By JULIA KAGAN | Reviewed by ANTHONY BATTLE | Fact checked by SUZANNE KVILHAUG

July 5, 2024

What Is a 529 Plan?

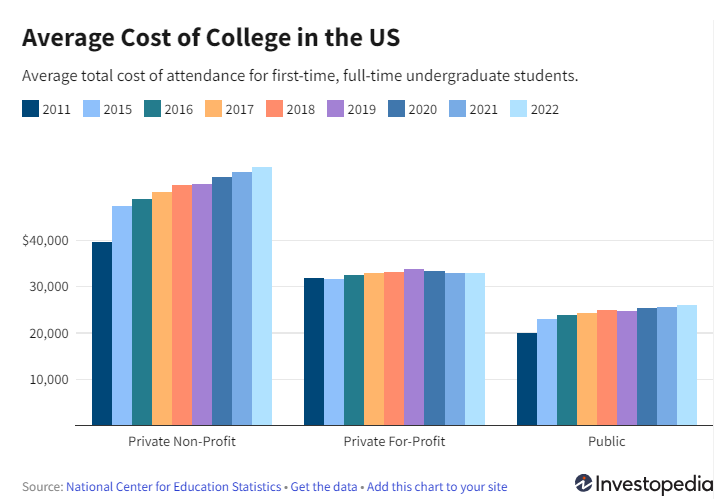

As the cost of higher education continues to rise and the problems of many Americans spending much of their adulthood mired in student debt is readily apparent, many are turning to tax-advantaged 529 savings plans to help fund their children's education. Named after Section 529 of the Internal Revenue Code (IRC), these plans were originally designed to cover postsecondary education costs.

Their scope has greatly expanded in the last decade. In 2017 and 2019, respectively, Congress passed legislation allowing 529 plans to cover the costs of K-12 education and apprenticeship programs.1 Later, the Setting Every Community Up for Retirement Enhancement (SECURE) Act of 2019 and the SECURE 2.0 Act of 2022 permitted 529 funds to be used for student loan repayment and Roth IRA contributions.²,³

iStock-1205534430

There are two main types of 529 plans:

- Education savings plans and prepaid tuition plans. Education savings plans offer tax-deferred growth, and withdrawals are tax-free when used for qualified education expenses. These plans remain under the control of the donor, usually a parent.⁴

- Prepaid tuition plans enable account owners to lock in current tuition rates for future attendance at selected colleges and universities.5 Given the rising costs of tuition, this generally means locking in lower prices for college later on.

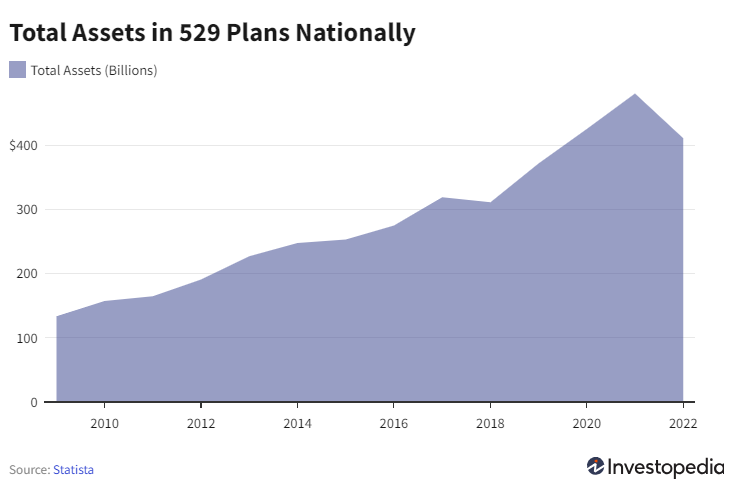

Despite their advantages, the Education Data Initiative estimated in 2023 that only about 30% of American college savings are held in 529 accounts. Nevertheless, those who do use them contribute an average of over $7,500 annually.⁶

KEY TAKEAWAYS

- Section 529 plans are tax-advantaged accounts that can be used to pay educational expenses from kindergarten through graduate school.

- There are two basic types of 529 plans: educational savings plans and prepaid tuition plans.

- Section 529 plans are sponsored and run by the 50 states and the District of Columbia. The rules and fees of 529 plans differ from state to state.

- These plans can be used directly through state platforms or via a broker or financial advisor.

- Up to $35,000 of leftover funds in a 529 account can be rolled over into a Roth individual retirement account (IRA), provided the fund is at least 15 years old.

Understanding 529 Plans

Although 529 plans take their name from Section 529 of the federal tax code, they are administered by the 50 states and the District of Columbia.⁷

Anyone can open a 529 account, but parents or grandparents typically establish them on behalf of a child or grandchild, the account's beneficiary. In some states, the person who funds the account may be eligible for a state tax deduction for their contributions.

The money in a 529 plan grows tax-deferred until it is withdrawn. What's more, as long as the money is used for qualified education expenses as defined by the Internal Revenue Service (IRS), withdrawals aren't subject to either state or federal taxes. In addition, some states may offer tax deductions on contributions.⁴

For K–12 students, tax-free withdrawals are limited to $10,000 annually.⁸

Since tax benefits vary from state to state, you should check the details of any 529 plan to understand the specific tax benefits to which you may be entitled.

Types of 529 Plans

The two main types of 529 plans have some significant differences.

Education Savings Plans

Of the two types, 529 savings plans are more common. The account holder contributes money to the plan, which is invested in a preset selection of investment options.

Account holders can choose which investments (usually mutual funds) they want to make. How those investments perform determines how much the account value grows over time.

Many 529 plans offer target-date funds, which adjust their assets as the years go by, becoming more conservative as the beneficiary approaches college age. Withdrawals from a 529 savings plan can be used for college and K–12 qualified expenses. Qualified expenses include tuition, fees, room and board, and related costs.⁹

The SECURE Act of 2019 expanded tax-free 529 plan withdrawals to include registered apprenticeship program expenses and up to $10,000 in student loan debt repayment for account beneficiaries and their siblings.³

The SECURE Act of 2022, passed as part of the 2023 omnibus funding bill, permits rolling over up to $35,000 of unspent funds in a 529 account into a Roth IRA account. The account must be at least 15 years old to qualify.¹⁰,¹¹

Prepaid Tuition Plans

Prepaid tuition plans are offered by a few states and some higher education institutions. They vary in their specifics, but the general principle is that they allow you to lock in tuition at current rates for a student who may not be attending college for years to come. Prepaid plans are not available for K–12 education.

As with 529 savings plans, prepaid tuition plans grow in value over time. Eventual withdrawals from the account used to pay tuition are not taxable. However, unlike savings plans, prepaid tuition plans do not cover the costs of room and board.

Prepaid tuition plans may place a limit on which colleges they may be used for. By contrast, the money in a savings plan can be used at almost any eligible institution.

In addition, the money paid into a prepaid tuition plan isn't guaranteed by the federal government and may not be guaranteed by some states.⁹ Be sure you understand all aspects of the prepaid tuition plan before you use it.

Contribution Limits Differ Across States

There are no limits on how much you can contribute to a 529 account each year. However, many states cap the total amount you can contribute over time, ranging from $235,000 to $575,000.¹²

Tax Advantages of 529 Plans

Withdrawals from a 529 plan are exempt from federal and state income taxes, provided the money is used for qualified educational expenses.

Any other withdrawals are subject to taxes plus a 10% penalty, with exceptions for certain circumstances, such as after death or disability.⁹

Contributions to a 529 plan aren't tax deductible for federal income tax purposes. However, more than 30 states provide tax deductions or credits of varying amounts for these contributions.¹²

You need to invest in your home state's plan if you want a state tax deduction or credit. However, some states will allow you to invest in their plans as a nonresident if you're willing to forgo a tax break.

Gift Tax Implications

In 2024, the annual gift tax exclusion has increased to $18,000, up from $17,000 in 2023. This means that you can give up to $18,000 per year to any individual without it counting against your lifetime gift tax exemption, which has also increased to $13.61 million for single filers and $27.22 million for married couples filing jointly, up from $12.92 million and $25.84 million in 2023, respectively.

This background on gift taxes is important for 529 plans since there are additional tax advantages for those who wish to contribute to the savings of a future college student. You can contribute up to five years' worth of annual gift tax exclusions in a single lump sum without triggering gift tax consequences. For instance, in 2024, a grandparent could make a one-time contribution of $90,000 to their grandchild's 529 plan ($18,000 annual exclusion x five years).

As long as the grandparent does not make any additional contributions to the same beneficiary over the next five years, this lump-sum contribution will not count against their lifetime gift tax exemption.¹³,¹

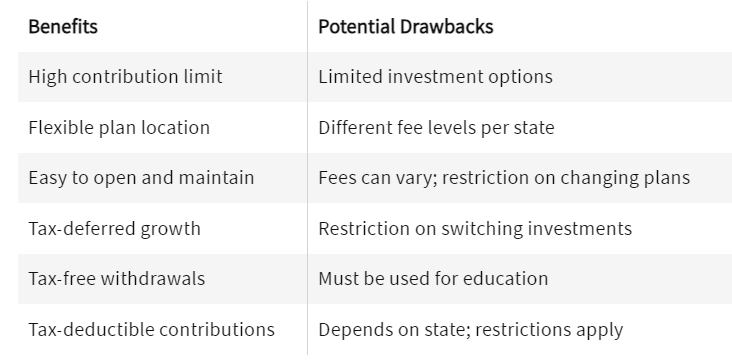

Benefits and Potential Drawbacks of 529 Plans

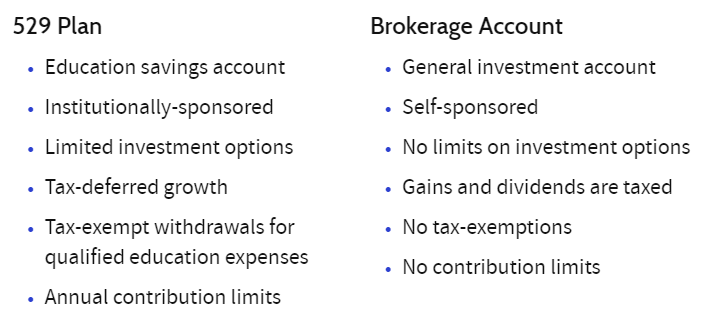

529 Plans vs. Brokerage Accounts

When saving for college, 529 plans and individual brokerage accounts are two popular options. A 529 plan is a tax-advantaged investment account designed specifically for education expenses. By contrast, a brokerage account is a general-purpose investment account with no specific tax benefits for education savings.

Section 529 plans are sponsored by a state or financial institution and have limited investment options, often through a menu of mutual funds or ETFs. Your selection may include age-based options that automatically adjust the asset allocation as the beneficiary approaches college age. They also offer tax-deferred growth and tax-free withdrawals for qualified education expenses. Plan withdrawals are then tax-free if used for qualified education expenses, such as tuition, fees, books, and room and board. Some states offer additional tax benefits, such as deductions or credits for contributions to in-state 529 plans. There are no annual contribution limits, but there are limits on the total in a given account, from $235,000 in Georgia and Mississippi to $575,000 in California.¹⁴

Meanwhile, brokerage accounts offer a wide range of investment options, including individual stocks, bonds, mutual funds, and ETFs. There are no contribution limits, but gains and dividends are taxable in the current period. There are also no additional benefits to using the proceeds for educational purposes.

Suppose your child does not end up going to college. In that case, funds in a 529 plan can be transferred to another qualifying family member or used for other education expenses, such as apprenticeships, graduate school, or student loan repayments (up to $10,000). Nonqualified withdrawals or transfers, however, are fully taxable and may carry penalties. Brokerage account funds can be used for any purpose, including education, without restrictions or penalties.

529 Plan Transferability Rules

Section 529 plans have specific transferability rules governed by the federal tax code. The owner may transfer funds to another 529 plan once per year unless a beneficiary change is involved. You are not required to change plans to change beneficiaries. You may transfer the plan to another family member, who is defined as one of the following:

- Son, daughter, stepchild, foster child, adopted child, or a descendant of any of them

- Brother, sister, stepbrother, or stepsister

- Father or mother or ancestor of either

- Stepfather or stepmother

- Son or daughter of a brother or sister

- Brother or sister of father or mother

- Son-in-law, daughter-in-law, father-in-law, mother-in-law, brother-in-law, or sister-in-law

- The spouse of any individual listed above

- First cousin

TIP: You aren't restricted to investing in your own state's 529 plan, but doing so may get you a tax break. Be sure to check out your state's plan first.

Additional Tips for 529 Plans

As with other kinds of investing, the earlier you get started, the better. With a 529 plan, your money will have more time to grow and compound the sooner it's opened and funded.

Prepaid tuition plans offer the advantage of locking in current tuition rates, potentially saving you money compared with future prices, as many schools increase tuition annually.

If you have leftover funds in a 529 plan, such as when the beneficiary receives a significant scholarship or chooses not to go to college, you have several options. You can change the beneficiary to another qualifying relative, keep the current beneficiary in case they decide to pursue higher education later or attend graduate school, or use up to $10,000 to repay the original beneficiary's or their siblings' federal or private student loans.

You can also transfer unused funds to a Roth IRA if your account meets the necessary requirements. Lastly, you can always withdraw the money, although you will be subject to taxes and a 10% penalty on the earnings portion of the withdrawal.

How Much Does a 529 Plan Cost?

States often charge an annual maintenance fee for a 529 plan, which ranges from free to $25.15 In addition, if you bought your 529 plan through a broker or advisor, they may charge you an additional fee for the assets under management.¹⁶ The individual investments and funds inside your 529 may also charge ongoing fees. Look for low-cost mutual funds and ETFs to keep management fees low.

Who Maintains Control Over a 529 Plan?

A 529 plan is technically a custodial account, so an adult custodian controls the funds for the benefit of a minor. The beneficiary can assume control over the 529 once they turn 18. However, the funds must still be used for qualifying education expenses.

What Are Qualified Expenses for a 529 Plan?

Qualified expenses for a 529 plan include the following:¹

- College, graduate, or vocational school tuition and fees

- Elementary or secondary school (K–12) tuition and fees

- Books and school supplies

- Student loan payments

- Room and board

- Computers, internet, and software used for schoolwork (student attendance required)

- Special needs and accessibility equipment for students

The Bottom Line

Creating a 529 plan gives you a tax-advantaged strategy to save for educational expenses from kindergarten to graduate school, including apprenticeship programs.¹⁷ If the 529 account is 15 or more years old, you can move up to $35,000 of unspent funds into a Roth IRA account. With many choices for a 529 plan, you get great flexibility and the potential for tax-advantaged growth to help with saving for the needs of future college students.

ARTICLE SOURCES

Investopedia requires writers to use primary sources to support their work. These include white papers, government data, original reporting, and interviews with industry experts. We also reference original research from other reputable publishers where appropriate. You can learn more about the standards we follow in producing accurate, unbiased content in our editorial policy.

- Internal Revenue Service. "Publication 970 (2023), Tax Benefits for Education."

- U.S. Congress. "SECURE 2.0 of 2022 Act."

- U.S. Congress. "H.R.1994 - Setting Every Community Up for Retirement Enhancement Act of 2019," Sec. 302.

- Internal Revenue Service. "TG 44: Qualified Tuition Programs."

- U.S. Securities and Exchange Commission. "An Introduction to 529 Plans."

- Education Data Initiative. "College Savings Data."

- National Association of State Treasurers. "College Savings."

- Internal Revenue Service. "Topic No. 313 Qualified Tuition Programs (QTPs)."

- U.S. Securities and Exchange Commission. "An Introduction to 529 Plans."

- Congress.gov. "H.R. 2617 - Consolidated Appropriations Act, 2023." Division T, Section 126.

- my529. "SECURE Act 2.0."

- 529 College Savings Plan. "529 Plan Comparison by State."

- Internal Revenue Service. "Gift Tax."

- Saving for College. "How Much Is Your State’s 529 Plan Tax Deduction Really Worth?"

- Saving For College. "529 Fee Study."

- The Wall Street Journal. "The Fees on Your ‘529’ Tuition-Savings Plan Matter More than Ever."

- U.S. Securities and Exchange Commission. "Investor Bulletin: 10 Questions to Consider Before Opening a 529 Account."