Amy Fontinelle

May 22, 2024

Setting short-term financial goals, as well as mid-term and long-term, is an important step toward becoming financially secure. If you aren’t working toward anything specific, you’re likely to spend more than you should. You’ll then come up short when you need money for unexpected bills, not to mention when you want to retire. You might get stuck in a vicious cycle of credit card debt and feel like you never have enough cash to get properly insured, leaving you more vulnerable than you need to be to handle some of life’s major risks.

Even the most prudent person can't prepare against every crisis, as the world learned in the pandemic and many families learn every month. What thinking ahead does is give you a chance to work through things that could happen and do your best to prepare for them. This should be an ongoing process so you can shape your life and goals to fit the changes that will inevitably come.

KEY TAKEAWAYS

- Proper financial and retirement planning starts with goal setting, including short-, intermediate-, and long-term goals.

- Key short-term goals include setting a budget, reducing debt, and starting an emergency fund.

- Medium-term goals should include key insurance policies, while long-term goals need to be focused on retirement.

Annual financial planning gives you an opportunity to formally review your goals, update them, and review your progress since last year. If you’ve never set goals before, take the opportunity to formulate them so you can get—or stay—on firm financial footing. Here are goals, from near-term to distant, that financial experts recommend setting to help you learn to live comfortably within your means, reduce your money troubles, and save for retirement.

Short-Term Financial Goals

Setting short-term financial goals gives you the foundation and the confidence boost that you'll need to achieve the bigger goals that take more time. These first steps can relatively easy to achieve in as little as a year: Create a budget and stick with it. Build an emergency fund. Pay down the credit card debt that's holding you back.

Establish a Budget

“You can’t know where you are going until you really know where you are right now. That means setting up a budget,” says Lauren Zangardi Haynes, a fiduciary and fee-only financial planner with Spark Financial Advisors in Richmond and Williamsburg, Virginia. “You might be shocked at how much money is slipping through the cracks each month.”

An easy way to track your spending is to use a free budgeting program like Mint. It will combine the information from all your accounts into one place so you can label each expense by category. You can also create a budget the old-fashioned way by going through your bank statements and bills from the past few months and categorizing each expense with a spreadsheet or on paper.

When you see how you are spending your money and you're guided by that information, you can make better decisions about where you want your money to go in the future. Is the enjoyment and convenience of eating out worth the extra money each month to you? If so, great—as long as you can afford it. If not, you’ve just discovered an easy way to save money every month. You can look for ways to spend less when you dine out, replace some restaurant/takeout meals with homemade ones, or have a combination of the two.

Create an Emergency Fund

An emergency fund is money you set aside specifically to pay for unexpected expenses. To get started, $500 to $1,000 is a good goal. When you meet that goal, you’ll want to expand it so that your emergency fund can cover greater financial difficulties, such as unemployment. If you didn’t have an emergency fund prior to the COVID-19 pandemic, you likely wished you did. And if you did have one, you may have tapped into it and need to replenish it.

Ilene Davis, a certified financial planner (CFP) with Financial Independence Services in Cocoa, Florida, recommends saving at least three months' worth of expenses to cover your financial obligations and basic needs, but preferably six months' worth—especially if you are married and work for the same company your spouse does or if you work in an area with limited job prospects. She says finding at least one thing in your budget to cut back on can help fund your emergency savings.

Another way to build emergency savings is through decluttering and organizing, says Kevin Gallegos, vice president of sales and Phoenix operations with Freedom Financial Network, an online financial services company for consumer debt settlement, mortgage shopping, and personal loans. You can make extra money by selling unneeded items on eBay or Craigslist or holding a yard sale. Consider turning a hobby into part-time work from which you can devote the income to savings.

Zangardi Haynes recommends opening a savings account and setting up an automatic transfer for the amount you’ve determined you can save each month (using your budget) until you hit your emergency fund goal. “If you get a bonus, tax refund, or even an ‘extra’ monthly paycheck—which happens two months out of the year if you are paid biweekly—save that money as soon as it comes into your checking account. If you wait until the end of the month to transfer that money, the odds are high that it will get spent instead of saved,” she says.

Important: Though you probably have other savings goals too, such as saving for retirement, creating an emergency fund should be a top priority. It’s the savings account that creates the financial stability you need to achieve your other goals.

Pay Off Credit Cards

Experts disagree on whether to pay off credit card debt or create an emergency fund first. Some say that you should create an emergency fund even if you still have credit card debt because, without an emergency fund, any unexpected expense will send you further into credit card debt. Others say you should pay off credit card debt first because the interest is so costly that it makes achieving any other financial goal much more difficult. Pick the philosophy that makes the most sense to you, or do a little of both at the same time.

As a strategy for paying off credit card debt, Davis recommends listing all your debts by interest rate from lowest to highest, then paying only the minimum on all but your highest-rate debt. Use any additional funds you have to make extra payments on your highest-rate card.

The method Davis describes is called the debt avalanche. Another method to consider is called the debt snowball. With the snowball method, you pay off your debts in order of smallest to largest, regardless of the interest rate. The idea is that the sense of accomplishment you get from paying off the smallest debt will give you the momentum to tackle the next-smallest debt, and so on until you’re debt-free.

Gallegos says debt negotiation or settlement is an option for those with $10,000 or more in unsecured debt (such as credit card debt) who can’t afford the required minimum payments. Companies that offer these services are regulated by the Federal Trade Commission and work on the consumer’s behalf to cut debt by as much as 50% in exchange for a fee, typically a percentage of the total debt or a percentage of the amount of debt reduction, which the consumer should only pay after a successful negotiation. Consumers can get out of debt in two to four years this way, Gallegos says. The drawbacks are that debt settlement can hurt your credit score, and creditors can take legal action against consumers for unpaid accounts.

Warning: Bankruptcy should be a last resort because it destroys your credit rating for up to 10 years.

Midterm Financial Goals

When you’ve created a budget, established an emergency fund, and paid off your credit card debt—or at least made a good dent in those three short-term goals—it’s time to start working toward midterm financial goals. These goals will create a bridge between your short- and long-term financial goals.

Get Life Insurance and Disability Income Insurance

Do you have a spouse or children who depend on your income? If so, you need life insurance to provide for them in case you pass away prematurely. Term life insurance is the least complicated and least expensive type of life insurance and will meet most people’s insurance needs. An insurance broker can help you find the best price on a policy. Most term life insurance requires medical underwriting, and unless you are seriously ill, you can probably find at least one company that will offer you a policy.

Gallegos also says that you should have disability insurance in place to protect your income while you are working. “Most employers provide this coverage,” he says. “If they don’t, individuals can obtain it themselves until retirement age.”

Disability insurance will replace a portion of your income if you become seriously ill or injured to the point that you can’t work. It can provide a larger benefit than Social Security disability income, allowing you (and your family, if you have one) to live more comfortably than you otherwise will if you lose your ability to earn an income. There will be a waiting period between when you become unable to work and when your insurance benefits will start to pay out, which is another reason why having an emergency fund is so important.

Pay Off Student Loans

Student loans are a major drag on many people’s monthly budgets. Lowering or getting rid of those payments can free up cash that will make it easier to save for retirement and meet your other goals. One strategy that can help you pay off your student loans is refinancing into a new loan with a lower interest rate. But beware: If you refinance federal student loans with a private lender, you may lose some of the benefits associated with federal student loans, such as income-based repayment, deferment, and forbearance, which can help if you fall on hard times.

Tip: If you have multiple student loans and won’t stand to benefit from consolidating or refinancing them, the debt avalanche or debt snowball methods mentioned above can help you pay them off faster.

Consider Your Dreams

Midterm goals can also include goals like buying a first home or, later on, a vacation home. Maybe you already have a home and want to upgrade it with a major renovation—or start saving for a larger place. Saving for college expenses or the costs that come with starting a family are other examples of midterm goals.

When you've set one or more of these goals, start figuring out how much you need to save to make a dent in reaching them. Visualizing the type of future you want is the first step toward achieving it.

Long-Term Financial Goals

The biggest long-term financial goal for most people is saving enough money to retire. The common rule of thumb is that you should save 10% to 15% of every paycheck in a tax-advantaged retirement account like a 401(k) or 403(b), if you have access to one, or a traditional IRA or Roth IRA. But to make sure you’re really saving enough, you need to figure out how much you'll actually need to retire.

Estimate Your Retirement Needs

Oscar Vives Ortiz, a CPA financial planner with PNC Wealth Management in the Tampa Bay/St. Petersburg, Florida, area, says you can do a quick back-of-the-envelope calculation to estimate your retirement readiness:

- Estimate your desired annual living expenses during retirement. The budget you created when you started on your short-term financial goals will give you an idea of how much you need. You may need to plan for higher healthcare costs in retirement.

- Subtract the income you will receive. Include Social Security, retirement plans, and pensions. This will leave you with the amount that needs to be funded by your investment portfolio.

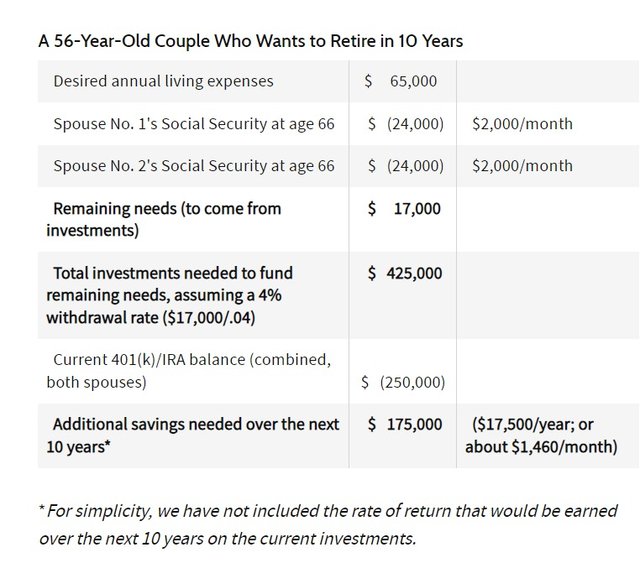

- Estimate how much in retirement assets you need for your desired retirement date. Base this on what you currently have and are saving on an annual basis. An online retirement calculator can do the math for you. If 4% or less of this balance at the time of retirement covers the remaining amount of expenses that your combined Social Security and pensions do not cover, you are on track to retire.

4.5%

The sustainable withdrawal rate for retirement in the U.S., based on a 15% savings rate and 45% income replacement rate.

If, for example, you started with a portfolio of $1 million and withdrew $40,000 in year one (4% of $1 million), then increased the withdrawal by the rate of inflation each subsequent year ($40,000 plus 2% in year two, or $40,800; $40,800 plus 2% in year three, or $41,616, and so on), you would have made it through any 30-year retirement without running out of money. “This is why you often see 4% as a rule of thumb when discussing retirement,” Vives Ortiz says.

“In most scenarios, you actually end up with more money at the end of 30 years using 4%, but in the worst of the worst, you would have run out of money in year 30,” he adds. “The only word of caution here is that just because 4% has survived every scenario in history does not guarantee it will continue to do so going forward.”

Ortiz provided the following example of how to estimate whether you’re on track to retire:

Increase Retirement Savings

For most people who have an employer-sponsored retirement plan, the employer will match a percentage of what you are paid, says CFP Vincent Oldre, founder of CFG Retirement in Minneapolis. They might match 3% or even 7% of your paycheck. You can get a 100% return on your investment if you contribute enough to get your full employer match, and this is the most important step to take to fund your retirement.

“What kills me is that people do not put money into their retirement plan because either they ‘can’t afford to’ or they are ‘afraid of the stock market.’ They miss out on what I call a ‘no-brainer’ return,” Oldre says.

Michael Cirelli, a financial advisor with SAI Financial in Warrenville, Illinois, recommends making IRA contributions at the beginning of the year as opposed to the end, when most people tend to do it, to give the money more time to grow and give yourself a larger amount to retire with.

What Are Examples of Financial Goals?

There are all kinds of financial goals that a person can set for themselves. Some of the most common include paying off debt, saving for retirement, establishing an emergency fund, saving money for a down payment on a home, saving money for a child's college education, feeling financially secure and comfortable, and being able to financially help a friend or family member.

How Do You Start Setting Your Financial Goals?

One way to set your financial goals is to use so-called SMART goals. In the acronym, S stands for specific, M is for measurable, A is for achievable, R is for relevant, and T is for time-based. Write out specific goals you have, prioritize them, and then go through all the SMART factors. For retirement, have a specific age you want to retire at and a measurable amount of funds that you want to have available at that age. Make sure the goal is realistic and achievable. Make it relevant and be sure you have a set plan to achieve that goal in a specific timeframe.

Should You Make a Budget?

A budget is a financial plan geared toward a specific, often short-term amount of time. Creating a budget can be a great way to keep track of your finances and make changes to the way you spend money. It can also help achieve specific financial goals, such as cutting debt or saving money.

The Bottom Line

You probably won’t make perfect, linear progress toward achieving any of your goals, but the important thing is to be consistent. If you are hit with an unexpected car repair or medical bill one month and can’t contribute to your emergency fund but have to take money out of it instead, don’t beat yourself up; That’s what the fund is there for. Just get back on track as soon as you can.

The same is true if you lose your job or get sick. You’ll have to create a new plan to get through that difficult period, and you may not be able to pay down debt or save for retirement during that time, but you can resume your original plan—or perhaps a revised version—when you come out on the other side.

That’s the beauty of annual financial planning: You can review and update your goals and monitor your progress in reaching them throughout life’s ups and downs. In the process, you will find that both the small things you do on a daily and monthly basis and the bigger things you do every year and over the decades will help you achieve your financial goals.