspan famously told a congressional committee: “If I seem unduly clear to you, you must have misunderstood what I said.” It’s hardly the case anymore. Pressure from investors, politicians and media for central bankers to be less Delphic has opened the verbal floodgates.

Since January, ECB board members alone have delivered 55 speeches. In the United States, the seven members of the Fed’s main board and the heads of its 12 regional banks can often be found behind a microphone somewhere, while in Britain, five internal and four external members of the BoE’s Monetary Policy Committee are talkative, too.

Throw in parliamentary appearances and the press conferences that follow interest rate decisions, and it’s a veritable Tower of Babel, or babble, to decipher. Investors seem baffled. When academics Anna Cieslak, Michael McMahon and Hao Pang asked ChatGPT models to analyze some 7,700 articles about the Fed published in the Wall Street Journal between 2020 and 2023, they found that more than a third of them conveyed a degree of confusion. Even the professionals are crying uncle. Although they praise Fed communications overall, nearly 60% of experts surveyed by Brookings Institution said regional presidents should say less.

GET UNSTUCK.

Every central banker’s worst nightmare is “1970s-style inflation.” During that stretch, which extended into the early 1980s, U.S. prices nearly doubled, prompting the Fed, then-led by Paul Volcker, to jack up interest rates to about 20%. In Germany, prices rose 46% between 1974 and 1982, spurring the Bundesbank to attempt similarly painful heroics.

Powell & Co. feared that, as inflation accelerated, companies and workers would recalibrate their own expectations for prices and wages and feed an uncontrollable upward spiral. In applying the Volcker playbook, however, central banks failed to fully appreciate that price growth was largely due to unusual shocks to supply chains and consumer behavior. In that sense, it was less like the disco era and more like the one after World War Two, a cyclical, albeit prolonged, phenomenon caused by the transition to peacetime economies.

By mimicking Volcker, central banks risk endangering economic growth. The euro zone and Britain already have experienced recessions, albeit shallow ones, while U.S. GDP expanded by just 1.4% year-on-year in the first quarter this year, down from 3.4% during the last three months of 2023.

CHANGE MODELS.

One shortcoming laid bare has been within PhD-laden central bank research departments: their go-to methods of data-crunching aren’t necessarily well-suited for every economic situation.

Take the Phillips curve, for example. Developed by New Zealand economist William Phillips, it correlates lower unemployment with higher wages, postulating that there are short-term trade-offs between inflation and joblessness. Its corollary is that to tame prices, central banks have to hurt labor markets.

Powell said as much in a high-profile speech on Aug. 26, 2022, which led to a rout in stock markets. Since the Fed began raising rates, however, U.S. unemployment has hovered around a historically low 3% to 4% rate. Economists disagree on the reasons, but it’s clear the Phillips curve was unreliable this time around.

One possible solution comes from another former Fed chair, Ben Bernanke. When reviewing the BoE’s forecasting methods after a series of mistakes, he suggested embracing scenario analysis, or comparing a variety of likely economic outcomes under alternative assumptions. Bernanke also advocated a “risk-management” approach to policymaking and taking out “insurance” against potential pitfalls. It’s what Greenspan did in July 1995, when the Fed unexpectedly cut rates because it feared the economy was weakening.

LOOK AHEAD.

Being at the helm amid choppy waters is a difficult and thankless task. If nothing else, however, this two-year span has shown that economics is not, as Thomas Carlyle said in the 19th century, “a dismal science,” but a cheerless art.

After obsessing for years over how to push inflation higher and, in the Fed’s case, changing its official target to reflect as much, central bankers were faced with diametrically opposed conditions. The reliance on historical upheavals and models did not serve them well, even though they may yet engineer the elusive “soft landing.” It’s important to be thinking about the next crisis as much as the previous or existing ones.

For all their stumbles, Powell, Lagarde and Bailey deserve a victory lap. As they circle the track, they would do well to embrace the lessons from recent experiences and also recall what Powell told his assembled peers almost a year ago: “We are navigating by the stars under cloudy skies.”

CONTEXT NEWS: U.S. Federal Reserve Chair Jerome Powell told Congress on July 9 that “more good data” would strengthen the case for the central bank to begin cutting benchmark interest rates.

On July 11, the U.S. Bureau of Labor Statistics reported that the consumer price index had fallen by 0.1% in June, the first drop since May 2020. In the 12 months through June, the CPI increased 3%, higher than the 2% level targeted by the Fed.