Robert Armstrong

June 6, 2024

Ignore the noise and focus on employment.

iStock-1184451055

Slowdown, or just normalisation?

Earlier this week, I took a look at the possibility that the US consumer — hero of the “no-landing” economic scenario that sets hearts aflutter across Wall Street and the world — might be slowing down a bit. The key evidence: a weak personal consumption expenditures report for April. Over the last day or two, though, the economic slowdown narrative has kept popping up in the media and in emails from assorted banks, brokers, and research shops. Here, for example, is Paul Krugman in the New York Times:

[T]he big narrative from last year — “immaculate disinflation,” inflation gradually ramping down to an acceptable rate even though we haven’t had the recession some economists insisted was necessary — is back on track. The big question now is whether, having discovered that we didn’t need a recession, we’ll get one anyway . . .

I think the Fed should start cutting rates, and soon.

Yesterday, this narrative got another piece of supporting evidence, in the form of the April Job Openings and Labor Turnover Survey (Jolts).

The survey showed job openings falling briskly from March (about 300,000 openings disappeared, a decline of 4 per cent). This brings the ratio of job openings to unemployed people to 1.24, which looks a lot like pre-pandemic normalcy:

There are two ways one might respond to this. One way is: yay, the labour market is back to normal, wage and inflation pressure is going to keep falling, and now Federal Reserve policy can become accommodative. Here for example is Ron Temple of Lazard: “The evidence is accumulating that the Fed should begin easing . . . Today’s labour report taken together with April’s improved inflation data should cause investors to start raising the odds of Fed rate cuts.”

The other way to respond is: this is nice, but if things are really slowing down, at some point it will not be job openings but actual jobs that disappear, and that would be bad, so please, Fed, cut before things go south.

Fed governor Chris Waller was (to my surprise) quite prescient in his view that, in this cycle, lower labour demand would show up in falling job listings rather than lost jobs. He has argued that this phenomenon, historically, holds true when the job openings rate (openings/employment) is above about 4.5 per cent (hat tip to Troy Ludtka of SMBC Nikko Securities America for pointing this out). The openings rate, which peaked at 8 per cent in spring of 2022, is now at 5.1 per cent and falling steadily. It is therefore not crazy to think that, on current trends, job losses could be in our future, bringing recession risk along with them.

It is a question of whether we are living through post-pandemic normalisation, or an economic slowdown.

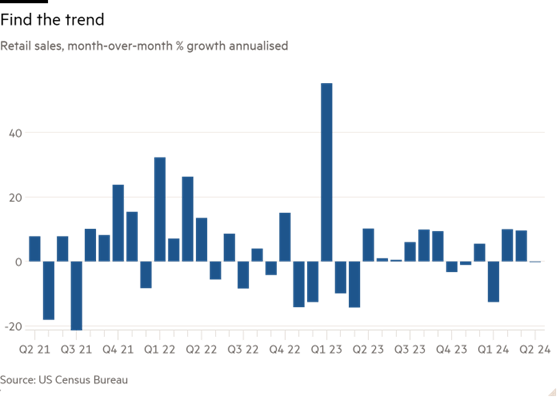

Let us look for other signals. In my previous discussion of the PCE report, I concluded that a month of weak spending does not make a slowdown, but falling disposable incomes were an ill omen. Another look at the vigour of the consumer, the retail sales report, was similarly inconclusive. April retail sales were flat, but the series is very choppy. I can’t pick out a pattern here:

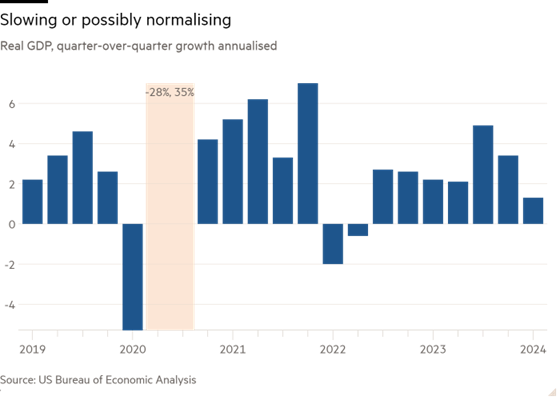

The downward revision in first-quarter real GDP that spooked everybody last week might have been expected, given that the third and fourth quarters of last year were so extraordinarily strong (I have taken the middle quarters of 2020 out of this chart because the changes were so large as to make the rest of the chart illegible; that period is highlighted):

In any case, the revised GDP growth rate, 1.3 per cent, is still meaningfully positive and not far from US trend growth. This could be a picture of benign normalisation.

The really dreary news comes from survey data, such as ISM Manufacturing. The latest data came out Monday; it was lousy. Here is the new orders component of the survey:

There is not much good to say about this, except to plead that the very low readings of early 2023 did not presage economic disaster.

Don Rissmiller of Strategas, least hysterical of Wall Street economists, says it is simply too early to call an economic inflection point. He says in this cycle, the two indicators that have provided the most reliable signal — the ones that earlier suggested the much-feared recession would not come — were the jobless rate and credit spreads. Both still look good. “Is it possible that the economy is slowing? Sure. But that is what tight monetary policy is supposed to do, and if it is doing that without rising unemployment, that is good news, not bad news.”

Dario Perkins of TS Lombard agrees. “A lot of this is noise,” he says of the April data. Normal seasonal patterns were thrown out of whack by the pandemic. It is rising unemployment that marks the difference between normalisation and recession risk, because unemployment brings lower spending, lower business revenues, and lower investment in its wake.

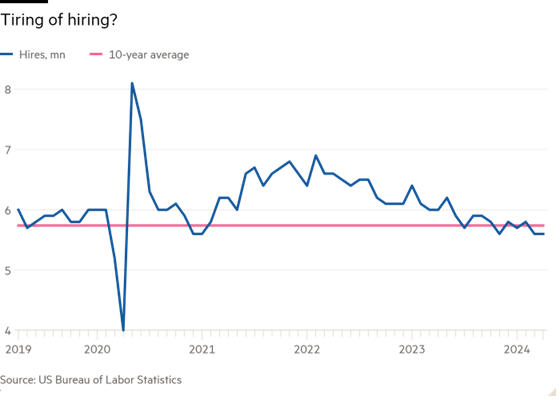

So all eyes will be on Friday’s jobs report for May. But the low unemployment rate (it is still less than 4 per cent) and steady prime-age employment to population ratio (over 60 per cent) conceals a slightly more worrisome story, as Skanda Amarnath of Employ America pointed out to me. The reason that the unemployment rate is low is that quits and lay-offs remain low — workers and employers are not eager to risk changes. This conceals a rather low and definitely falling rate of hiring:

“If hiring keeps falling,” Amarnath says, “We’re going to have issues.”

Copyright The Financial Times Limited 2025

© 2025 The Financial Times Ltd. All rights reserved. Please do not copy and paste FT articles and redistribute by email or post to the web.

This article was legally licensed by AdvisorStream