By Srivindhya Kolluru | Contributing Columnist

April 29, 2024

Turning 71 is an important milestone for Canadians as it marks the year you must decide what to do with your RRSP.

You have three main options: Withdraw the money, purchase an annuity or, what most people do, transfer the funds into a registered retirement income fund (RRIF).

Withdrawing the full amount will subject you to a withholding tax. You might also have to pay tax on the income you receive after purchasing an annuity, a financial product designed to provide you a guaranteed regular income.

iStock-940070398

“Eventually, there’ll be a date where either you choose to, or you’re forced to take money out of that account, and it will mature into a RRIF,” said Ian Calvert, vice-president and principal at Toronto-based HighView Financial Group

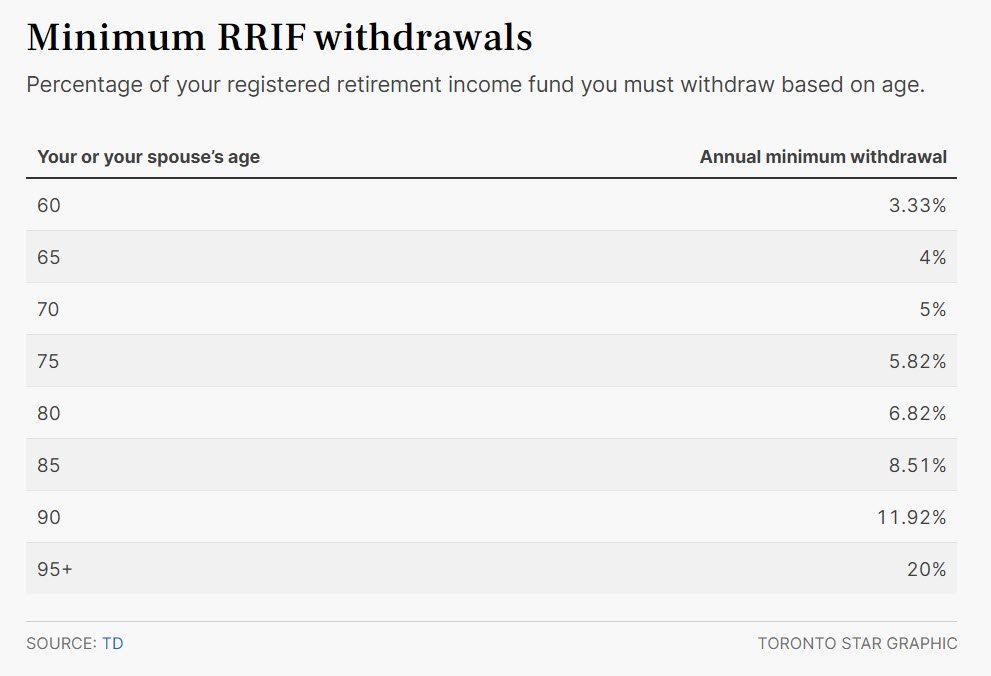

Converting an RRSP into an RRIF generates minimum withdrawals — which you can set up to be monthly, quarterly, semi-annually or annually — based on a rising percentage as you age. Canadians can make the most out of this account by implementing a few strategies.

Calvert said holding your investments in an RRIF allows gains on interest dividends to remain tax-sheltered until you draw money out and are taxed at your marginal tax rate at that time.

While converting your RRSP to a RRIF is mandatory by the end of the calendar year in which you turn 71, Calvert says there are tax planning benefits to converting some of the RRSP funds earlier, particularly if you’ve already retired and have no pension income.

“After the age of 65, the income from a RIFF is considered eligible pension income,” Calvert said, “which can be split with a partner and has a tax credit attached.”

This federal, non-refundable income tax credit applies to the first $2,000 of eligible pension, Calvert said. Plus, most financial institutions charge a deregistration fee for withdrawing directly from your RRSP.

“Converting over to the RRIF could be beneficial because you’d be avoiding that RRSP deregistration fee every time you make a withdrawal,” Calvert said.

Another key consideration Canadians sometimes forget about is to set up their spouse as a ‘successor annuitant’ on their RRIF account rather than as a ‘beneficiary,’ according to Victor Todorovski, financial planner and portfolio manager at Toronto-based Foster & Associates Financial Services.

“The account ‘rolls over’ tax-free, and the spouse or common-law partner becomes the successor annuitant of the RRIF,” he said. Otherwise, Todorvoski warns, the full amount of the RRIF could be taxable in the year the original annuitant has died.

Annuitants can also choose their spouse’s age to set the withdrawal amounts, said Todorovski.

These minimum withdrawals are subject to change and vary by age, ranging from 2.86 per cent at age 55 to 20 per cent at age 95. Todorovski says this flexibility can offer you a strategic advantage in your retirement planning.

“If your spouse happens to be younger, you might want to set it up based on their age.”