By Hardika Singh and Charley Grant

April 15, 2024

Expectations that the Federal Reserve would aggressively cut interest rates this year have helped propel stocks to repeated records. Now that the case for rate cuts is weakening, scrutiny of the bull market is intensifying.

iStock image

The S&P 500 has added 7.4% this year and is off a mere 2.5% from its all-time high, set March 28. Stocks have marched higher since 10-year government-bond yields peaked at 5% in late October. That also fueled an “everything rally,” driving up prices for other asset classes from gold to bonds.

But some investors are beginning to worry that future gains in the stock market may be more difficult to come by. Wednesday’s hotter-than-expected inflation report raised questions about whether the Fed can deliver cuts this year without signs of an economic slowdown. At the beginning of the year, Wall Street penciled in six, or even seven, interest-rate cuts through 2024, but now some investors are beginning to doubt that the Fed would lower rates at all.

That could spell trouble for stocks. The yield on the benchmark 10-year Treasury note ended the week at 4.499% after posting on Wednesday its biggest one-day rise since 2022.

Higher yields make stocks less attractive than holding Treasurys to maturity, and they increase borrowing costs across the economy for everything from corporate debt to mortgages to car loans.

“It changes the math,” said Quincy Krosby, chief global strategist for LPL Financial. “You have to recalibrate, you have to adjust, and the rate regime must be in concert with where the valuations are.”

Here are some areas of the stock market that are vulnerable to higher rates:

Small-caps

The small-cap focused S&P 600 index tumbled 3% last week. That included a 2.9% drop on Wednesday after the inflation report, the largest one-day percentage decline since February. Small-caps, which tend to derive most of their revenue from inside the U.S., are especially sensitive to the trajectory of the economy.

One big reason: Small stocks generally devote a much larger share of operating profit to covering interest on debt than larger ones do. The ratio of operating income to interest expense within the S&P 600 was 2.3 times as of March, according to Dow Jones Market Data. That compares with 7.6 times for S&P 500 companies.

They generally issue more floating-rate debt than bigger companies, so their loan payments fluctuate with benchmark interest rates. When rates go up, that means higher interest expenses dent their bottom lines and leave them more at risk of defaults.

About 44% of debt among companies within the Russell 2000, another small-cap index, was floating-rate at the end of last year, compared with 10% for the S&P 500, according to data from Lazard Asset Management.

Adding to the crunch: About 40% of the companies in the Russell 2000 didn’t turn a profit over the past year, compared with 10% in the S&P 500, according to J.P. Morgan Asset Management.

Big Tech

Tech stocks have led the market’s advance since early 2023, powered by a surge in investor enthusiasm for artificial-intelligence technology. The largest companies have strong balance sheets and big cash piles that should insulate them against the effects of higher rates. But some investors worry that their popularity could begin to work against them if sentiment darkens.

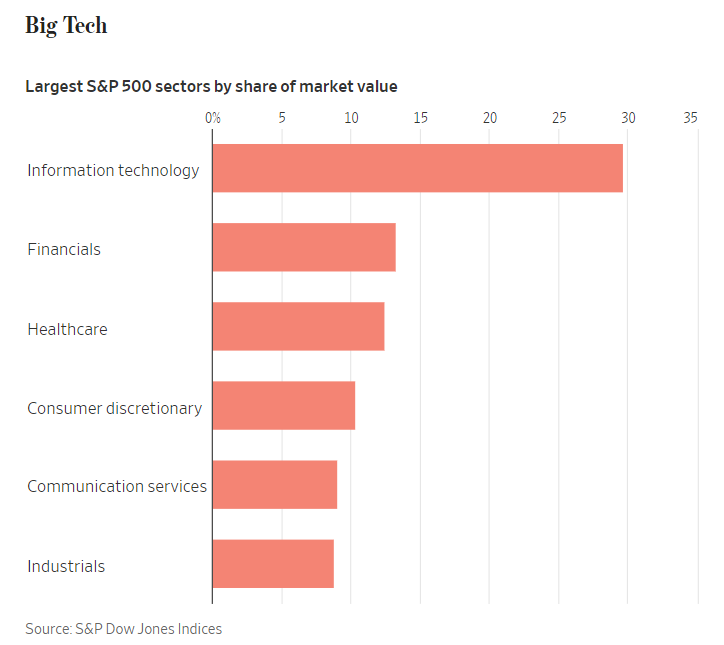

The S&P 500’s information-technology sector accounts for nearly 30% of the market-value weighted index, more than twice the size of any of the other 10 sectors. If investors decide to take profits, tech stocks are a natural place to look.

“Looking at the actively managed mutual funds that are out there, cap-weighted index funds, it’s all the same stuff. Is Microsoft or Nvidia the largest holding; is it Amazon?” said Emerson Ham III, senior partner at Sound View Wealth Advisors. “If you did get a bad cycle in the market, large tech stocks could have a problem.”When the Fed started its interest-rate-increase campaign in 2022, the tech sector closed the year down 30% and the consumer-discretionary sector, home to the likes of Amazon.com and Tesla, declined nearly 40%.

Cyclicals

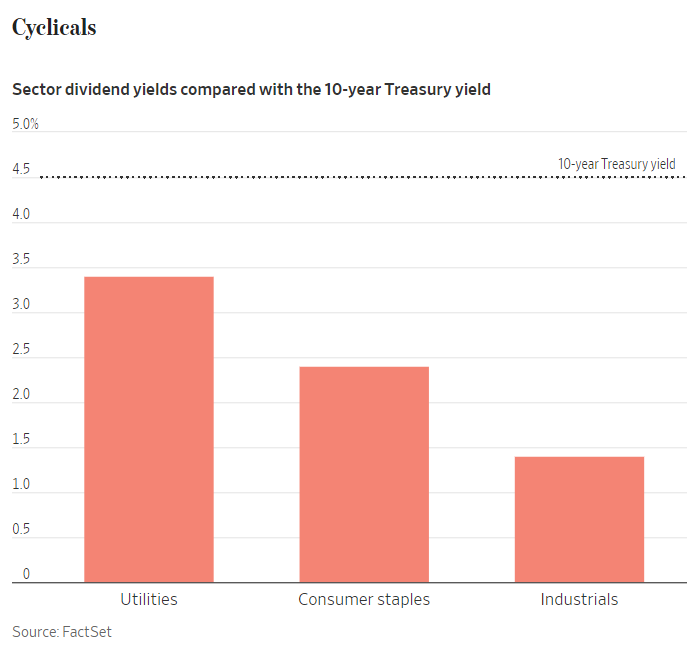

Cyclical stocks that are sensitive to the performance of the economy, such as utilities, consumer staples and industrials, lose their appeal when interest rates are higher, in particular because they are often seen as dividend plays.

The S&P 500’s utility sector boasts a dividend yield of 3.4%, consumer staples pays 2.4% and industrials has a 1.4% yield. Those all seem measly when compared with the 4.5% risk-free rate on government bonds. Besides, the stocks aren’t offering enough extra yield to compensate for the risk of a slowdown in business activity from higher interest rates.

Industrial conglomerate 3M offers a dividend yield of 6.6%, and its shares are down 0.1% this year; consumer-staples company Walgreens Boots Alliance has a yield of 5.6%, and its shares are down about 30%; and American Electric Power pays 4.3%, and its shares are up 1.1%. All three are underperforming the S&P 500.

Around 40 stocks in the S&P 500 have a dividend yield above that of the 10-year Treasury note, according to FactSet. Two years ago when the Fed had just started its interest-rate campaign, there were 94 stocks that offered a higher yield.

Banks

Higher interest rates propel depositors to move money to Treasurys and money-market funds for higher returns, contributing to lower deposits at banks. Meanwhile, banks have had to shell out more interest to yield-hungry depositors, particularly hurting the bottom line at small and midsize banks. Wells Fargo said Friday it expects net interest income, or profit from lending, to decline by 7% to 9% in 2024.

Delinquency rates could also creep higher if interest rates remain high, which could increase loan losses for banks.

Higher interest rates have also pushed up mortgage rates back toward 7%, a level they haven’t seen since December. That has kept many would-be home buyers on the sidelines, leading to sharp declines in mortgage activity at the big banks, a source of revenue.

The S&P 500’s real-estate sector is down 7.2% this year, the worst performer of the 11 segments and the only group in the red.

The rate whipsaw has hit smaller banks harder than big ones. The KBW Nasdaq Bank Index, which includes heavyweights such as JPMorgan, has advanced 2.1% this year, while an index of regional banking stocks is down 13%.

Energy

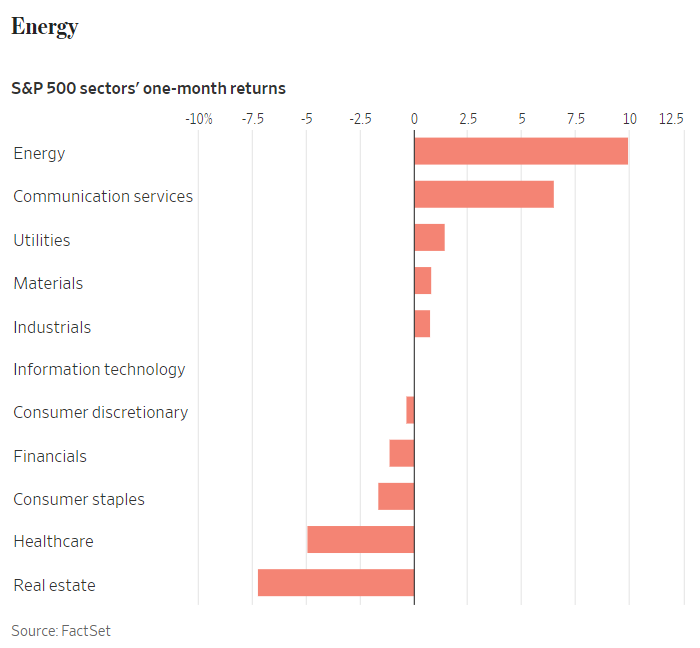

Shares of oil-and-gas companies are making another run after being among the top performers in 2022. Rising oil prices boost revenue for oil-and-gas providers, while big companies in the sector trade at a discount to the overall market. Exxon and Chevron trade at about 13 and 12 times their earnings over the past 12 months, respectively; the S&P 500 trades at roughly 20 times.

The S&P 500 energy sector is up almost 10% over the past month, beating every other corner of the broad index by at least 3 percentage points.

Write to Hardika Singh at hardika.singh@wsj.com and Charley Grant at charles.grant@wsj.com

Dow Jones & Company, Inc.