Philipp Carlsson-Szlezak and Paul Swartz

Aug. 16, 2024

MODELS AND FORECASTS CAN BE SEDUCTIVE, BUT IT’S TIME FOR EXECUTIVES TO RECLAIM THEIR ECONOMIC JUDGMENT.

OVER THE PAST FIVE YEARS corporate leaders and investors have had to digest a rapid succession of macroeconomic shocks, crises—and false alarms. In 2020, when the pandemic delivered an intense recession, leaders were told it would be worse than 2008 and potentially as bad as the Great Depression. Instead a fast and strong recovery unfolded. In 2021, when supply bottlenecks and strong demand sent prices soaring, a common view was that runaway inflation would take us back to the ugly 1970s. Instead inflation fell from 9.1% to just above 3% in a year. In 2022, when U.S. interest rates climbed, a cascade of emerging-market defaults were predicted—but they didn’t materialize. Also in 2022, and again in 2023, public discourse cast an imminent recession as “inevitable.” Instead a resilient U.S. economy not only defied the doomsayers but delivered strong growth.

iStock-1762856937

For executives and investors such whiplash comes with two types of costs: financial and organizational. Consider the financial cost to automakers that reduced their semiconductor orders in 2020 because they misread the Covid-19 recession as a protracted economic depression. That meant they missed out on sales during the roaring recovery. And leaders can lose the trust of their organizations if they overreact to false alarms with abrupt reversals in strategy, operations, and communications. Clearly, getting the macro call right really matters.

The current turmoil is particularly painful because it comes after 40 years of relative calm. Many executives built their careers and businesses with powerful structural winds at their backs. In the real economy, volatility moderated and cycles grew longer. In the financial realm, inflation fell gradually for decades and pulled interest rates down with it. Around the world, a convergence of institutional arrangements encouraged executives to build a global web of value chains. Yes, setbacks occurred, chief among them the global financial crisis of 2008. Nonetheless, for most of the past few decades, macroeconomic risks have taken a back seat in boardrooms.

Today faith in such stability has been shaken. Shocks and crises are back—but as we have shown, so are false alarms. Without an understanding of the forces that drive disruptions, executives will have a hard time keeping their balance as economic conditions, and the narratives around them, seesaw violently. Shocks and crises pose a real threat, but so does overreaction to them. And for every true crisis there are many false alarms. Understanding macroeconomic risk—the potential for negative or positive change, both cyclical and structural—is essential to responding to these threats with rational optimism.

In this article we will outline how leaders can better discern which risks are genuine. We will also sketch the landscape of real, financial, and global economic risks they face and demonstrate how risks in each category can be approached. Understanding risk is not about building the right model—no matter what many economists will tell you. To be sure, perfect foresight is impossible even if we look beyond the confines of modeling. But executives can cultivate their judgment—and use it to see past the headlines, to identify key causal narratives, and ultimately to make better calls.

RECLAIMING MACROECONOMIC JUDGMENT

For all its scientific veneer and Greek-letter equations, the discipline of macroeconomics offers no precise instruments for business leaders to rely on. No economic model succeeded in predicting the shocks of the past five years while avoiding the false alarms. If anything, the field contributed to the problem, by inviting knee-jerk and too-confident reactions to volatile data flow.

Still, by embracing three analytical habits that can result in better macroeconomic judgment, leaders stood a fair chance of recognizing the false alarms mentioned above. The key is an approach that values contextual flexibility over theoretical rigidity, rational optimism over doom mongering, and judgment over prediction.

LET GO OF MASTER-MODEL MENTALITY. No single theory or approach can provide a consistently accurate economic forecast. The track record of such forecasting is so poor that economic models are rarely a source of insight and often one of false alarms. Surprisingly, the common belief that sophisticated models yield precise and useful answers has persisted even as misguided predictions have piled up.

Models are unreliable because macroeconomic relationships are context-dependent and use small sample sizes. For instance, each recession in the United States since World War II was the result of a highly idiosyncratic constellation of drivers, and there were only 12 of them. Thus supposedly scientific recession modeling is often remarkably unscientific.

That criticism isn’t new. More than a century ago the economist Ludwig von Mises railed against the “fallaciousness” of assuming “constant relations” in economics. John Maynard Keynes drew a distinction from the natural sciences by saying that economics is “not constant through time.” And Friedrich Hayek thought it an “outright error” that economics tries to “imitate…the brilliantly successful natural sciences.” But instead of heeding such warnings, the discipline has added layer upon layer of scientific veneer that is of little use to leaders who must navigate volatility in the real world.

Compounding this problem is the fact that models and their forecasts are least reliable when they are most needed: in times of crisis. When the economy is in free fall, executives are understandably desperate for guidance as to what might happen next. But by definition, crises generate extreme data points—so in situations where predictions would be most valuable, the models are asked to extrapolate beyond the data on which they were built.

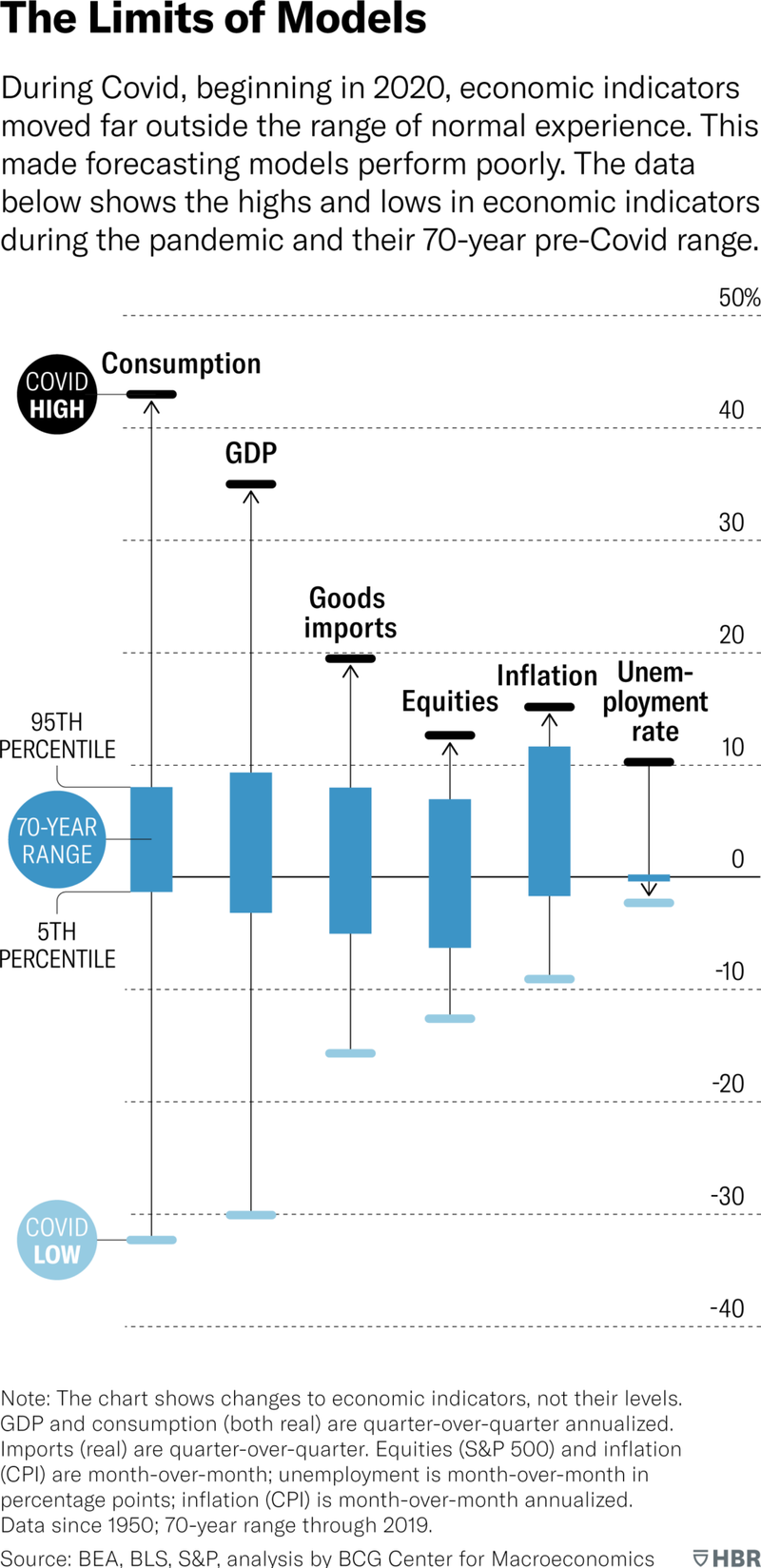

The Covid pandemic illustrated this clearly. Several important indicators—including changes in GDP, consumption, imports, and unemployment—swung so dramatically that they were far outside the range of typical historical experience. Take, for example, the monthly change in the U.S. unemployment rate: In 90% of the months over the past 70 years it has shifted up or down by just 0.3 percentage points or less. But in April 2020 it increased by 10.3 percentage points. The idea that a path to economic recovery could have been precisely modeled when the models had never before seen such shifts is laughable.

DISCOUNT DOOM MONGERING. Leaders must contend with a constant drumbeat of headlines foretelling disaster. Why the negative bent? Simple: Doom sells. Economic and financial journalists rarely have an opportunity to write about sex, crime, or celebrities. Crises and collapse are reasonable substitutes in a competition to attract eyeballs and generate clicks. That is true across television, print, and online media. And even the most respectable outlets, along with pundits and commentators, reliably dial up negative coverage. Thus false alarms are amplified as the microphone is inevitably passed to the loudest pessimists in the room, who grab airtime by confidently portraying long-shot if valid risks from the edges of the risk distribution as being at its very center.

Public discourse does not hold the doomsayers accountable. Predicting the 2008 global financial crisis provided rich rewards for perennially bearish commentators—but looks less impressive considering that those same pundits predicted another dozen crises that somehow didn’t materialize. A broken clock is right twice a day.

Without judgment of their own, executives have little to protect them from the pull of this negativity. Leaders need to choose their clicks wisely and remember who is speaking and from what perch. They don’t have to follow every news cycle that spins the latest data point into a story of collapse. And they must be able to quickly calibrate the stories they do spend time on by asking, simply: What would it take for this to happen?

PRACTICE JUDGMENT THROUGH ECONOMIC ECLECTICISM. There is an alternative to master models and doom scrolling. To stand a better chance of getting macroeconomics right, leaders must develop a situationally aware mindset that is focused on causal persuasiveness and coherence of narrative. Inputs to this sort of judgment should come not only from economics but also from adjacent (and far-flung) disciplines and methods. Sometimes frameworks help us understand risks; sometimes historical episodes are illuminating; sometimes even formal economic models can be useful. Narratives about how the system works matter and can be used to stress-test the bold claims in economic debate. And once it is understood that macroeconomics lacks the analytical elegance of, say, physics, leaders can more confidently bring in broader perspectives and methods. Macroeconomics is not best suited to be a soloist; it plays better as part of a band.

An eclectic approach is accessible to and appropriate for those with inquiring minds—a group that includes many business executives and investors. Equipped with curiosity and judgment, leaders should not be intimidated by number crunchers and model-wedded forecasters, whose grasp of risk and context may be far weaker than their own. Economic eclecticism doesn’t seek to shut down debate the way model-generated “truths” do. It encourages rigorous argument, which is the cornerstone of good judgment.

Executives know that leadership is about navigating uncertainty. If the future were readily predictable, leading would be no more than execution. Assessing economic risks involves a combination of knowledge, skill, and experience—in a word, judgment.

Let’s turn to specific demonstrations of eclectic judgment, looking at risks within the real, financial, and global domains.

THE REAL ECONOMY: HOW TO AVOID FALLING FOR THE WORST CYCLICAL CALLS

The real economy concerns ups and downs in the production and consumption of goods and services, and it often dominates perceptions of the macroeconomic risk landscape. That is only natural: The ability to anticipate coming recessions or incipient recoveries is particularly valuable to executives.

But forecasting macro cycles remains fiendishly hard, as the pandemic illustrates. Why was the recovery from Covid predicted to be far worse than what followed the global financial crisis of 2008? Because cyclical models often anchor on the unemployment rate. After 2008 that rate rose to 10% and then took many years to come down. Thus in 2020, when unemployment spiked to near 15%, the models concluded that the recovery would be even more sluggish. Master-model thinking unwittingly and erroneously extrapolated from the shock’s intensity to its legacy, feeding narratives of a “Greater Depression.”

However, an eclectic approach showed early on that intensity and legacy are not causally linked. The long-term scarring of an economy—the cause of a poor recovery—requires that the economy’s capacity (the supply side) be damaged. To leave scars like those of 2008, a crisis must cripple balance sheets, slow investment and the growth of capital stock, break the labor market, and collectively undermine productivity growth.

We can conceptualize the legacy of a crisis by distinguishing between recovering to the precrisis trend of output and recovering to the precrisis growth rate. After the global financial crisis, the United States eventually achieved a growth rate similar to the one prior to the crisis. But output never regained its precrisis trend. Too little investment occurred, and too many skills were lost, leaving a permanent scar on the economy’s supply side and lowering the economy’s future potential. Yet despite the far greater intensity of the Covid recession, the economy made a successful return to both output trend and growth rate.

Could that “V-shaped” recovery have been foreseen? Even in March and April of 2020, when consensus suggested a lengthy recovery, it was possible to outline a narrative in which the recovery was full—as we did in “Understanding the Economic Shock of Coronavirus” (HBR.org, March 27, 2020). Of course, Covid’s intensity had the potential to cripple balance sheets and degrade capital, labor, and productivity. But comparisons to either 2008 or the 1930s failed to look at a full range of drivers and ask: What would it take?

An eclectic (and rationally optimistic) view of the recovery focused on the many drivers of supply-side damage and the instruments to prevent it. Comparisons to 2008 failed to see that 2020 lacked an investment bubble, or leveraged balance sheets, or a rickety financial system—even if the later recession was more intense. And comparisons to the Great Depression lacked an appreciation of what delivered that catastrophe: persistent policy failure as those in charge stood by and watched the economy bleed out. During the pandemic, political interests in the United States aligned—despite extreme partisanship—to deliver “existential” stimulus.

No model or forecast could compete with an eclectic view of recovery potential, which was about so much more than macroeconomics. It required a reading of supply-side risks and policy instruments to offset them, of finance and the health of balance sheets, of crisis politics and the nature of stimulus, of history and structural changes since prior crises, and of the capacity for societal adaptation. In short, it required judgment. Even with a coherent narrative about drivers, it was not possible to deliver a precise forecast of recovery. But it was possible to deliver a rationally optimistic call that avoided doomsaying.

THE FINANCIAL ECONOMY: HOW TO CALIBRATE SYSTEMIC RISK

Leaders may be less aware of financial risks than of real-economy shocks, but those risks bring both cyclical jeopardy and systemic peril. This part of the risk landscape contains a wide range of potential threats: gyrations in inflation and interest rates, a reliance on stimulus, a proclivity for bubbles, and the prevalence of debt.

One particularly thorny, persistent source of economic anxiety is public debt. When does a government’s debt threaten its economy or risk igniting a financial crisis? Consider this perspective:

With every deficit year the indebtedness of the U.S. government goes up, and with it the interest charges on the U.S. budget, which in turn raises the deficit even further. Sooner or later…confidence in America and the American dollar will be undermined—some observers consider this practically imminent.

Although this could have been written in 2024, Peter Drucker wrote it in 1986. In the nearly 40 years since then, the U.S. public debt has risen almost without pause while the value of the dollar has neared record highs in recent years. Rather than being a cause of crises, that debt has been a critical solution to them several times over, such as in 2008 and 2020. Meanwhile, Germany and other economies that put austerity above the use of debt have underperformed the United States.

Why, then, the existential angst? The perennial prediction of a U.S. debt crisis invariably anchors on debt levels, suggesting that some tipping point will trigger systemic unraveling. Influential economists, including Carmen Reinhart and Kenneth Rogoff, have worked to wrap this idea in scientific precision. Reinhart and Rogoff argued in 2010 that exceeding a debt-to-GDP ratio of 90% would lead to collapsing growth. Thresholds like that not only failed to predict debt problems but also fed into misguided post-2008 austerity narratives and spread unjustified gloom.

Executives looking at public debt to assess systemic risk—not just in the United States—should spend less time thinking about debt levels and more time thinking about interest rates versus growth rates. The interplay between those two determines an economy’s ability to pay its debt. When the growth rate is higher than the interest rate, all the interest can be paid for with new debt without raising the debt-to-GDP ratio. But when the interest rate rises above the growth rate, the economy must set aside income just to keep the ratio stable.

Thus, calibrating the risk from public debt involves asking whether interest rates could durably rise above the growth rate of GDP. In the United States, although long-term interest rates are likely to be higher in the 2020s, it’s difficult to see how they will be persistently above nominal growth. But even when growth drops below interest rates, it is not automatically “game over.” It does, however, become costly and force trade-offs. Fiscal profligacy is always unwise.

The question of public debt demonstrates that executives must remain vigilant about economic models and doom mongering in the media when it comes to financial risk. Rather than anchoring on a clear but questionable metric (debt levels), an eclectic leader searches for key drivers, constructs narratives, and evaluates their coherence by drawing on a rich range of sources. In this case the key driver is the interplay of interest rate and growth rate—and the numerous factors that have a role in determining them.

THE GLOBAL ECONOMY: HOW TO NAVIGATE DIVERGENCE

Today geopolitics appears to occupy an ever-greater share of the risk landscape, which is particularly challenging because it was relatively calm for so long. A multidecade trend toward the global convergence of political, security, economic, and financial systems had made geopolitics all but irrelevant in macroeconomics. Now global divergence forces leaders to rapidly climb a risk-management learning curve. Surely geopolitical turmoil casts a shadow on the global economy.

But does it really? We cannot model the impact of geopolitics on the global economy with any real confidence. Not even the simple direction of the relationship (positive or negative) can be assumed.

Consider the two world wars. When World War I broke out, the stock market dropped 10% in three days and was subsequently closed down. When it reopened 136 days later, it was down another 20%. The fall captured a seemingly straightforward pass-through from geopolitics to economic impact.

Yet when World War II broke out, the U.S. stock market jumped 13%. This time a geopolitical calamity materially improved the economic backdrop in the United States. That’s because World War II delivered an enormous demand boost to the U.S. economy, effectively (and finally) ending the Great Depression. Though the downside of geopolitical stress, crisis, and conflict is real and can be catastrophic, the ability to predict flashpoints or their knock-on effects remains poor. And even when a geopolitical outcome is accurately predicted, understanding its economic impact is an entirely different undertaking, as demonstrated above.

The best way to navigate such uncertainty is by trying to predict not whether or when the gun will fire but how the bullet will ricochet through a complex maze of real, financial, and institutional channels. To begin with, the economic factor with the greatest impact may be the policy response rather than the geopolitical event itself. The big lift to the U.S. economy from WWII didn’t come until the country’s full mobilization after Pearl Harbor.

The present hears many echoes. The war in Ukraine has barely left a mark on the U.S. economy. The eurozone, much more directly exposed, escaped a downturn over the past two years, defying the commonplace extrapolation that this shock would lead to a recession. Similarly, multiple conflicts in the Middle East—as devastating as they’ve been for the economies in its midst—have left few marks on the global economy, because the linkages are few and the workarounds many. This is not calloused or nihilistic: Wars and geopolitical hostilities rightly dominate debate because of their devastating human toll—and because they can escalate. But that doesn’t make economic doom mongering accurate. Leaders tasked with gauging the impact of geopolitical shocks on the macroeconomy need to dig deeper.

What can improve the odds of making the right call? Regarding the real economy, we should ask: Will a geopolitical shock change spending power? Will it change the calculus of investment? Regarding the financial economy: Will geopolitics change credit creation or intermediation? Will it undermine or weaken companies’ balance sheets? And on the institutional front: Will it change the explicit or implicit rules of the road? This is just an abbreviated list, but it illustrates how context and reaction, rather than the shock itself, define the economic impact.

THE CASE FOR RATIONAL OPTIMISM

Our helicopter tour of real, financial, and global risks highlights pitfalls and opportunities for leaders, who can’t rely on forecasts and the media to provide answers. As with every other aspect of leadership, they must ultimately exercise judgment.

Letting go of prescriptive models, actively leaning against the doomsaying slant in public discourse, and taking an eclectic perspective will give executives a better shot at calibrating macroeconomic risk—even if outcomes cannot consistently be predicted. Those who are willing to do this work will also discover a more optimistic take on the future. Despite the menacing landscape, we believe that an era of economic tightness should make executives feel upbeat about the prospects for the U.S. economy.

In the real economy, structurally tight labor markets will keep workers in short supply. That will push companies to invest and discover productivity gains in order to contain labor costs. Growth opportunities will outweigh growth risks in the years ahead. In the financial economy, tighter utilization of both labor and capital will deliver higher interest rates. Though they strain the economy and pose systemic risks, we see them as good on balance, because they lead to better capital allocation. And in the global economy, continued convergence would have been preferable, but divergence will also boost the U.S. economy in the years ahead: It will drive more capital expenditure in domestic manufacturing alongside strategic investment in other needs such as decarbonization and AI. New recessions will come, but they are unlikely to end the era of tightness.

The “dismal science” of economics and our clickbait culture of public discourse are a perfect match to fuel simplistic narratives of doom. To avoid false alarms and achieve a true assessment of macroeconomic risks, leaders should look past both to reclaim their own judgment.

c.2025 Harvard Business Review. Distributed by The New York Times Licensing Group.

This HBR article was legally licensed through AdvisorStream.