Aug. 27, 2024

An early-warning system for recessions would be worth trillions of dollars. Governments could dole out stimulus at just the right time, and investors could turn a nice profit. Unfortunately, the process for calling a recession is too slow to be useful. America’s arbiter, the National Bureau of Economic Research, can take months to decide. Other countries simply look at GDP data, which emerge with a lag.

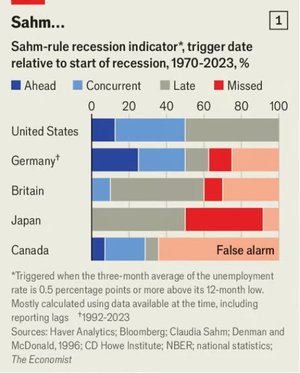

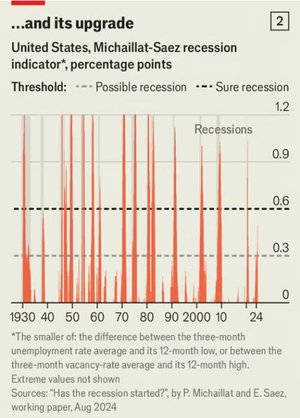

So recession-watchers have developed rules of thumb. Many now indicate trouble for America. Best-known is the Sahm Rule (see chart 1), which was triggered earlier this month. It looks for a short, sharp rise in unemployment, sounding the alarm when the three-month average of the unemployment rate moves by at least half a percentage point above its 12-month low. A new paper by Pascal Michaillat of the University of California, Santa Cruz, and Emmanuel Saez of the University of California, Berkeley, modifies the rule by adding a second indicator: changes in the job-openings rate. This catches every recession since the Depression, and entered the danger zone in March (see chart 2).

CHART: THE ECONOMIST

Other recession-seers look to the bond market. Historically, an inverted yield curve—where long-term interest rates fall below short-term ones—has preceded recessions. But inversions can come a year or more before an actual recession; indeed, the latest started in the summer of 2022. The moment to really panic has been when an inverted yield curve un-inverts. The 2s-10s yield curve, comparing the rates on two- and ten-year Treasuries, has been inching towards un-inverting for months (see chart 3). Now it is just 0.2 percentage points away. A paper from Thomas Philips of New York University combines the unemployment rate and the yield curve. His rule has had only two false alarms since 1960, and indicates that a recession started in July.

CHART: THE ECONOMIST

Is America doomed? Should investors bet on stocks cratering? Probably not. For one thing, Mr Philips finds that his rule calls recessions well, but is no good for investing. Using its strictures to switch portfolios around recessions mostly lost money relative to holding stocks throughout, aside from a good run during the global financial crisis of 2007-09. As stockmarkets tend to rise, investors have to get things absolutely spot-on, not just roughly right.

Recession rules also have deeper problems. A boom in immigration has distorted American jobs numbers. Goldman Sachs, a bank, reckons that 15% of the recent rise in unemployment reflects migration, since new arrivals are more likely to be jobless. Without this, the Sahm Rule would not have been triggered. The vacancies data that Messrs Michaillat and Saez lean on is also behaving unusually. Job openings leapt as covid-era stimulus juiced demand and lockdowns rejigged the economy. Vacancies have fallen sharply since, which helps trigger their rule, but are still at healthy levels in outright terms.

CHART: THE ECONOMIST

Another issue is that the rules are mostly based on American data. Yield-curve inversions and the Sahm Rule work less well elsewhere. Perhaps America’s economy is uniquely well-behaved, but it is more likely that the rules have been massaged to fit the contours of American history. In future, they will probably be more error-prone both in America and elsewhere.

Recession rules are based on the premise that once news gets bad enough, it will worsen further. Historically, that has been a decent bet: unemployment shoots up quickly and then falls slowly; central banks tend to raise interest rates until something breaks. Yet today the Federal Reserve has room to ease and, given the unusual labour-market recovery, some bumpiness does not spell disaster. Although America’s gangbusters expansion is calming, a gradual slowdown is not a crash—no matter what the rules say. ■