Claire Ballentine

Sept. 20, 2024

Three little numbers can drastically alter the course of your financial life. Credit scores are a key tenet of American consumer financing[1], used by lenders to judge how well an individual can pay back their obligations. But they’re also part of a confusing, opaque system that even some experts don’t fully understand[2].

And right now, if you’re a prospective borrower, your credit score could be more important than ever. In the US, interest rates are starting to budge from their highest level in decades, which could mean the time has come for you to consider a big purchase, such as a house, a car or even appliances. People with better (read: higher) credit scores can usually get more favorable terms for, say, mortgages or car loans, which can potentially save tens of thousands of dollars in interest payments over the lifetime of the loan. But what determines a credit score? And why do we use this system in the first place?

iStock-2162952418

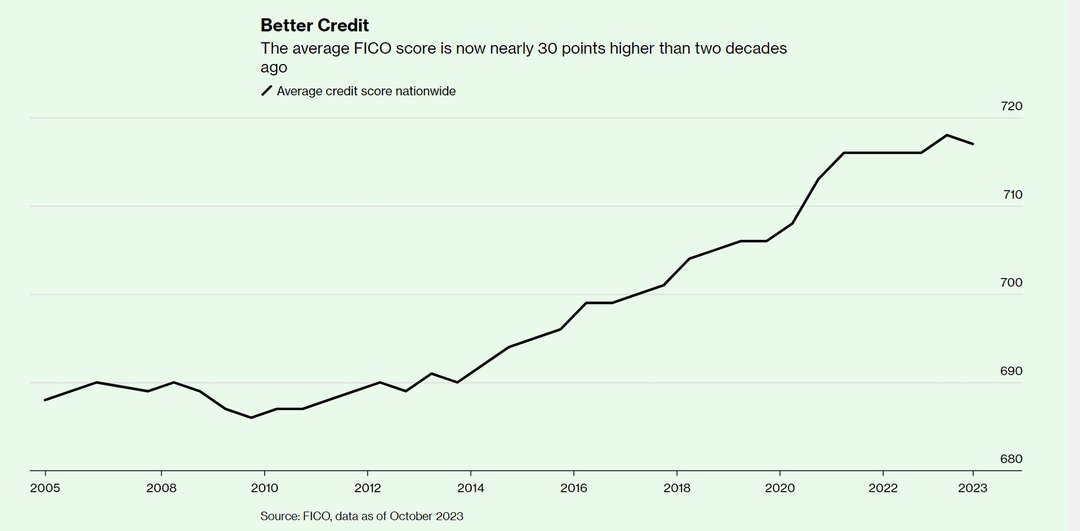

Lenders have long sought ways to determine whether borrowers are trustworthy, but the first true credit score was introduced in 1989. Fair Isaac Corporation, which now goes by FICO, created a model that used credit bureau data to generate a three-digit number summarizing an individual’s creditworthiness. That helped cut down the lengthy loan approval process. Many lenders today use FICO scores, but there’s another model called VantageScore, which started in 2006.

Both FICO and VantageScore use data from credit reports to generate a score ranging from a low of 300 to a high of 850. They consider factors such as a borrower’s payment history, age and type of credit, and percentage of credit limit used. There are three major providers of consumer credit reports in the US: Equifax, TransUnion, and Experian.

Anyone who’s ever had a credit card or a loan from a financial institution has a credit score[3]. To find yours, you can usually check your credit card or other loan statement, or a free credit score site like Credit Karma or SoFi. A note of caution: You don’t just have a single credit score — different sites and sources might show you a different score depending on their model or when they pulled the information.

If you’re going to apply for a mortgage or a car loan in the near future, improving your credit score can lead to big savings. Say you’re taking out a 30-year mortgage of $250,000. If you had a FICO score of 670, you could save about $161 a month, compared with someone with a 620 score, according to Experian. In total, that would result in $57,842 less in interest payments over the loan’s duration.

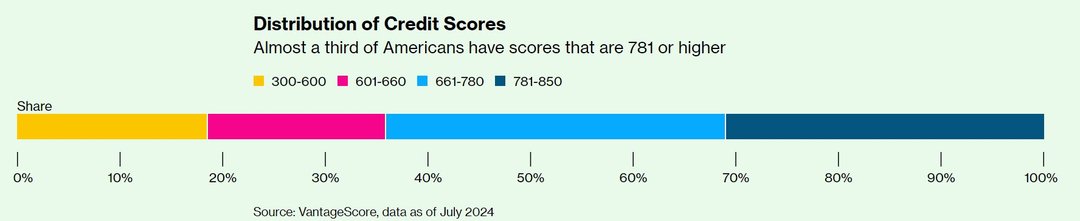

There are four general tranches of credit scores: poor, fair, good and excellent. Where you fall, and what counts as a “good” credit score, depends on which model is being used. But in general, scores in the low-600s and below are considered poor, while those between the low-600s and mid-700s are fair to good. Those above the mid-700s are excellent.

No matter what your standing is right now, here are some ways to improve your credit score.

Pay on Time

The best way to get a better credit score is simply to make your credit card and other loan payments on time. It sounds boring, but this is the biggest component of your score, said Margaret Poe, head of consumer credit education at TransUnion. Try setting up auto-payments for your bills whenever possible, or a calendar reminder each month. Obviously, paying down credit card or personal loans — “bad” debt — will give you a boost, too.

Use Your Credit

The next largest aspect of your score is your credit utilization — the amount of credit you use compared with the amount available to you. For instance, if your credit card has a $10,000 limit and it has a $5,000 balance, then your credit utilization is 50%. Experts recommend trying to keep this figure below 30% if possible. It might be easier than you think to improve yours — and is probably the single quickest way to hack your credit score, if you’re able. “A phone call to the credit card company can often raise your credit limits right away,” said Noah Damsky, principal at Marina Wealth Advisors. If your credit card had a $50,000 limit, say, and your balance is $5,000, suddenly your credit utilization is only 10%[4].

Don’t Cancel Old Cards

Another simple trick: Don’t cancel old credit cards. That’s because your credit history is a significant component of your credit score, and an old card likely has a strong history of payments, according to Ryan Johnson, founder of Hundred Financial Planning. If you do need to close a credit card for some reason — maybe you just have way too many — pick a newer one[5].

Avoid Hard Checks

Make sure you apply only for credit that you truly need. Whenever you submit an application for a loan, the lender typically does what’s called a “hard inquiry” or a “hard pull” to check your credit history. This can cause your score to dip — albeit temporarily — since being in the market for credit can be predictive for risk (as in, you might be in trouble and more likely to default on payments), according to Jonah Kaplan, senior program manager at the Consumer Financial Protection Bureau. However, there’s no need to panic; your score should bounce back quickly[6].

Diversify Your Loans

Try to diversify the types of loans in your name. People with the highest credit scores usually have a mix of loans in their name — a car loan, a mortgage, a few credit cards — for which they make on-time payments[7]. Obviously, don’t go out and get a mortgage just to improve your credit score. But if you see a new credit card that would fit well into your life, getting that card (and paying it off each month) can help build out your credit history, according to Jeff Richardson, senior vice president of marketing at VantageScore.

Monitor Your Score

Check your credit score and credit report regularly. You can pull your credit report from each of the three bureaus using annualcreditreport.com. That can help you know where you stand, and also alert you to any errors that could be dragging down your score, said Phillip Durbin, financial planner at Generational Wealth Development. If there is an error, you can dispute it with the credit reporting company. All the credit bureaus will also allow you to freeze your credit for free, which means no one can pull your credit report without your permission. This also cuts down on the risk of any fraud or errors.

Self-Report Payments

You can also self-report good behavior that might not be already available to credit bureaus. This includes bills for rent, cell phones and utilities that you’re paying on time. Although you can’t report the info directly, there are several third-party services such as PayYourRent and RentTrack that can help. A tool called UltraFICO allows you to report your banking activity, such as your savings and checking account statements.

Help Your Kids

If you have kids or other dependents, you can add them as an authorized user on your credit card (when they’re ready and responsible), which can help them build up a credit history early. Just make sure to keep an eye on your statements for any unapproved spending sprees.

[1] Countries tend to have their own systems for judging credit scores; some are more intricate than others.

[2] Which is why a site such as freecreditreport.com has had such enduring popularity with web-savvy consumers ... although some of that appeal may come from all of those earwormy commercials from the '90s.

[3] According to the CFPB, as many as 26 million Americans are "credit invisible," meaning they have no credit history. That classification limits their ability to qualify for loans or credit cards.

[4] This is just a hypothetical example; in reality, a combination of mortgages, car loans and credit card debt will factor into this ratio.

[5] You could even just stash the old credit card in a safe spot and never use it. Simply having that account open will help your credit score.

[6] If you’re in the market for a mortgage or another kind of loan, and you submit applications or requests to several different lenders within a few days, credit bureaus will normally consider this just one inquiry, instead of multiple. So don’t be afraid to shop around for big loans.

[7] Paying off a loan can sometimes cause your credit score to dip, too — but this is usually just temporary, your score will bounce back.

© 2025 Bloomberg L.P.