Diccon Hyatt

Feb. 14, 2024

KEY TAKEAWAYS

- While totals for many types of debt consistently break records, debt levels are not at all-time highs when compared against the economic output of the country.

- Delinquency rates have been rising, suggesting that the debt has become more difficult to pay off in recent months amid high interest rates.

- The national debt, while not at a crisis point, is also a growing burden because of high interest rates.

Whether it’s credit cards, mortgages, student loans, or even the national debt, the amount of money Americans owe just keeps piling up.

How big of a problem is that?

Kseniya Ovchinnikova / Getty Images

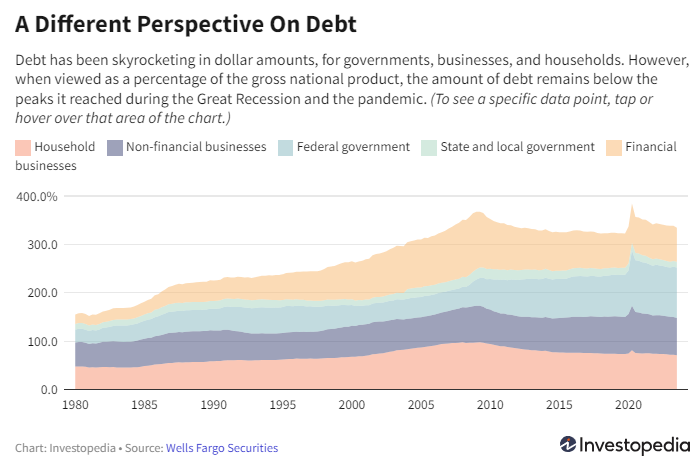

When it comes to economics, sheer dollar values can be misleading, according to economists. Inflation, along with the fact that the population and economy are both getting bigger, means that dollar totals tend to rise over time.

“Larger economies should be able to sustain higher amounts of debt, everything else equal,” Wells Fargo economists Jay H. Bryson and Delaney Conner wrote in a recent commentary. “The correct way to think about debt is not by its absolute level. Rather, the correct way to think about debt is to measure it relative to another economic variable that tends to grow over time.”

As the chart below shows, debt compared to the gross domestic product—a measure of the country’s entire economic output—hasn’t risen steeply and remains below its peak during the Great Recession.

That doesn’t necessarily mean debt is nothing to worry about, however. With interest rates running at their highest in decades thanks to the Federal Reserve’s campaign of hikes, servicing that debt has become much more expensive for households, businesses, and the government. And more people have been falling behind on certain kinds of loans.

For example, the delinquency rate for mortgages rose to 3.88% in the fourth quarter of 2023, up a little over a quarter of a percentage point from the third quarter, the Mortgage Bankers Association said last week. That was slightly lower than the fourth quarter of 2022, and well below the historical average of 5.25%, the MBA said. Still, it indicated increasing stress for household budgets.

“The resumption of student loan payments, robust personal spending, and rising balances on credit cards and other forms of consumer debt, paired with declining savings rates, are likely behind some borrowers falling behind at the end of 2023,” Marina Walsh, the MBA’s vice president of industry analysis, said in a commentary.

There’s also been an uptick in people falling behind on their credit card and auto loan payments.

And the national debt is also becoming more of a concern as interest payments take up a growing share of the budget, potentially hindering the government’s ability to respond to future emergencies.

For households at least, Bryson and Connor have concluded that the debt load is at its most manageable in decades because incomes have risen faster than debts.

“Every major category of household debt (i.e., residential mortgages, student loans, auto loans and revolving credit) has grown in recent years. But household income has risen even more—it is up 85% over the same period—so the household debt-to-disposable income ratio, commonly referred to as ‘leverage,’ is lower today than it was at the start of the housing bubble,” they wrote.

Easing inflation could also give households some breathing room from their debt.

“Lower inflation will lift real income growth and should allow for lower interest rates by mid-year, which in turn will start lowering credit card rates and make monthly payments more manageable,” wrote BMO’s Senior Economist Jay Hawkins.

The Federal Reserve, which has left its benchmark rate unchanged at a two-decade high since mid-2023, has said it is looking for further evidence that inflation is under control before cutting interest rates. On Tuesday, consumer price data showed that inflation moderated in January, but not as much as economists had expected.