Andrew Beattie

May 27, 2024

Making sure that you have the right financial resources in place, including life insurance, is important if you have loved ones who depend on your income. Life insurance can help cover funeral and burial expenses, pay off remaining debts, and make managing day-to-day living expenses less burdensome for those you leave behind.

Here's how to find out if you need life insurance at all or, if you already have it, how to evaluate your coverage needs and determine whether your policy is sufficient.

KEY TAKEAWAYS

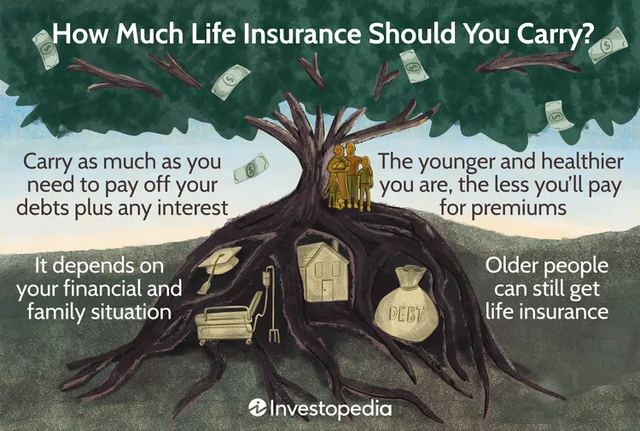

- Your financial and family situation will determine whether you need life insurance and, if so, how much coverage you should have.

- The younger and healthier you are, generally, the less you’ll pay for premiums, but older people can still get life insurance.

- It may be wise to carry as much life insurance as you need to pay off your debts plus any interest, particularly if you have a mortgage or co-signed student loans.

- Your policy’s payout should be large enough to replace your income, plus a little more to hedge against the impacts of inflation on purchasing power.

- There are several rules of thumb for computing the ideal amount of coverage.

Investopedia / Jessica Olah

What Is Life Insurance?

Life insurance is an agreement in which an insurance company agrees to pay a specified amount after the death of an insured party, as long as the premiums are paid and up to date. This payout amount is called a death benefit. Policies give insured people the assurance that their loved ones will have peace of mind and financial protection after their death.

Life insurance falls into two main categories: permanent and term. Permanent life insurance policies do not have an expiration date, meaning you’re covered for life as long as your premiums are paid. Some permanent life insurance policies offer an investment component that allows you to build cash value by investing a portion of the premiums you pay in the stock market. Term life insurance, on the other hand, only covers you for a set nunber of years. Some policies allow you to easily renew your coverage after a certain expiration date, while others require a medical exam to do so.

Fast Fact: A medical exam is a standard underwriting requirement for most life insurance policies. However, you may be able to purchase no-exam life insurance at a higher premium cost.

Do You Even Need Life Insurance?

Life insurance can be a helpful financial tool to possess, but buying a policy doesn’t make sense for everyone. If you're single and have no dependents, have beneficiaries for your major assets, and possess enough money to cover your debts as well as your final expenses—your funeral, estate settlement, attorney fees, and other expenses—then you may not need life insurance. The same applies if you have dependents but enough assets to provide for them after your death.

But if you’re the primary provider for your dependents or have a significant amount of debt that outweighs your assets, then insurance can help ensure your loved ones are well taken care of if something happens to you. Having a life insurance policy may also make sense if you own a business or owe co-signed debts, such as private student loans, for which someone else could be held responsible if you pass away.

Keep in mind that life insurance by itself doesn’t cover every situation. For example, a standard life insurance policy won’t pay out if you develop a chronic illness nor will it cover long-term nursing care costs. But you can purchase chronic illness riders or long-term care insurance riders for an additional premium cost that can provide living benefits to cover those types of scenarios.

What's the Minimum Amount of Life Insurance You Need?

A large part of choosing a life insurance policy is determining how much money your dependents will need. Choosing the face value—the amount that your policy pays if you die—depends on a few different factors. The minimum amount of coverage you need may be very different from what someone else requires. Financial experts often recommend purchasing at least 10 times your annual income in coverage, although your personal number may be higher or lower.

Tip: If you’re married, then both you and your spouse may need life insurance coverage, even if only one of you is primarily responsible for your household income.

Here are some of the most important considerations for choosing a minimum amount of life insurance.

Debt

Life insurance can be used to pay off outstanding debts, including student loans, car loans, mortgages, credit cards, and personal loans. If you have any of these debts, then your policy should include enough coverage to pay them off in full. For instance, if you have a $200,000 mortgage and a $4,000 car loan, you need at least $204,000 in your policy to cover your debts. You should take out a little more to settle any extra interest or charges as well.

Income Replacement

One of the biggest purposes of life insurance is to replace income. If you are the sole provider for your dependents and bring in $40,000 a year, for example, you will need a policy payout that is large enough to replace your annual income, plus a little extra to guard against inflation.

Life insurance experts suggest having enough coverage to replace at least 10 years of your salary. In this case that would be $400,000. You could also add some extra as a buffer for inflation and other unexpected costs. For this example, then, a $500,000 policy might be reasonable. This would replace your income for your family for at least a decade.

Once you determine the needed face value for your insurance policy, you can start shopping around by talking to an agent or using an online insurance estimator to determine how much insurance you will need.

Insuring Others

Obviously, there may be other people in your life who are important to you, and you may wonder if you should insure them. As a rule, you should only insure people whose death would mean a financial loss to you. The death of a child, while emotionally devastating, does not constitute a financial loss because children cost money to raise. The death of an income-earning spouse, however, does create a situation with both emotional and financial losses.

In that case, follow the income replacement calculation above with his or her income. This also goes for business partners with whom you have a financial relationship. For example, consider someone with whom you have a shared responsibility for mortgage payments on a co-owned property. You may want to consider a policy for that person, as that person’s death will have a big impact on your financial situation.

Fast Fact: If you’re purchasing life insurance to cover a business partnership arrangement, then you may want to consider a key-person insurance policy versus traditional coverage.

How To Calculate Your Life Insurance Needs

Most insurance companies say a reasonable amount for life insurance is at least 10 times the amount of annual salary. If you multiply an annual salary of $50,000 by 10, for instance, you'd opt for $500,000 in coverage. Some recommend adding an additional $100,000 in coverage per child above the 10x amount.

Years-Until-Retirement Method

Another way to calculate the amount of life insurance needed is to multiply your annual salary by the number of years left until retirement. For example, if a 40-year-old currently makes $20,000 a year, they will need $500,000 (25 years × $20,000) in life insurance.

Standard-of-Living Method

This method is based on the amount of money survivors would need to maintain their standard of living if the insured party dies. You take that amount and multiply it by 20. The thought here is that survivors can take a 5% withdrawal from the death benefit each year—the equivalent of the standard-of-living amount—while investing the death benefit principal and earning 5% or better. This type of calculation is sometimes known as human life value (HLV) approach.

Debt, Income, Mortgage, Education (DIME) Method

Another methodology is called DIME (debt, income, mortgage, education). This is meant for a minimal amount of coverage that will cover family expenses in the event of an untimely death. With the DIME approach, your coverage should be enough to cover all your outstanding debts (including your mortgage), pay for your kids' education, and replace your income for the years until your children reach 18 years old.

Alternatives to Life Insurance

If you’re getting life insurance purely to cover debts and have no dependents, there are alternatives. One is to self-insure, which occurs when someone sets aside a pool of money to be used to remedy an unexpected loss, rather than spend it on insurance. Self-insuring against certain losses may be more economical than buying insurance from a third party.

Another option is to forgo buying life insurance if you're single, have beneficiaries to receive your significant assets, and your estate can cover your debts as well as the expenses related to death that would arise after you're gone.

What Is a Rule of Thumb for How Much Life Insurance You Need?

There are several rules of thumb you can use for computing the amount of life insurance you'll need. These often involve multiplying your current income by a number such as 10 or your number of years left until retirement. Other rules of thumb involve adding up all expenses and obligations you need to cover for your family.

Is Life Insurance Needed After Age 60?

While life insurance is often intended to replace the economic loss of someone with a family to support in the event of their untimely death, it can be purchased by those whose children have grown up as well. This can be done for several purposes, including leaving an inheritance, establishing a trust upon death, contributing to a charity, or if the older individual is a key employee or partner in a business. In general, depending on the insurer and type of policy, you can get coverage up to age 100. Note, however, that premiums increase the older you are when you purchase the policy.

What Happens to My Life Insurance if I Lose My Job?

If you lose your job and have private life insurance that you purchased on your own, as long as you continue paying your premiums, you will have coverage. If the insurance was provided as a group plan through your employer, however, you typically will lose that coverage around one month after being terminated. Some group plans will give you the option to switch the coverage to your own individual policy, though the cost could be higher than what you were paying at work.

Can I Cash Out My Life Insurance Policy?

If you own a permanent life insurance policy that accrues cash value (such as whole life or universal life), you can often borrow against or withdraw some or all of that value. The death benefit will typically also decline proportionally to the amount you take out of the policy. If you surrender the entire amount, you will lose all your coverage.

The Bottom Line

Your financial and family details will determine whether you need life insurance and, if so, how much you should have. If you choose to buy insurance, use one of the common methods to calculate the coverage you’ll need, such as 10 times your salary. Do this before meeting with an agent or broker to avoid getting stuck with inadequate coverage or expensive coverage that you don’t need.

As with investing, educating yourself is essential to making the right choice about whether you need life insurance and, if so, what level of coverage. Make sure to do your research to acquire the best life insurance for you.