Frederick Vettese

Feb. 28, 2024

Putting off retirement for just a little while can significantly boost your retirement income. Consider the situation of a couple who are both age 60 today and are contemplating retirement. They are wondering how much more income they could expect if they wait.

iStock-1188966130

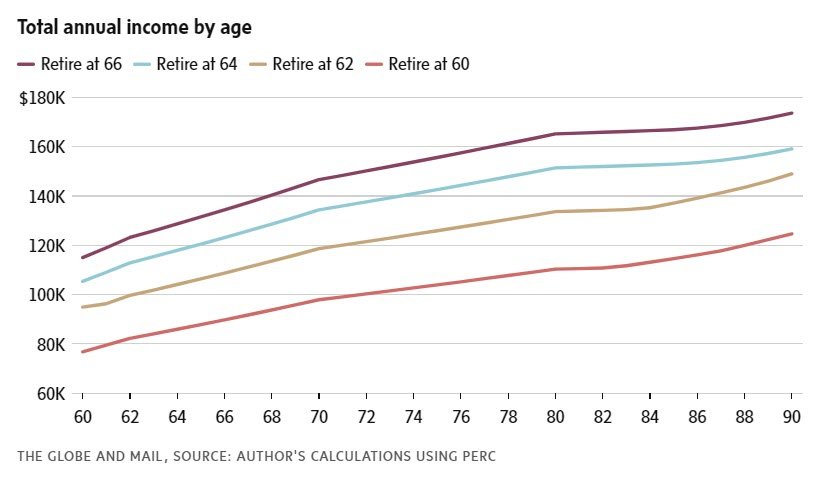

They currently have a total of $600,000 in their RRSPs and another $200,000 in TFSAs. Each is earning $80,000 a year and both are prepared to contribute 30 per cent of pay to RRSPs plus the maximum to their TFSAs if they keep working. The chart below shows the resulting income.

If they were prepared to wait six years and retire at 66, their starting income would be 50 per cent greater than if they retired at 60. Even putting off retirement for just two years will boost their lifetime income by nearly 25 per cent. Is it worth it? It depends on the individual. A good trade-off for many people would be to work part-time into their 60s and possibly beyond. (The calculations were performed by PERC, which is available at perc-pro.ca.)

Some important notes about the projections. I assumed the couple would earn an annual return on their investments of 4.5 per cent less 1 per cent for investment fees. I also assumed that inflation would be 2.2 per cent a year after 2025 and that they use $150,000 of their savings to buy a life annuity.

For every year they continue to work, they augment their CPP pensions because neither had earned the maximum CPP pension yet. The starting age for both CPP and OAS has been optimized in each scenario and may be higher than age 65. All amounts are before income tax.

This Globe and Mail article was legally licensed by AdvisorStream.

© Copyright 2024 The Globe and Mail Inc. All rights reserved.