By Srivindhya Kolluru | Contributing Columnist

July 2, 2024

Despite the latest Bank of Canada interest rate cut, more Canadians are turning to their credit cards to pay for essentials, piling on debt in the process.

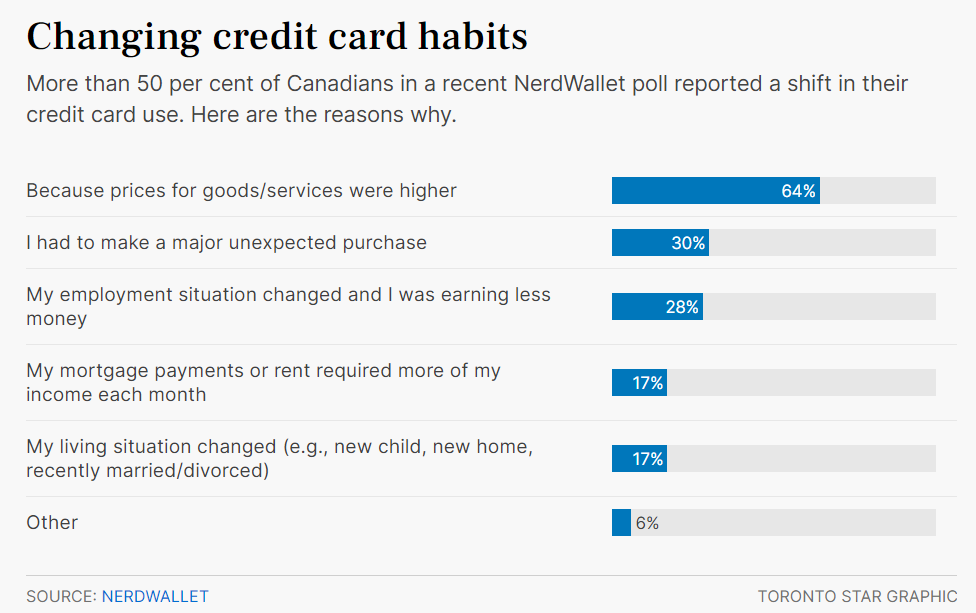

More than half of Canadian adults — 55 per cent — have credit card debt, up from 43 per cent in 2023, according to a recent poll from NerdWallet.

iStock-1217473554

Credit card delinquencies are also on the rise as fewer consumers are able to pay their balances off in full, according to a recent report from credit bureau Equifax Canada.

In struggling to deal with the problem, some Canadians are now using ‘balance transfers’ to manage nonmortgage debt. While this can give you some short-term breathing room, you need to be cautious.

A balance transfer is the process of moving your outstanding nonmortgage debt from one or more credit cards to another card with a lower interest rate. Standard credit card interest rates of almost 21 per cent in some cases can be punishing for consumers.

Balance transfer credit cards let you pay off debt faster since you’ll generally pay less interest over time.

For example, someone with $15,000 on two credit cards with a 19.99 per cent interest rate, could transfer the balances to a credit card that offers a promotional interest rate of zero per cent on a balance transfer completed within three months of opening the account.

But be mindful of when that promotional interest rate ends, which can range from three to 12 months, warns Ian Calvert, principal and vice-president at HighView Financial Group in Toronto. After that, some of the best balance transfer credit cards on the market feature rates between 12.99 and 17.99 per cent, according to Ratehub.

And make sure to ask about balance transfer fees, typically between one and three per cent of the amount you’re transferring, says Natasha Macmillan, director of everyday banking at Ratehub.ca

On the plus side, organizing your nonmortgage debt in one place can simplify your life and help you better track and eliminate the debt faster.

But be cautious about opening a new credit card just for a lower interest rate. While owning multiple cards may improve your credit score by reducing your debt-to-credit ratio, according to Equifax, using your available credit responsibly is crucial.

“If you can achieve it, consolidating your debt to a lower rate of interest is going to work out to your benefit in the long run,” says Calvert. “But opening up a lot of different credit cards at different financial institutions can potentially harm your credit score in the short term.”

Calvert and Macmillan stress that a balance transfer credit card should be seen as a short-term tool — not a solution — for getting out of debt.

If you habitually carry a balance each month, Macmillan advises looking into a low-interest credit card instead and seeing if that helps you save money. If you think you’ll need longer than a year to tackle your debt, she recommends looking at other avenues, such as taking out a personal loan or turning to a more comprehensive debt consolidation method.

“If you continue to accumulate credit card debt, consolidating it onto one card and then continuing to rack it up or increase it won’t make that problem go away,” says Calvert. “You need to look at your personal cash flow and what’s continuing to add to your credit card debt and tackle that first to move forward.”