A Critical Combo: Life Insurance with Long-Term Care Benefits

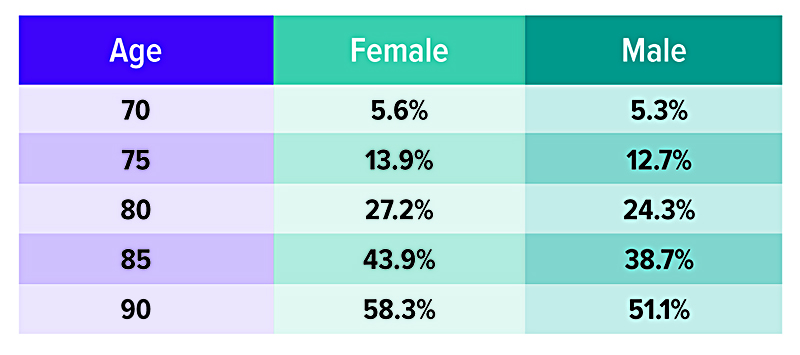

An important part of any retirement strategy involves accounting for potential long-term care (LTC) expenses, which can be surprisingly high. The median cost of a private room in a nursing home was $9,733 in 2023, while a full-time home health aide was $6,292 per month. 1

If you plan to pay for care out of pocket, consider how long your retirement savings would last if you or your spouse end up needing care in a nursing home for several years. How would writing those checks every month affect the healthy spouse's quality of life?

On the other hand, you may not like the idea of paying costly premiums for traditional long-term care insurance that you might never need. If so, you may be interested in one of these alternatives that combine permanent life insurance with long-term care coverage.

An efficient hybrid

Although LTC insurance is typically a "use-it-or-lose-it" proposition, a hybrid (or linked-benefit) policy can help pay for care if it's needed or provide a larger death benefit for your beneficiaries if it's not. Hybrid policies are generally more expensive than standalone LTC policies, and the maximum LTC benefit may be smaller. Currently, the max LTC benefit amount is typically equal to about five times the premium. 2

A hybrid policy may be purchased with a single premium, or installments paid over a few years (usually no more than 10). And you won't have to worry about future rate increases or the issuer canceling the policy, which can happen with a traditional LTC policy.

Tack on a rider

Another option is to buy a life policy with an attached long-term care rider — which typically can't be added later. Any LTC payments are usually limited to the death benefit, which means they are generally not as robust as with a standalone LTC policy or a linked-benefit policy. However, the death benefit is larger (for the same premium).

If you consider either of these strategies, you should have a need for life insurance and evaluate the policy on its merits as life insurance.

Collecting benefits

Long-term care benefits kick in when the insured person needs help with two or more activities of daily living (such as eating, bathing, and transferring) or is severely cognitively impaired, though there is typically a 90-day waiting, or elimination, period. Care may be provided in your home or at a facility.

With linked-benefit policies and LTC riders, benefits may be paid through reimbursement of the actual cost of care or an indemnity model that pays a certain cash benefit regardless of the actual cost of care. If your policy uses an indemnity model, it might allow you to pay a family caregiver. When you use the LTC benefit, the death benefit is reduced, but some policies may still offer a small death benefit even if you use up the LTC coverage.

Plus, permanent life policies and most hybrid life-LTC policies have a cash-value component that you could tap into for emergencies or retirement income if you are lucky enough to need little or no care. (Loans and withdrawals will reduce the policy's cash value and death benefit.)

The danger in waiting to explore combination life-LTC policies — beyond the fact that premiums rise with age — is that you could develop a health condition that would disqualify you from coverage.

The cost and availability of life insurance depend on factors such as age, health, and the type and amount of insurance purchased. Policies commonly have mortality and expense charges. If a policy is surrendered prematurely, there may be surrender charges and income tax implications. Optional benefit riders are available for an additional cost and are subject to the contractual terms, conditions, and limitations outlined in the policy; they may not, however, benefit all individuals. Any guarantees are contingent on the financial strength and claims-paying ability of the issuing insurance company.