BONNIE-JEANNE MACDONALD

July 29, 2020

Canadians with RRSP savings that they intend to spend in retirement are missing out on a great financial strategy: using some of those savings as an income bridge to delay their Canada Pension Plan (CPP) benefits. Doing so is the safest, most inexpensive pension that money can buy.

But untangling all the considerations is confusing, since there are infinite combinations of relevant factors that enter into the decision and its outcome – including personal considerations and circumstances, the dynamics of the financial world during retirement, and the implications of Canadian tax and social transfer systems – like Old Age Security (OAS), which includes the Guaranteed Income Supplement (GIS).

SIMPLY COMPLEX

The CPP and its Quebec counterpart, the Quebec Pension Plan (QPP), are iconic Canadian social programs. People love these programs because they’re simple: automatically pay contributions while you work, along with your employer; then, in retirement, collect the benefits earned until you die. And, contrary to popular misconceptions, this program is actuarially sustainable for at least the next 75 years. In other words, your CPP pension is a safe bet.

However, underneath that outward simplicity lies a complicated financial system. That complexity includes generous financial incentives to delay the start of CPP – or QPP – payments.

My new research with the Canadian Institute of Actuaries and the Society of Actuaries, with Marvin Avery and Richard Morrison, demonstrates the clear advantages of this uniquely profitable financial opportunity.

APPLES TO APPLES

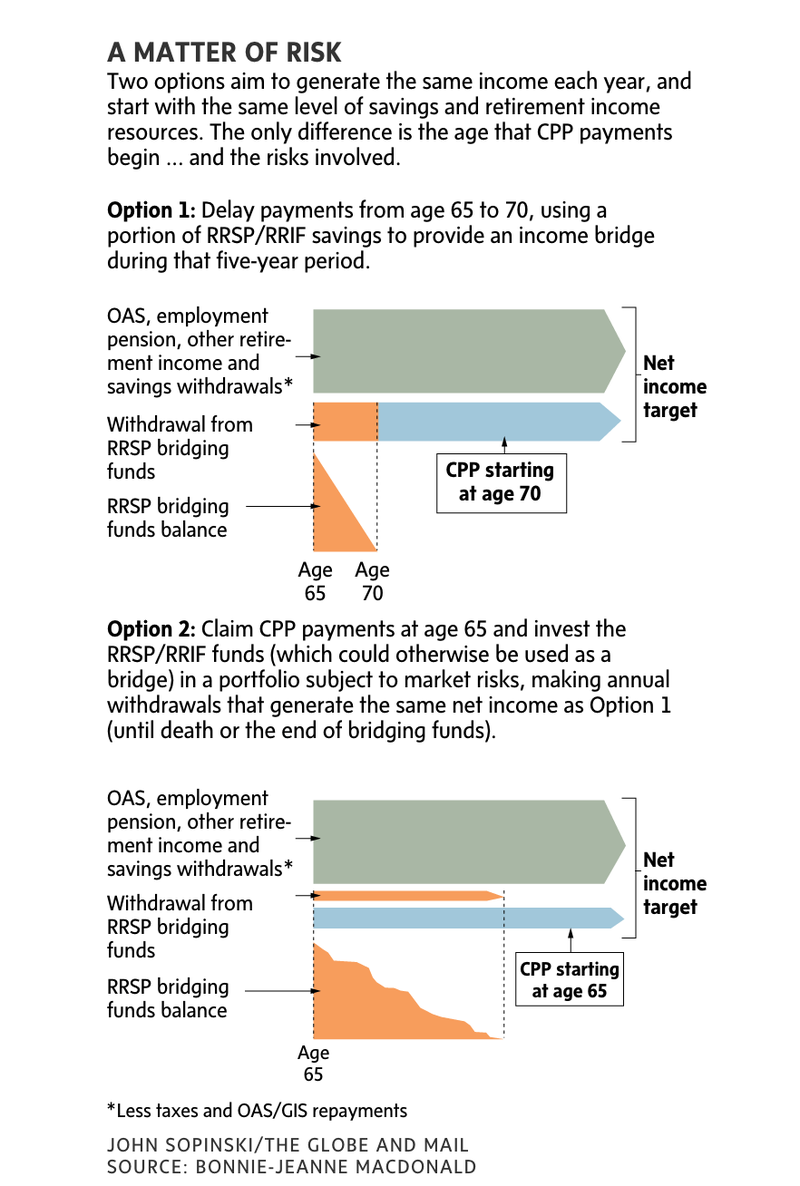

Using the example of a 65-year-old retiring Canadian, the goal of the research was to make a straightforward comparison of two otherwise identical financial strategies, where the only difference is the age that CPP payments start (see graphic).

In our study, we quickly realized the ramifications on personal income taxes and OAS/GIS eligibility are the same in both options as well. (Note that CPP death and survivor benefits are unaffected by the age of CPP uptake, and the same applies to employer pension plan benefits).

So, what’s the difference between these two options? The simple answer is the risks involved.

THE ODDS ARE NOT IN YOUR FAVOUR

Using comprehensive dynamic microsimulation computer modelling, we looked at many (millions) of alternative futures to see how both options played out. In each scenario, income flowed appropriately through the Canadian tax and transfer system, financial market returns moved realistically, and the age of death followed the same patterns as experienced by the Canadian population.

The results showed that most Canadians with RRSP savings are far better off slicing off a portion of their savings in early retirement and using them as a bridge to a higher delayed CPP benefit, rather than stretching out their entire savings over retirement.

For example, if a person takes their CPP benefits at age 65 and invests their RRSP funds in a portfolio that yields an average of 4 per cent after fees, the vast majority would run out of those potential “bridging funds” before they die (70 per cent of the time for males, and 80 per cent of the time for females).

Overall, there is insufficient reward for assuming the risk and related worry of taking CPP benefits earlier, and leaving more money to navigate the challenges of financial markets over the long term.

Of course, there are some exceptions, which I’ll be expanding on in my upcoming book with my colleague, Alyssa Hodder, with the International Foundation of Employee Benefit Plans. For Canadians who have strong reason to believe their retirement will be short (e.g., owing to reduced life expectancy) or who simply can’t afford to delay the CPP payments, this option won’t be viable. Or, if a person’s RRSP funds are intended entirely as a bequest, then using some of them toward delaying your CPP benefit (and getting more secure pension income) is not on the menu.

But for the rest, even though it may seem counterintuitive, taking CPP early is the riskier option.

Delaying CPP benefits can put you on the path toward a more financially secure future – and your older future self will thank you for your foresight.

Bonnie-Jeanne MacDonald, PhD FSA FCIA, is the director of financial security research at the National Institute on Ageing (NIA) at Ryerson University, fellow of the Society of Actuaries, fellow of the Canadian Institute of Actuaries, and resident scholar at Eckler Ltd.

This Globe and Mail article was legally licensed by AdvisorStream.

© Copyright 2024 The Globe and Mail Inc. All rights reserved.